Subscribers Only

Japan – becoming binary

It is just about possible to defend the BOJ's slow but steady hikes since 2024, in the sense that growth, inflation and the JPY have all been rangebound. But leading indicators for growth and inflation are now rising. I'd expect the bank to now move faster. The market still isn't priced for that.

Subscribers Only

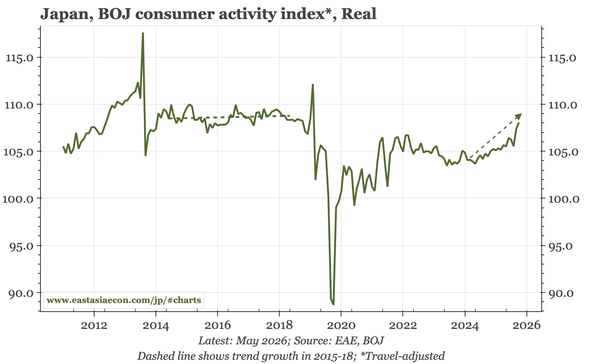

Japan – wages don't fully explain stronger spending

Today's May consumption activity data were stronger again. That rise can be explained by three factors: a temporary boost as purchases of household appliances are brought forward, decent – though in May, not necessarily stronger – wage growth, and perhaps, a wealth effect as asset prices rise.

Subscribers Only

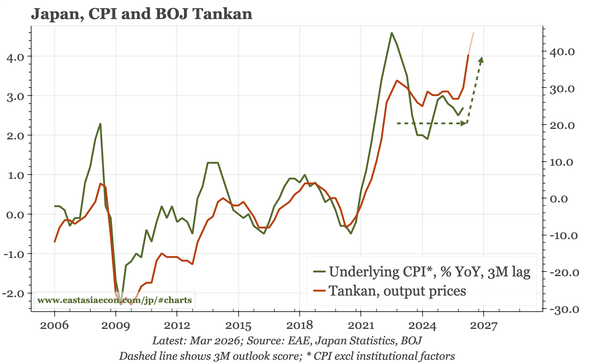

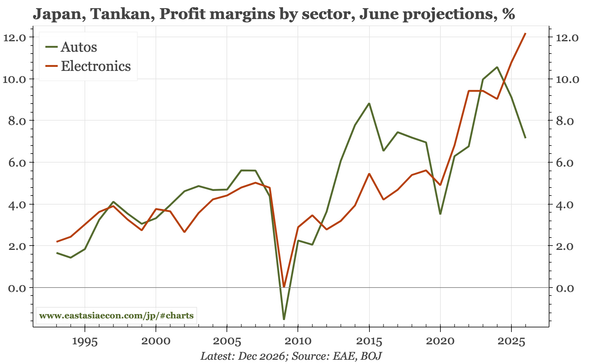

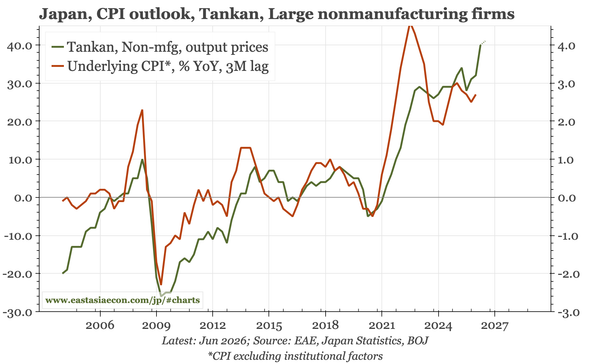

Japan – AI boosting manufacturing

The detailed release of the Tankan confirms the message of yesterday's summary: price pressures are rising again, and momentum in the corporate sector is strong. There is some sluggishness in autos, but as in export data, that is being offset by AI demand for electronics.

Subscribers Only

Japan – sentiment strong, prices stronger

The detailed version of the Tankan won't be released until tomorrow. But the headlines today show a clear story: business sentiment remains strong, and inflation pressures have risen yet again. The BOJ needs to become more hawkish.

Subscribers Only

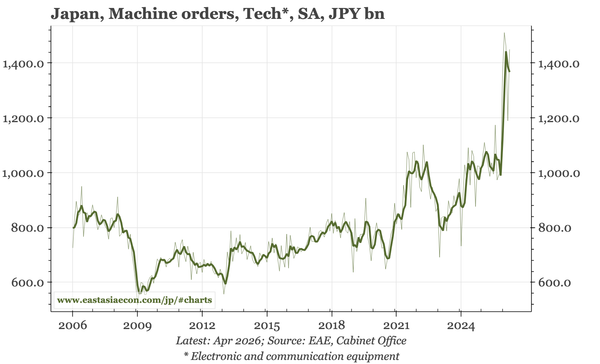

Japan – manufacturing upturn

Before the war, Japan's manufacturing cycle was gaining momentum. If the war is now over, then today's releases of machine orders, exports and business sentiment suggest that strengthening momentum can now become an important theme for Japan macro.

Subscribers Only

Japan – import prices up, but export prices too

The renewed rise in import prices is certainly inflationary, especially when the level of prices remains elevated after the hikes of 2021-22. However, this time export prices are rising too, and while that isn't enough to prevent the ToT from falling, it does limit the damage to the domestic economy

Subscribers Only

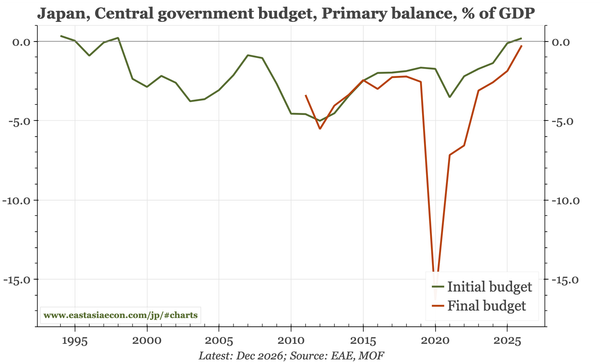

Japan – enough, if the BOJ decides it is

The narrowing budget deficit and widening BOP surplus likely won't move market opinion on either rates or fx. What is needed remains a more hawkish BOJ. Accelerating credit and wage growth push in that direction, though the wage data aren't great quality, and sentiment surveys are still weak.

Subscribers Only

Japan – Ueda stresses inflation risks

Some highlights from governor's speech today: his remarks about strong bank lending, higher prices being a bigger burden to firms than rising rates, the link between low policy rates and the rise in market yields, and the upside risks to prices now that the "deflationary mindset has been dispelled".

Subscribers Only

Japan – offsets to Iran

Tuition as well as energy subsidies make inflation look particularly low relative to the likely upside from the Iran war. The conflict will also slow growth. However, both export data for April and Koeda's speech yesterday indicate that growth downside will be limited if global tech demand sustains.