Subscribers Only

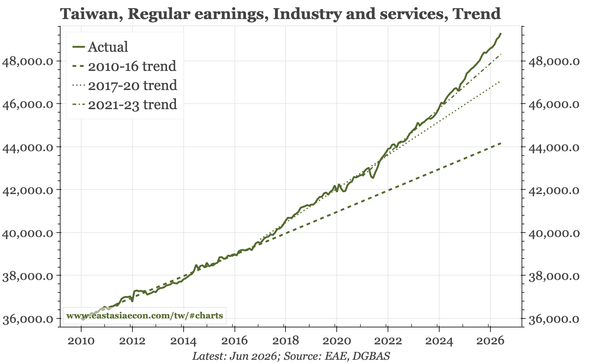

Taiwan – wage growth above 3%

Annualised regular wage growth in both manufacturing and services has been above 3% since 2024. In Q2 in manufacturing, it has been near 4%. The risk remains that the export cycle now slows, but TSMC's strong sales and elevated manufacturing overtime don't suggest that is happening yet.