Public Post

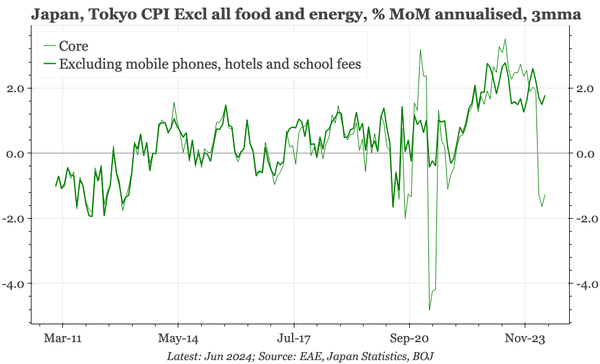

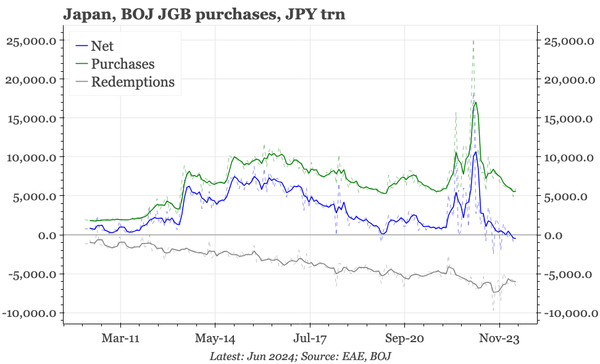

QTC: Japan – JGB net purchases falling

Latest data show that even before the BOJ makes its postponed decision about cutting gross new JGB purchases, on a net basis, the flow of new buying is already falling.