Public Post

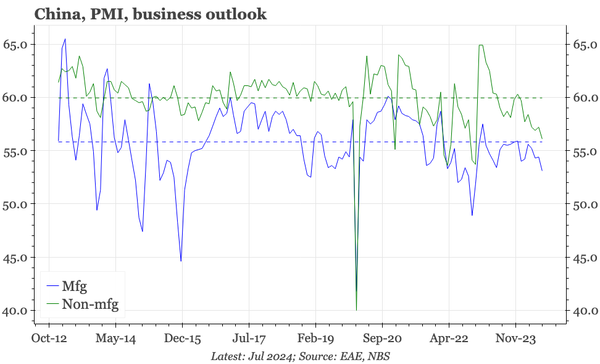

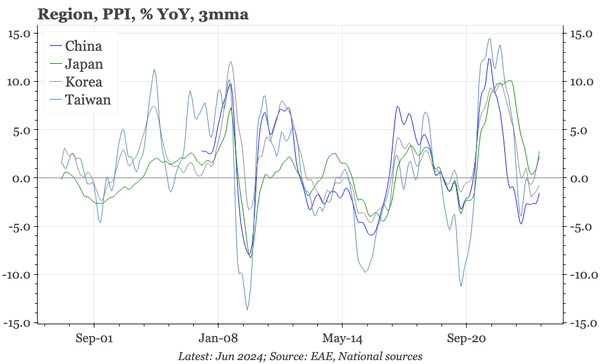

QTC: China – S&P/Caixin mfg PMI down too

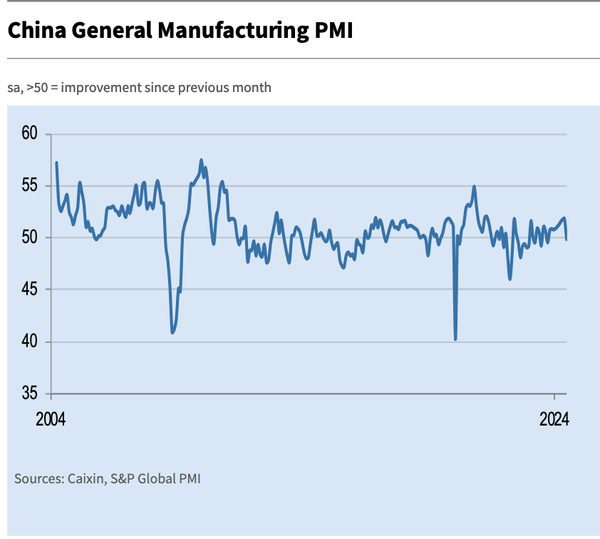

After the August PMIs, there's less room to think the economy is continuing to muddle through. Until now, the weakness of the official mfg PMI has been offset by strength in the Caixin version. Today's fall closes that gap, suggesting that even sectoral bright spots are now dimming.