Subscribers Only

China – PMIs down again

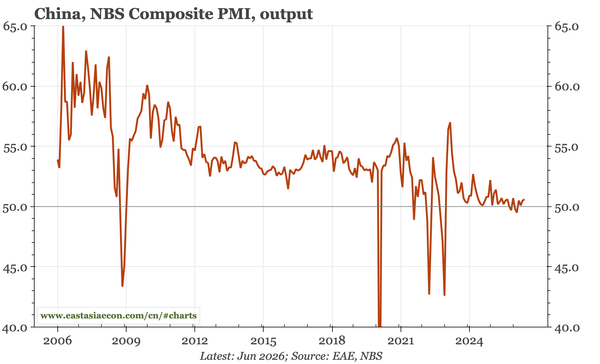

The across-the-board weakening of the official PMIs will reinforce cycle pessimism, with px indicators point to an end of the recent upturn in PPI inflation. The likelihood of renewed monetary easing is growing, but detailed data – and the Politburo statement – suggest only incremental change.

Subscribers Only

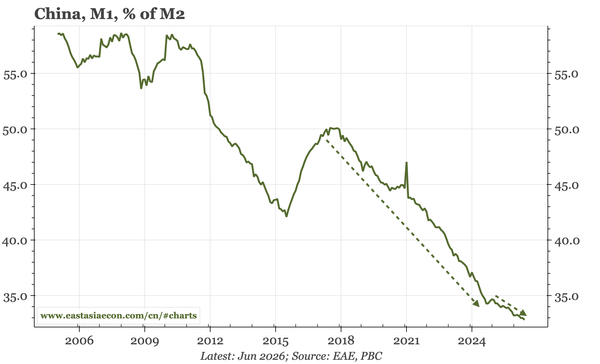

China – M1 growth slowing again

The continued slowdown in credit growth is led by households and CGBs – corporate borrowing has been firm. But the M1:M2 ratio is slipping again, warning that the domestic dynamic that had contributed to lessening deflation and a less dovish PBC is now once again fading.

Subscribers Only

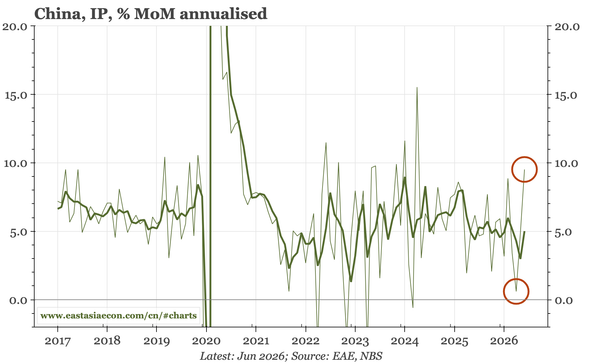

China – still weak, but better in June

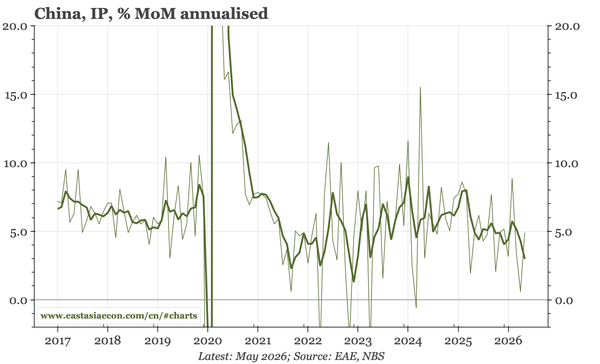

Q2 GDP data were weak, but the damage was done at the start of the quarter, with a clear improvement in industrial momentum thereafter. With the deflator also positive for the first time since 2022, that's likely enough for policymakers, even though domestic demand remains a mess.

Public Post

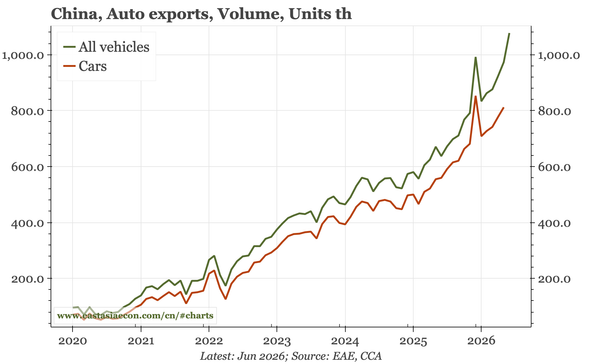

China – further export strength

China's exports continue to be strong. The rise in prices of semiconductors is playing a role, but so is the sharp increase in auto volumes, which is now over 1mn vehicles a month. Protectionism in the rest of the world has yet to disrupt these trends, which thus continue to support China's GDP.

Subscribers Only

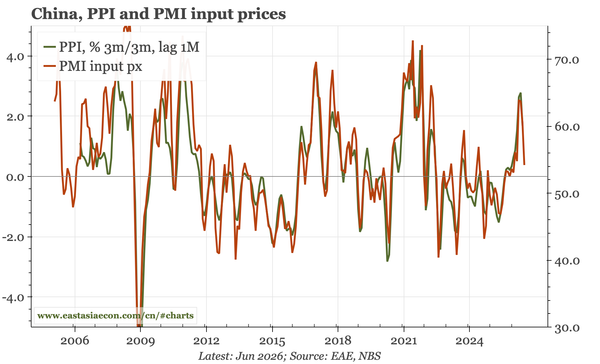

China – inflation peak

Average CPI and PPI inflation remained relatively elevated in June. However, most of the rise has been because of external factors, and leading indicators show that for now, the peak has likely been seen.

Subscribers Only

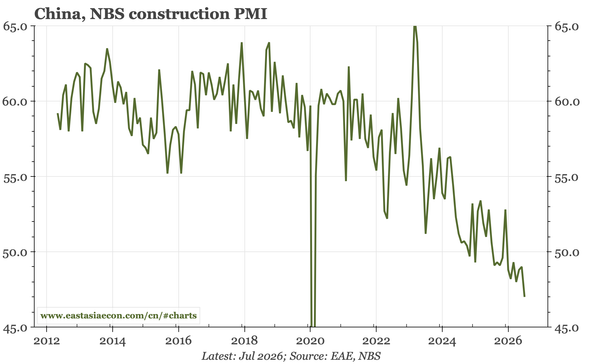

China – not much change in PMIs

Today's official PMIs ticked up, but not by enough to clear market concern about the strength of the cycle caused by the weak IP, retail sales and FAI data of the last couple of months.

Public Post

China – is (it still possible) the worst is over?

My latest video, making the case for a bottoming of China's economy. In light of this week's poor official data, the argument might look off-base, which means it should at least be interesting. I do think the logic holds up, but as discussed here, there are reasons I could be wrong.

Subscribers Only

China – another month of weak data

I have been arguing that the underlying economy has been stabilising, with prices bottoming out before the Iran war. But stabilisation is external-led, and today's data show the domestic cycle remains a mess. That will likely become a policy issue if IP doesn't stay at an annualised run-rate of 5%

Subscribers Only

China – externally driven inflation

The rise in PPI that continued in May is of macro significance: it is pushing up industrial sector earnings, and the GDP deflator will likely turn positive in Q2. But it is difficult to find signs of domestically generated inflation that would suggest a real upturn in the economy.