Public Post

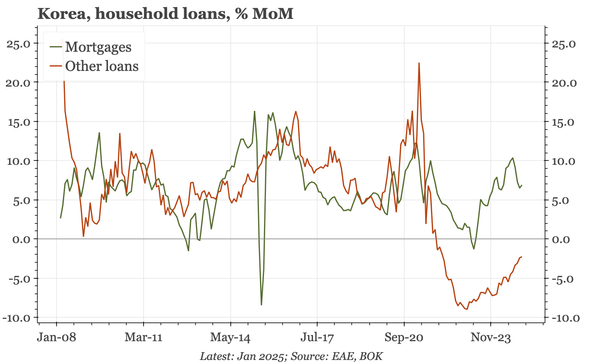

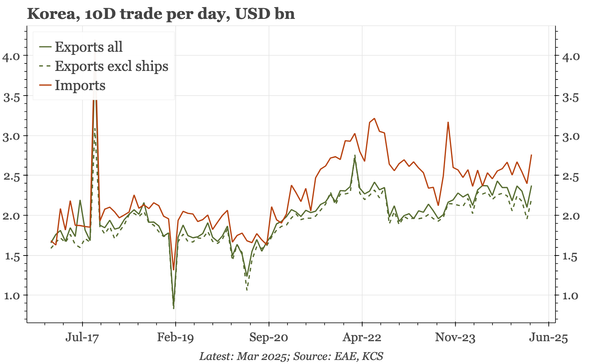

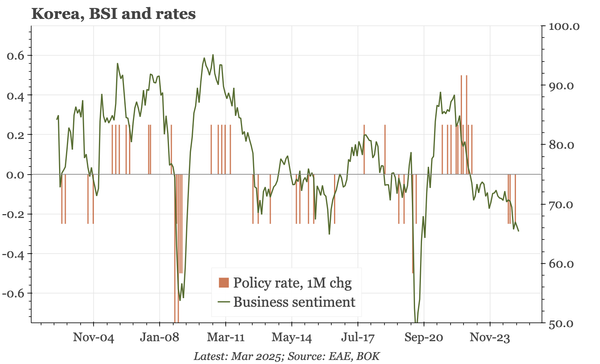

Korea – sentiment drops again

Business confidence remains extremely weak, and consumer confidence isn't a whole lot better. That being the case, the BOK is going to want to cut further, but inflation readings in the sentiment surveys aren't giving the all-clear for an aggressive loosening.