Subscribers Only

Taiwan – no excitement from the CBC

The CBC didn't change policy today. It increased its growth forecast, but didn't sound excited about the outlook. It warned about excesses related to equities, but didn't announce any remedial policies. Inflation is expected to remain below 2%.

Subscribers Only

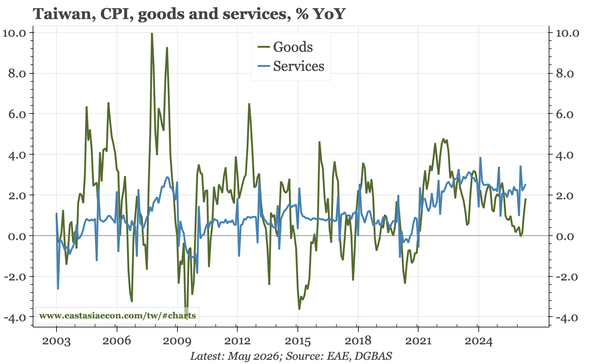

Taiwan – services inflation back at 2.5%

Services inflation averaged 0.7% in the 20 years before 2020. In the last five years it has been 2.3%, and is now rising again. Some of that reflects energy prices, with air fares rising 10% YoY in May. But there is also the backdrop of a strong economy, rising stockmarket and rising wage growth.

Subscribers Only

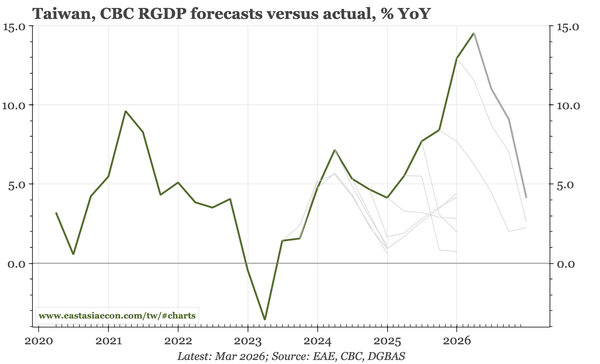

Taiwan – growth up, now inflation too

Today's Q1 GDP data show the economy growing more quickly than any time in over 40 years. The government thinks that continues: in the forecast, downside risk from Iran isn't mentioned, but trickle down from semi to the real economy is. CPI was also revised up, even if it remains (just) below 2%.

Subscribers Only

Taiwan – Trump shifts position

My initial interpretation of the Xi-Trump meeting looks wrong. While in the official talks neither side gave much, in a subsequent interview with Fox news, President Trump softened US support for Taiwan. Over the medium-term, that could be significant for politics in Taiwan, and currency valuations.

Subscribers Only

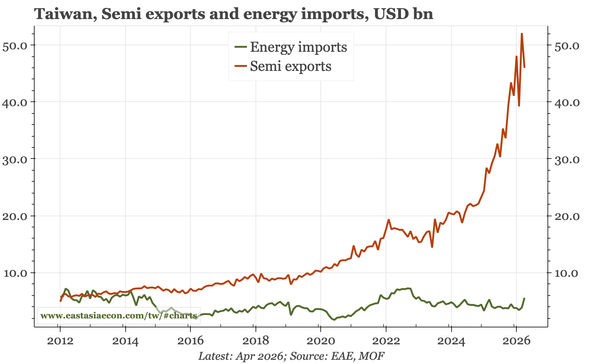

Taiwan – limited impact yet

April trade data show little damage from the Iran war. If the crisis remains limited to energy prices, Taiwan should be somewhat insulated. Energy imports are small relative to chip exports, and while import prices will rise, export prices are now also increasing for the first time in a generation.

Public Post

Taiwan – why macro matters

Latest video, discussing one of my main themes: that Taiwan macro is more relevant for global investors than it has been for a long time.

Subscribers Only

Taiwan – export surge continues

Exports in March were strong again. There aren't yet signs of the Iran war derailing the chip cycle, and while energy imports will increase more quickly, the impact on the trade surplus will be limited. The outlook for Taiwan as of now is resilient growth and higher inflation.

Public Post

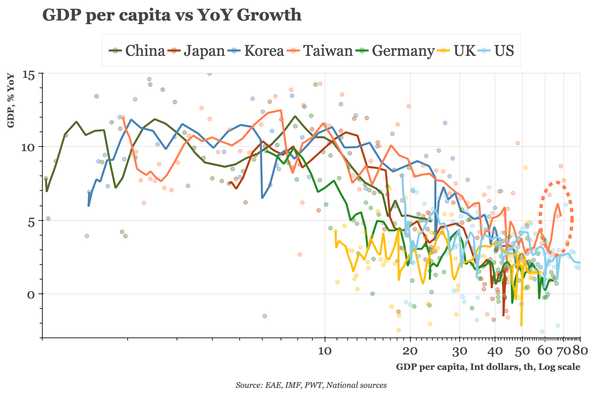

Taiwan – the world's most interesting economy?

I've been arguing that Taiwan is one of the most interesting macro stories in the world right now. I had the chance to lay out some of the elements in this week's Bloomberg Asia Centric podcast.

Subscribers Only

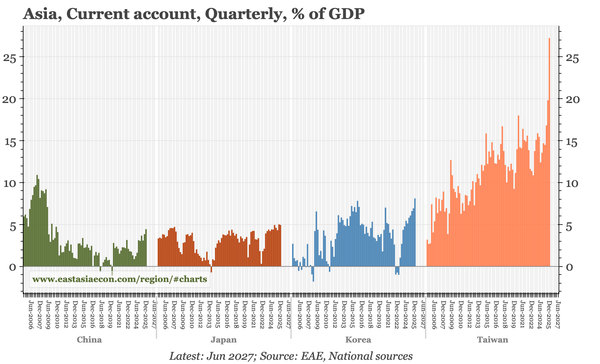

Taiwan – huge CA to rise yet further

The surge in the current account surplus of January-September continued into the end of 2025. In Q4, the surplus reached almost 30% of GDP. The government's GDP forecast implies that will be roughly the size of the full-year surplus in 2026. Taiwan needs huge capital outflows to keep the TWD stable.