Public Post

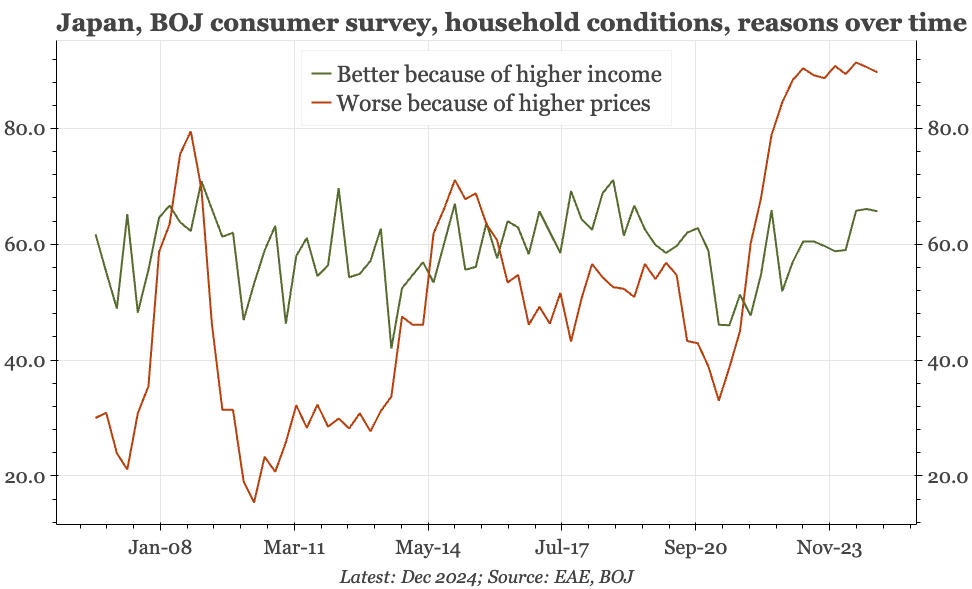

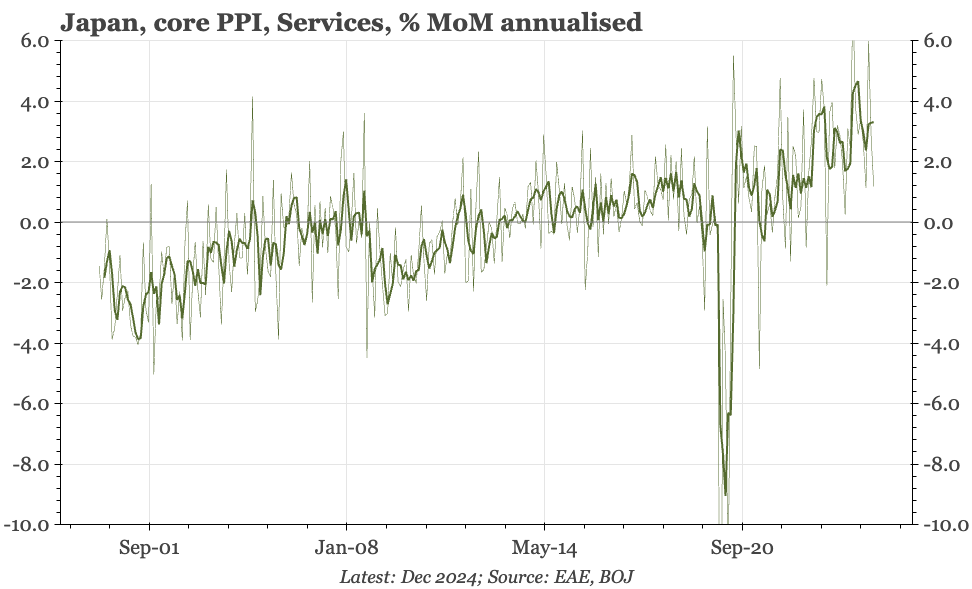

Japan – upstream services inflation still rising

SPPI inflation remains in an uptrend, and is now running around 3.5% saar. A few months ago the BOJ rejigged the data to include a breakdown by labour content, and that shows SPPI rising most quickly in high-labour industries. This will give the bank further confidence in its price-wage story.