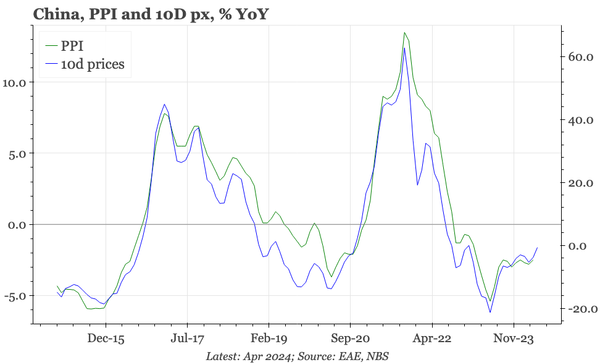

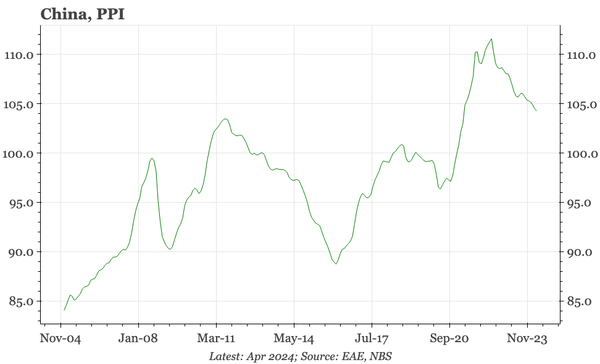

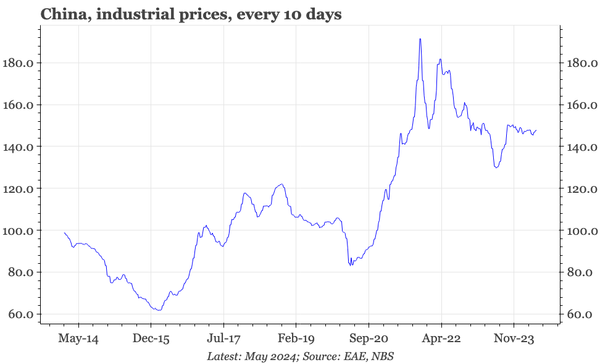

China – still expecting PPI to rebound The April PPI data were soft, but the government's higher-frequency series for industrial prices, updated today for the first 10 days of May, continues to suggest a lessening of deflation.

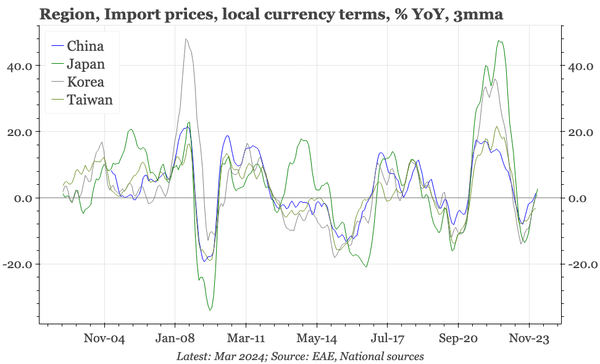

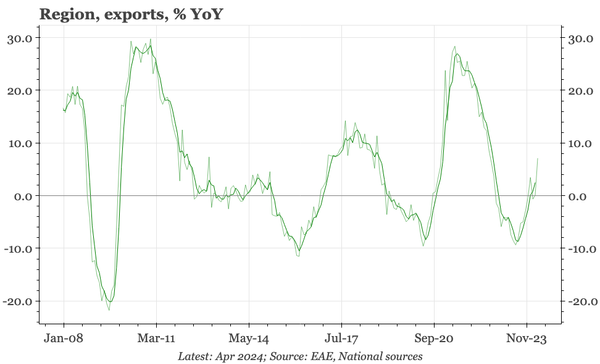

Region – import price inflation returns External goods price disinflation is now over, with import prices now rising again across the region. That is likely to feed into stronger PPI, even in China.

