Public Post

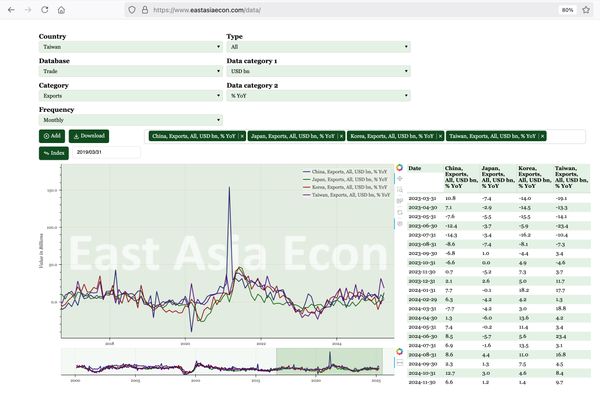

Asia – free resource for tracking East Asian economies

A new tool to view, chart and download macro data for the region