Subscribers Only

Weekly: CMXT and JPY

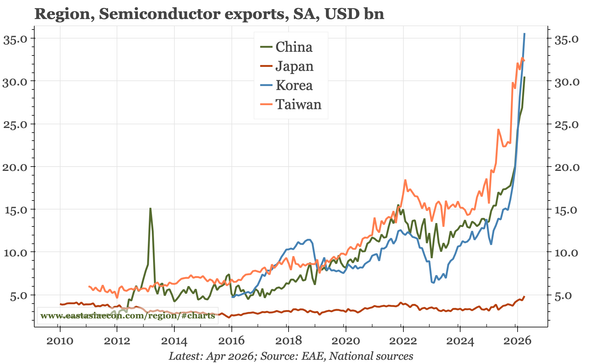

The two big events this week are China's CXMT listing and the Bank of Japan meeting. The first matters because the outlook for chip demand is such a dominant regional theme. The BOJ meeting is important because of rates in Japan, but also implications for the JPY and regional currencies.

Subscribers Only

Weekly

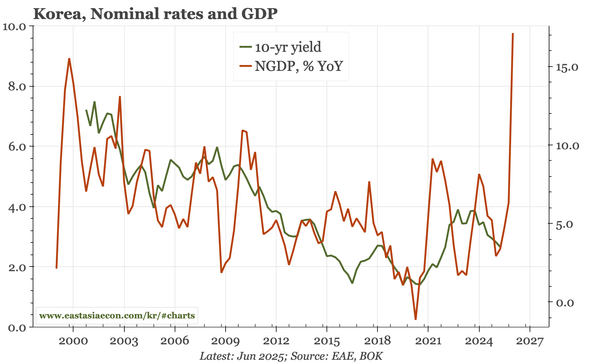

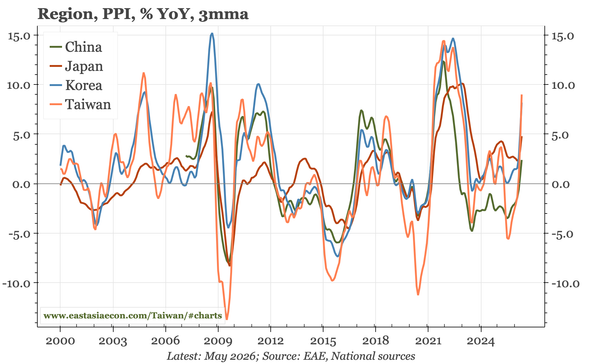

China's combination of recovering output, weak expenditure, and mixed monetary isn't great, but also doesn't suggest a big change in macro policy. I think it unlikely that Japan's bid for repatriation works without more BOJ normalisation. Korea and Taiwan cycles remain strong, implying rate hikes.

Public Post

Region – the upside risks to inflation

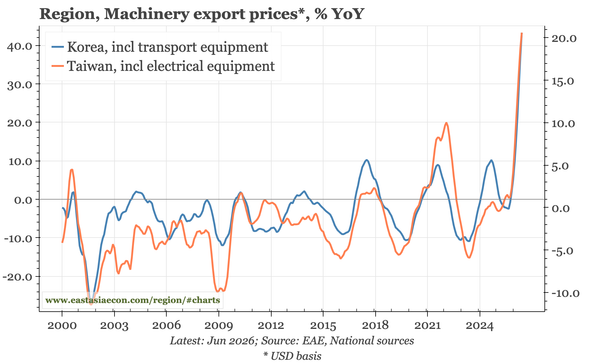

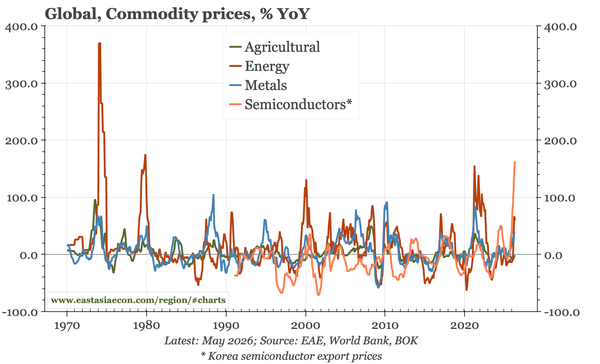

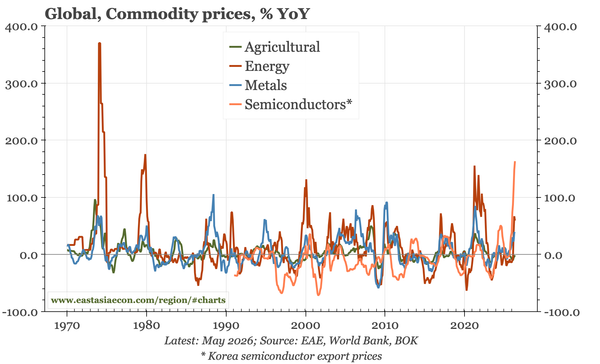

My latest video, discussing why inflation risks won't end even if the Iran War eventually does. The reasons: both cost-push and demand-pull from the semiconductor boom, dynamics that are being reinforced by the cheapness of currencies.

Subscribers Only

Region – chart pack

A slide pack laying out themes for the region overall, and for each individual economy.

Subscribers Only

Weekly – two questions: oil, and China

Two of the big questions for markets in the region are 1) the implications for monetary policy as oil prices fall, and 2) what is happening with China's cycle, and what does that – and the strengthening of the USD – mean for the USD.

Subscribers Only

Region – commodity boom or BS....slide pack

Earlier this week, I published a longer note delving into the macro and market implications of the semiconductor boom. You prefer pictures to text, so this is the accompanying chart pack.

Subscribers Only

Last week, next week

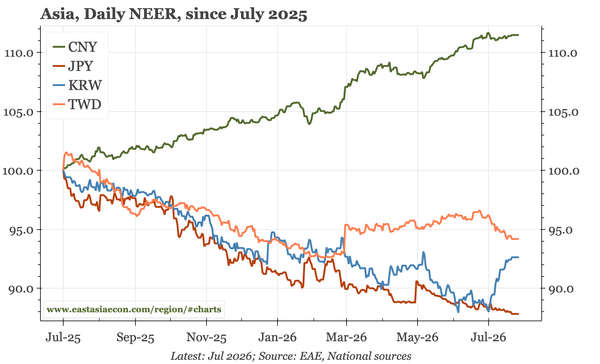

China's cycle is weak, but I'm not yet convinced it is getting worse. Japan's cycle will now be improving, but the BOJ needs to show that it can keep up. The BOK's hawkish turn can go further still if the KRW remains so weak. I think inflation risks in Taiwan are broader than judged by the CBC.

Subscribers Only

Region – inflation risks

Big oil price hikes matter, but have been seen before. It is the rise in chip prices, and the gap between surging trade surpluses and weak currencies, that is unprecedented. If fx markets don't price these developments, central banks and fixed income will have to do so instead.

Subscribers Only

Last week, next week

Two of the cycle themes in the region are the strength of the AI trade, and macro stability in China. These in turn form the context for the third: the impact of the Iran war. If that conflict, finally, is near some kind of resolution, market confidence around rate hikes could actually increase.