Public Post

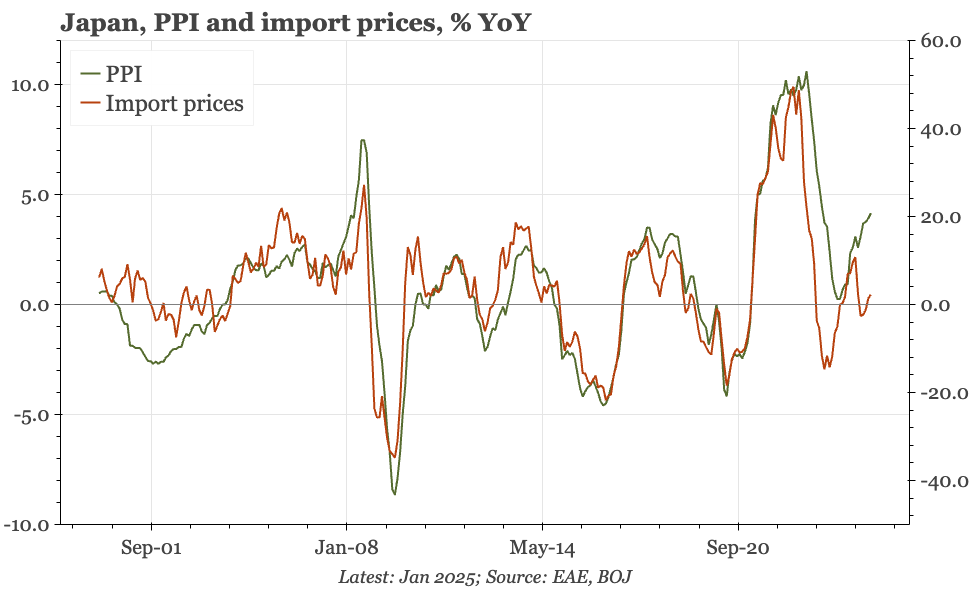

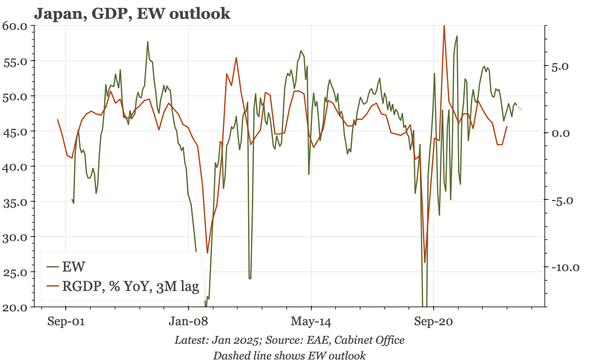

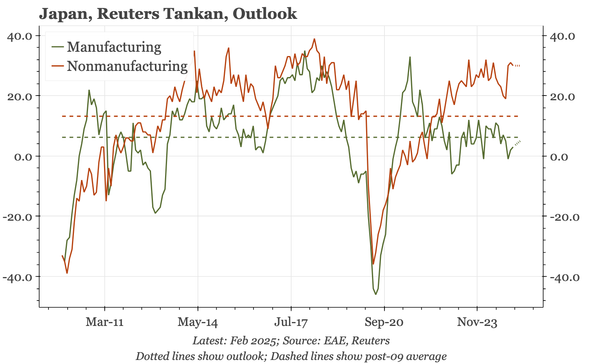

Japan – solid services Tankan

Services sector sentiment in the Reuters Tankan remained elevated in today's February survey. Manufacturing is much weaker, and that remains something to be watching given the extra downside risk from tariffs. But in terms of Japan's cycle, Q1 is likely to be another decent quarter.