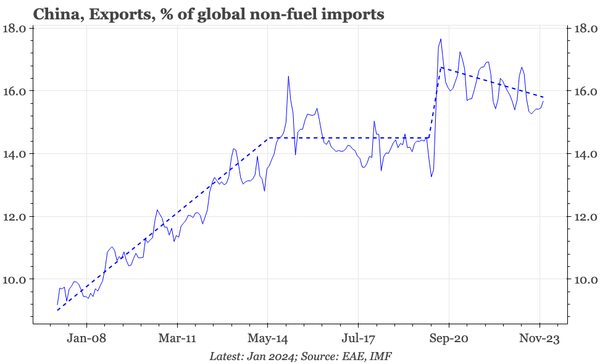

China – exports not quite so all-conquering In contrast to the common impression, China's global market share has been falling. Whether this is just a pause after the covid surge or something more permanent will be a big theme in 2024 for China's cycle, the CNY and China's trade relations with ROW.

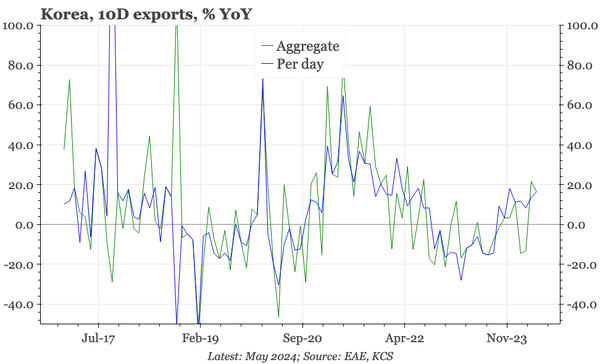

Korea – exports stronger so far in May On a headline basis, export growth accelerated again in the first ten days of May. That keeps alive the theme of industrial recovery, even if some of the details continue to look more sluggish.

Last week, next week A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

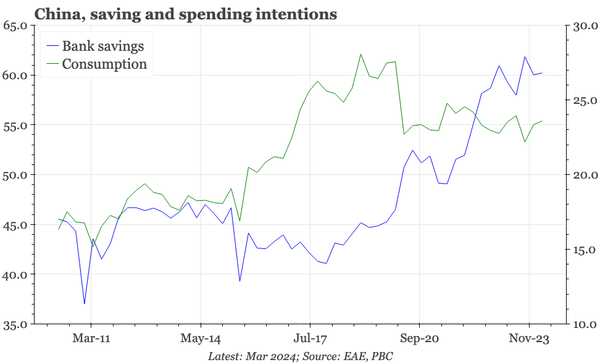

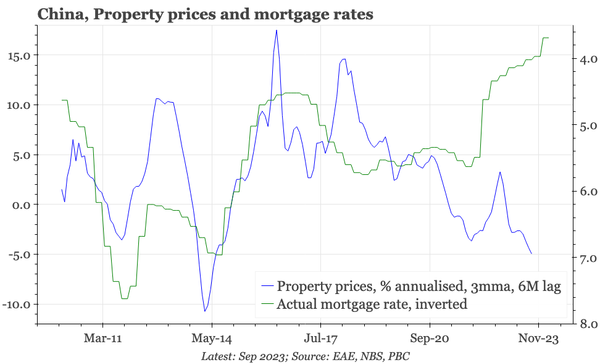

China – mortgage rates still falling fast Data in yesterday's Q1 monetary policy report showed another sharp fall in mortgage rates to well below 4%. But while they worked before, rate cuts in this cycle have shown no sign yet of boosting buyer sentiment.

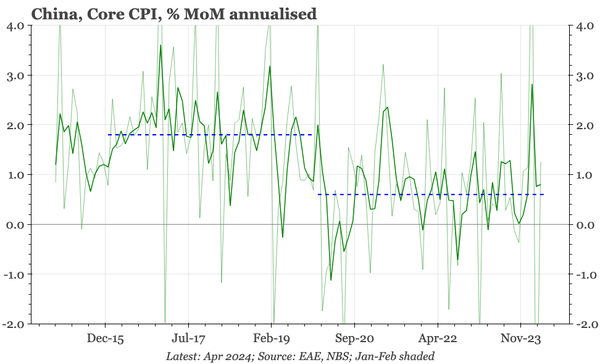

China – core inflation low but stable Core CPI inflation continues to run at a bit below 1% annualised. That is too low for comfort, though for now doesn't show any sign of taking a new step down into deflation.

