Public Post

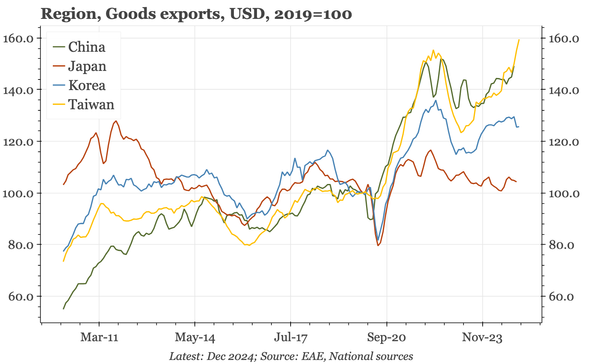

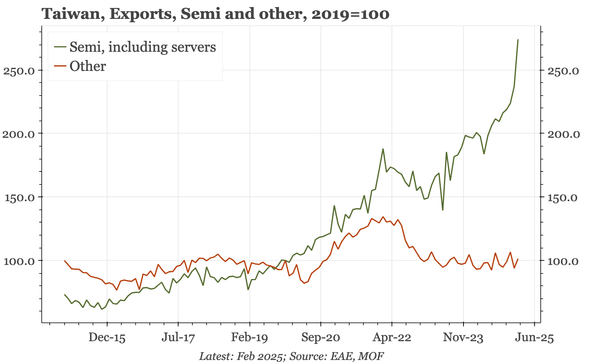

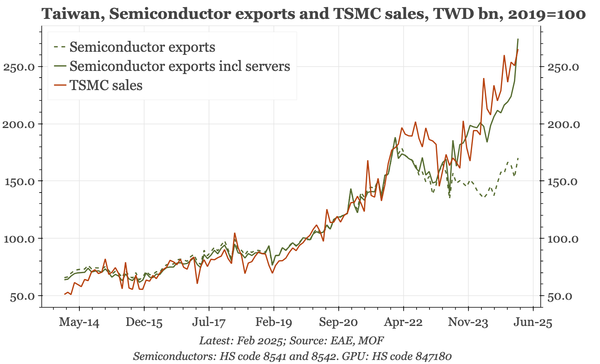

Taiwan – exports catch up with TSMC

The surge in exports this year isn't all front-loading and Chinese New Year. Through 2024, Taiwan's export data had been looking light relative to TSMC's sales. That gap has now been closed, meaning strong performance for TSMC can once again be thought of as implying macro strength for Taiwan.