Public Post

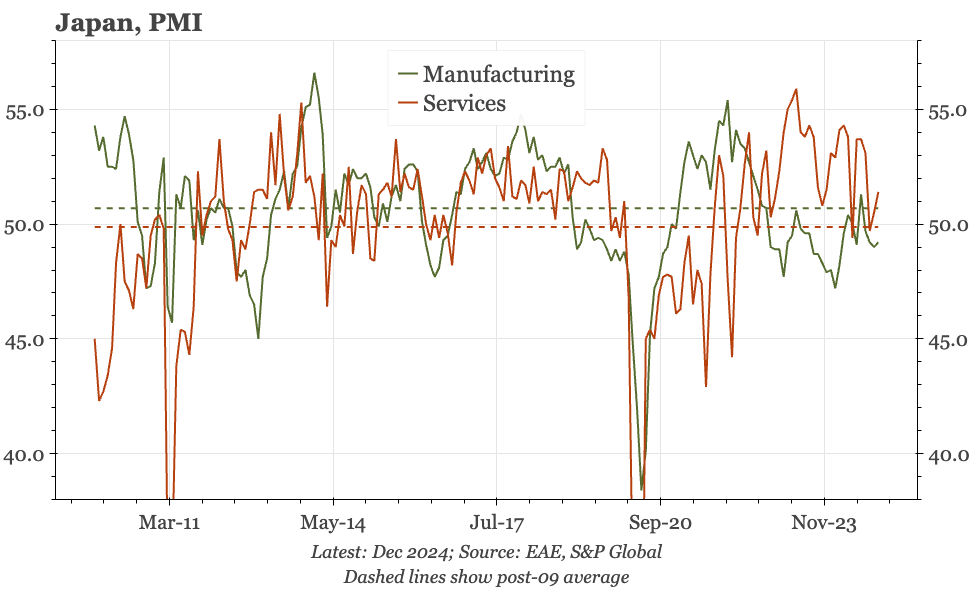

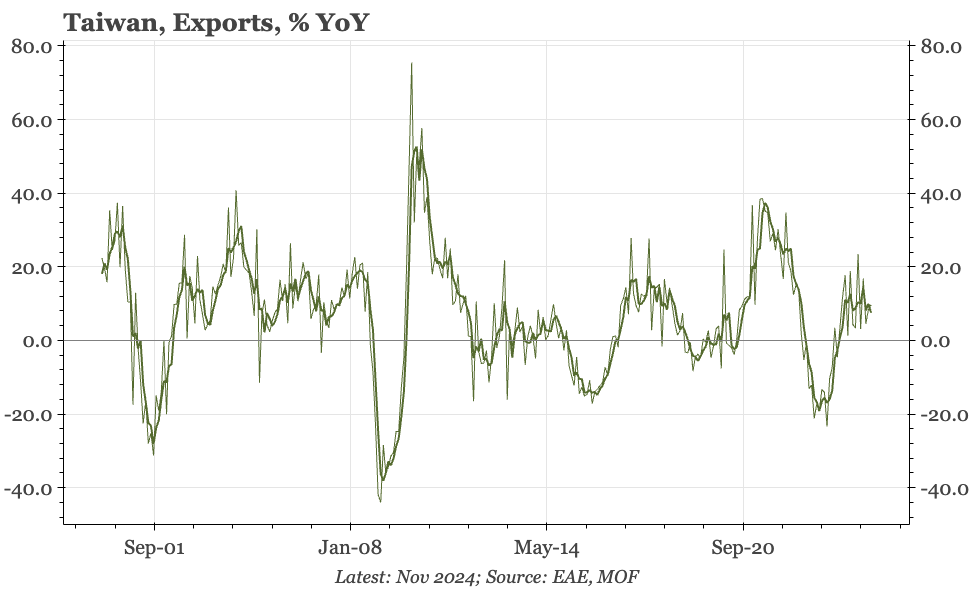

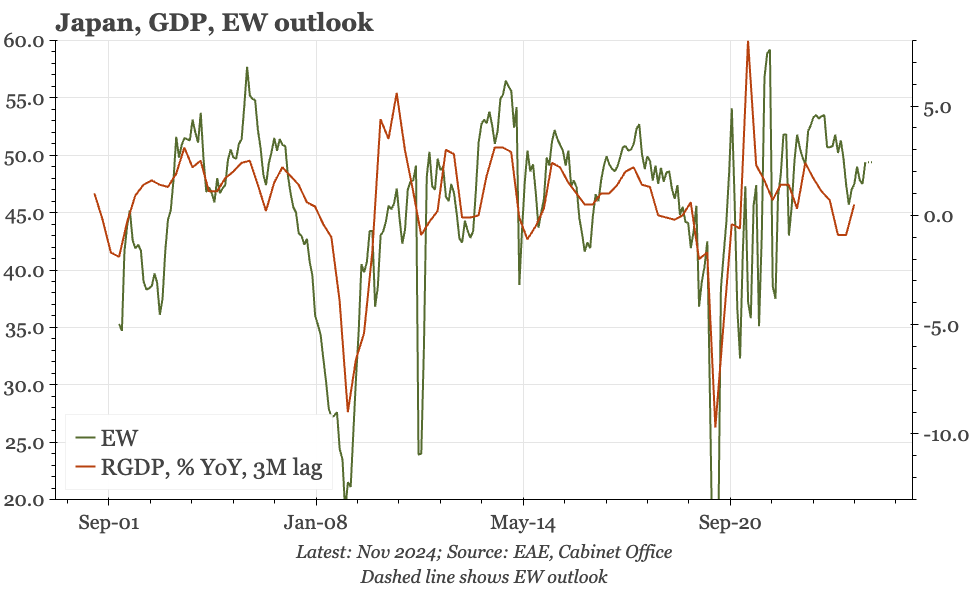

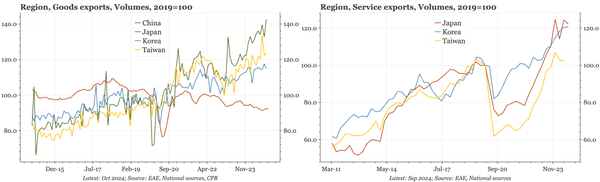

Japan – exports still sluggish

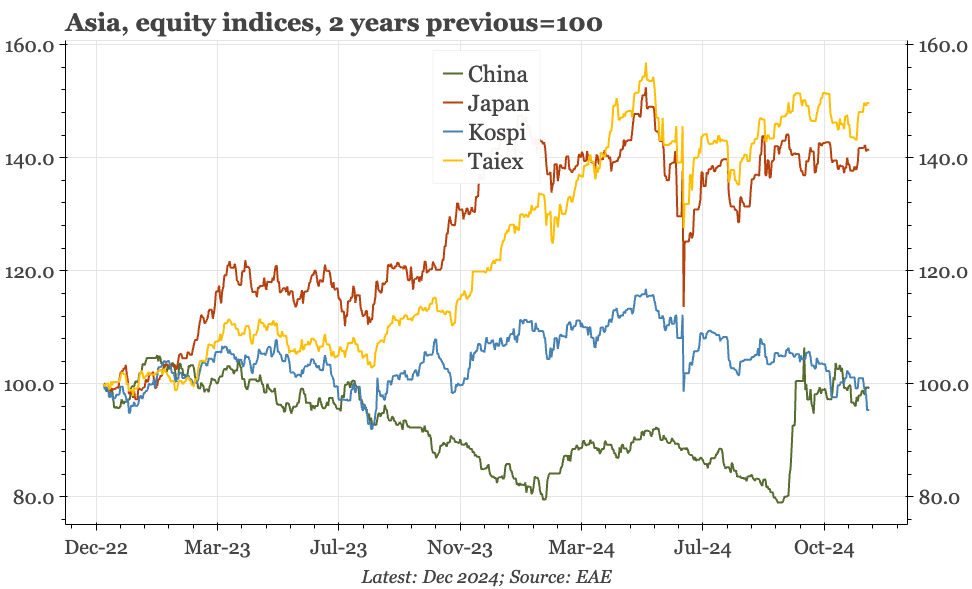

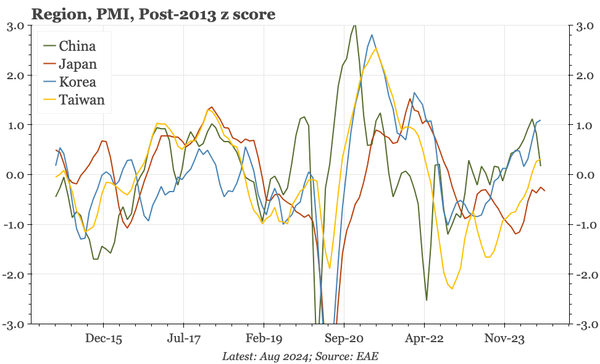

The weak JPY is having little impact on Japan's export performance. Yesterday's November data show export volumes still very sluggish, and continuing to underperform the rest of the region. Services are doing better, though even here, Japan isn't clearly outperforming.