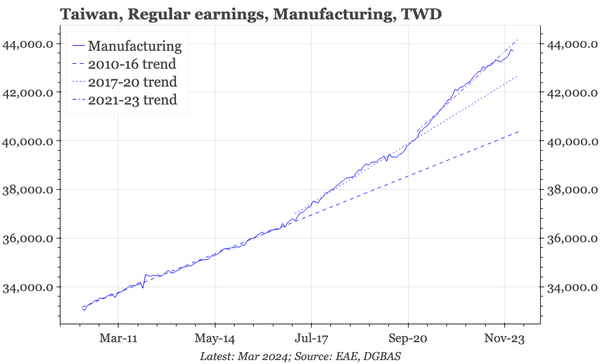

Taiwan – wage growth slower in March Cyclically, wage growth has slowed from over 2.5% YoY in 23 to 1.4% now. But the structural rise in manufacturing wage growth is persisting, which will have macro significance if the sector convincingly lifts out of recession.

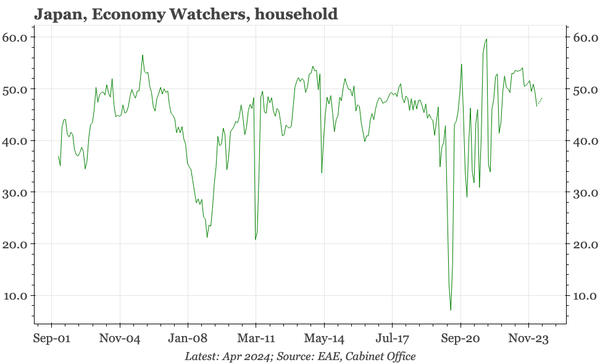

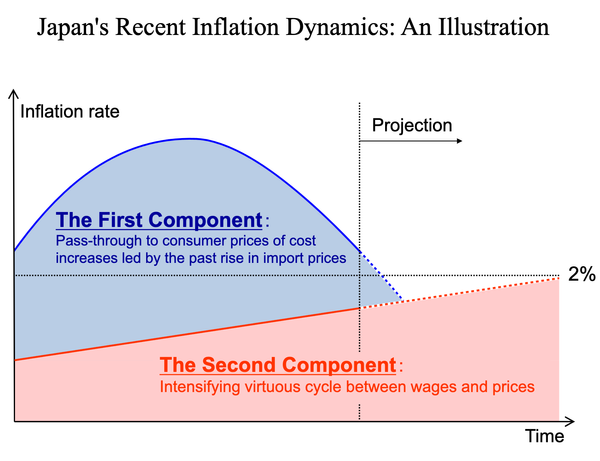

Japan – households lead sentiment lower There was quite a big fall in the EW survey in April, a warning that recent JPY volatility might be pushing up inflation expectations again.

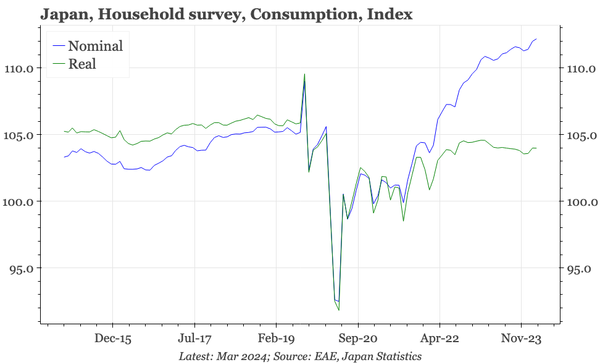

Japan – another weak consumption indicator While a bit stronger than the beginning of this year, the household survey shows real consumption spending still 2% lower than in 2019.

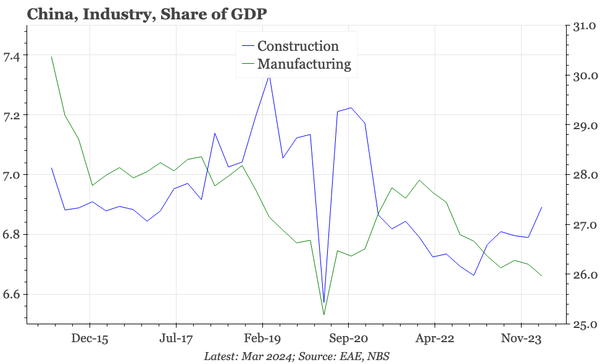

China – construction up, manufacturing down Another chart that challenges the idea that the structure of China's economy has changed much. Relative to GDP, construction is rebounding, while manufacturing is falling.

