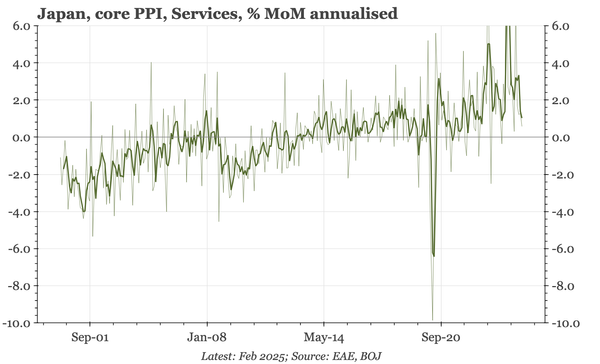

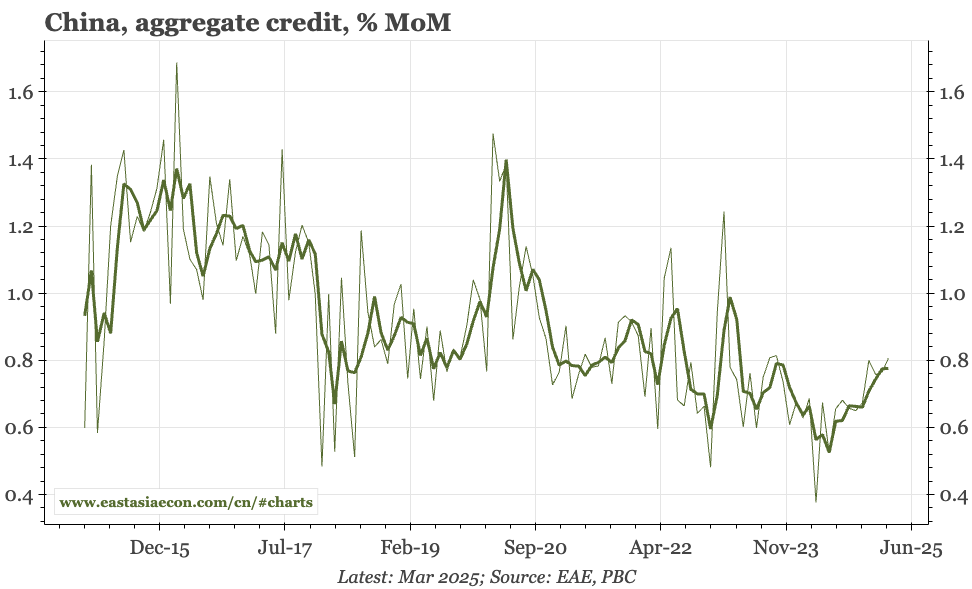

Subscribers Only

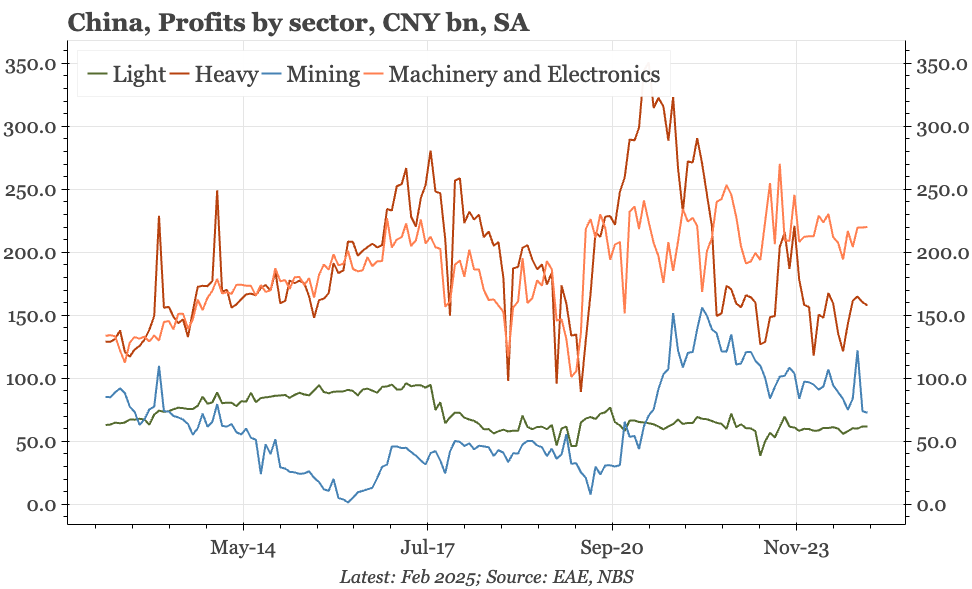

China – recovery in credit growth continues

Credit and monetary data continue to suggest the monetary squeeze of 2023 and 1H24 has ended. The significance of the rebound is offset by three factors: it isn't incorporating non-government borrowing; mortgage lending isn't rising; and definitional changes to M1.