Public Post

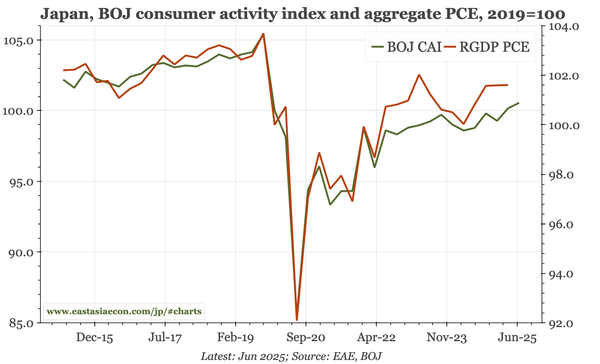

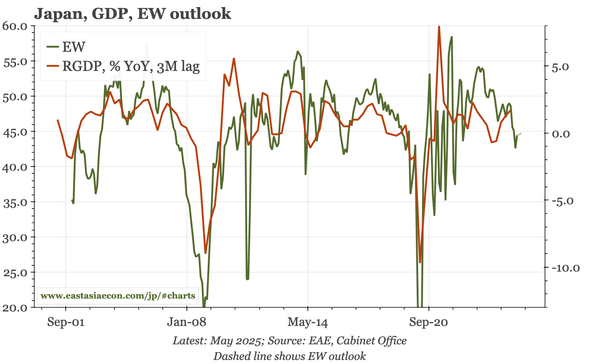

Japan – sentiment back to average

Sentiment in the Economy Watchers survey still points to slower GDP growth in 2H25. However, it now isn't particularly weak, improving in May back to the long-term average of the survey. That's probably not enough for the BOJ, but likely would be if Japan can now land a trade deal with the US.