Japan – no consumption recovery yet PMIs, CPI, wages, profits....most macro indicators look positive. The one weak spot remains consumption, with little sign of improvement through March.

China – moderate export recovery Underlying trade values show the moderate export recovery that began in mid-23 is continuing, while imports are flat-lining.

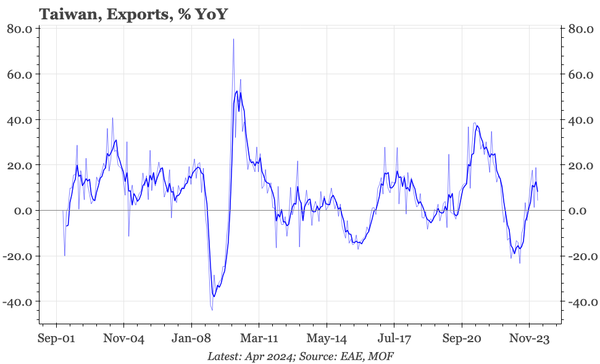

Taiwan – export recovery falters in April The nominal export recovery across the region has lost momentum, with Taiwan's April exports fading YoY and MoM.

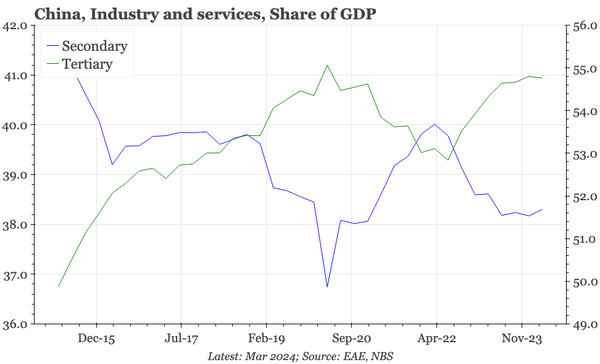

China – has anything really changed? It is often thought that China is transforming into a mfg-led, services-light economy. Relative growth did slow post-15. However, as a proportion of GDP, the services sector has never been bigger.

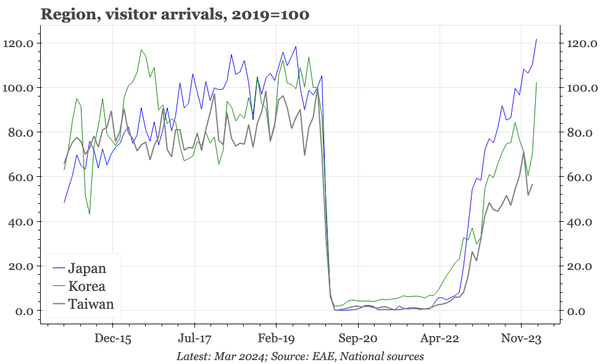

Region – perhaps the weak KRW helps as well It seems reasonable to think the cheap JPY is contributing to Japan's tourism boom. But Korea's visitor numbers are also closing in on pre-covid levels. Recovery in Taiwan, by contrast, is lagging.

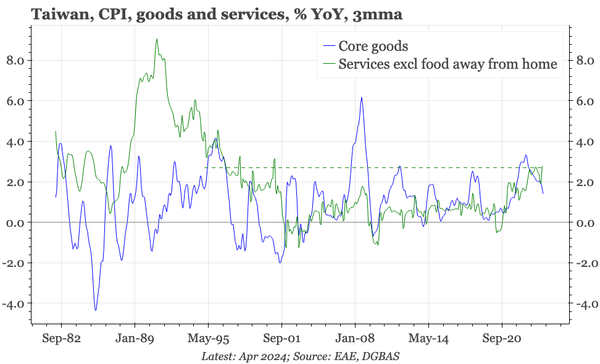

Taiwan – inflation still firm Headline inflation dropped below 2% YoY in April, and core eased too. But underlying services inflation – a proxy for domestically generated price pressures – remains at almost 3%, a near 30-year high.

China – PPI flat Prices might be drifting down a bit, and there's big product differences (steel weak, copper strong), but high-frequency data don't suggest any real deflation emanating from China's industrial sector.