Subscribers Only

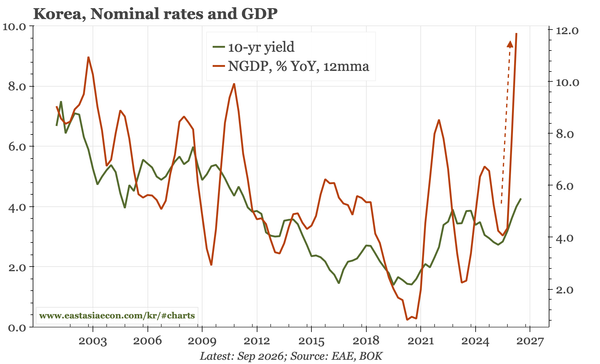

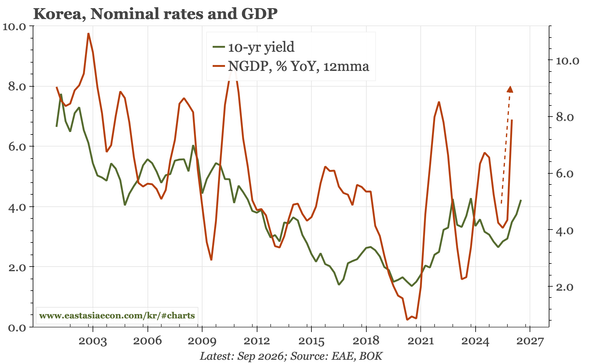

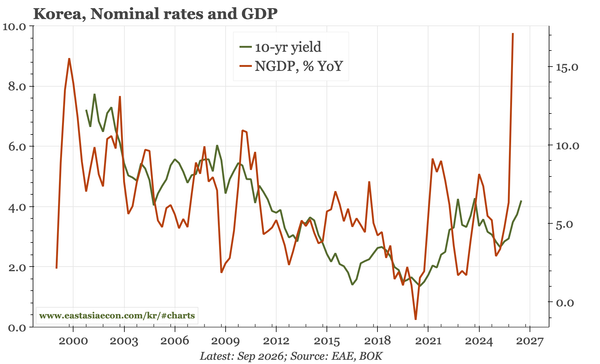

Korea – nominal growth nears 20%

Korea's real GDP growth in Q1 was solid, but nominal continues to be spectacular, rising almost 20% YoY for the first time in 30 years. Stronger nominal growth is typical of a commodity boom, and suggests more upside for rates than implied by inflation and real GDP alone.

Subscribers Only

Korea – mixed loan demand, firm PPI

In the Q3 loan officer survey, lower mortgage demand was offset by higher demand for other household loans. That points to the continuing risk of lending to finance stock purchases. The impact of the surge in equity market activity can also be seen in today's June PPI report.

Subscribers Only

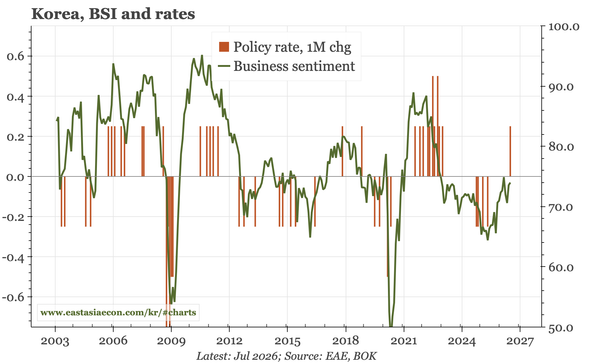

Korea – BOK more hawkish

As expected, the BOK hiked rates by 25bp today. The bank expects 2026 GDP growth to be "considerably" higher than the previous forecast of 2.6%, partly because it expects the cycle to broaden into domestic demand. That will in turn support inflation. Relative to market pricing, that feels hawkish.

Subscribers Only

Korea – rates to rise, but how hawkish?

The BOK discussion tomorrow should have two levels, the usual analysis of growth, CPI, housing, and the KRW, but also analysis of how the huge semi terms of trade shock affects medium-term economic prospects. The first justifies rate hikes. I think the second argues for more hawkishness still.

Subscribers Only

Korea – CA surplus of 20% of GDP still doesn't matter

The flow story behind KRW weakness has transitioned from overseas buying by domestic retail to domestic selling by foreigners. Two other factors help inform the exchange rate: correlation with the JPY and, perhaps, a BOK that is late in hiking given the huge acceleration in NGDP growth.

Subscribers Only

Korea – transition time for CPI

The sharp rise in inflation since March slowed in June, and the BOK expects a drop in July. But cost-push from the surge in semi prices is feeding into CPI, and the BOK also expects "expanding demand pressures" from the economic recovery to drive inflation from here.

Subscribers Only

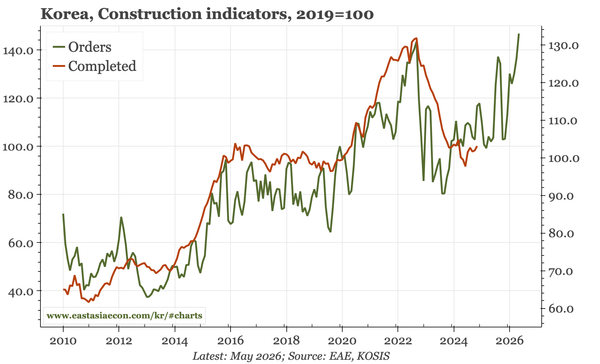

Korea – broader cycle, but mixed

There are signs of a broadening of the cycle, with construction past the worst, capex rising, and the labour market bottoming. However, while services activity has been strong recently, retail sales are still sluggish, and industrial production is going sideways.

Subscribers Only

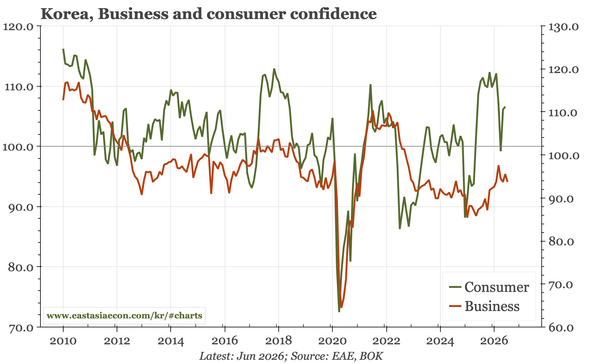

Korea – not quite K-shaped

Business sentiment is middling, and the gap between large and small firms looks K-shaped. However, consumer confidence is quite strong, and the BOK has argued that sector disparities aren't an issue for monetary policy. Falling oil prices do lessen inflation risk, but also boost GDP growth.

Subscribers Only

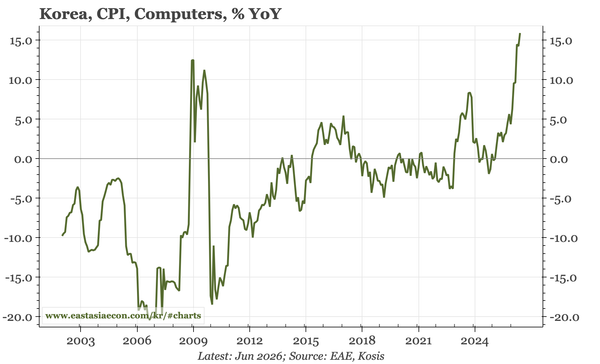

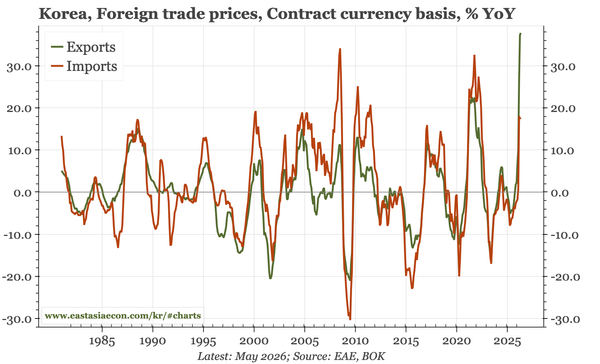

Korea – export prices still the standout

The sharp rise in import and export prices of recent months eased in May. But that leaves export prices at the highest level since the brief spike in 2008. That brings inflation for ROW and an income boost for Korea. With spot semiconductor prices still rising, neither trend is yet exhausted.