Subscribers Only

Last week, next week

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

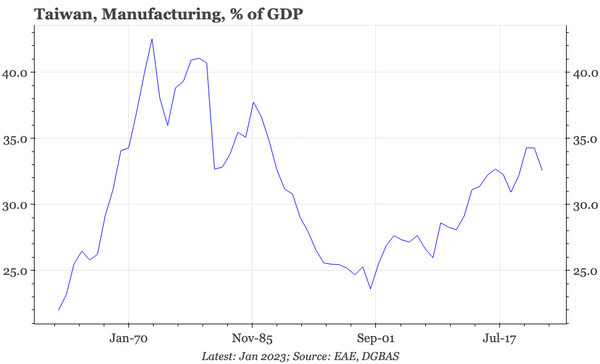

I suppose it isn't really surprising given exports and the trade balance, but the bounce back in the manufacturing share since the early 2000s is still rather remarkable.

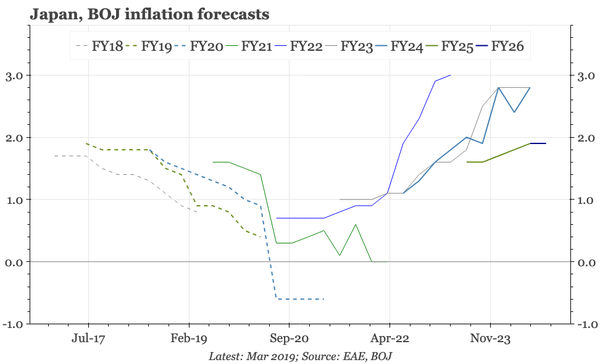

The BOJ didn't change policy, but once again, sounded incrementally more confident, issuing a FY26 core inflation forecast of +2.1%. That outlook makes policy rates still near zero look very low.

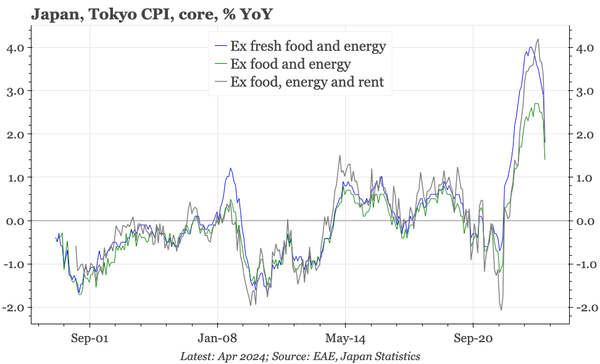

Inflation fell sharply in Tokyo in April. The macro story should mean some of the decline is temporary, but it complicates the more bullish story the BOJ wants to tell

Q1 GDP was solid, but the weakness in business sentiment in April makes us feel economic momentum is incrementally weaker. The consumer survey showed price expectations remaining elevated, which fits with weekly price data showing no big slowdown in food or energy price inflation through April.

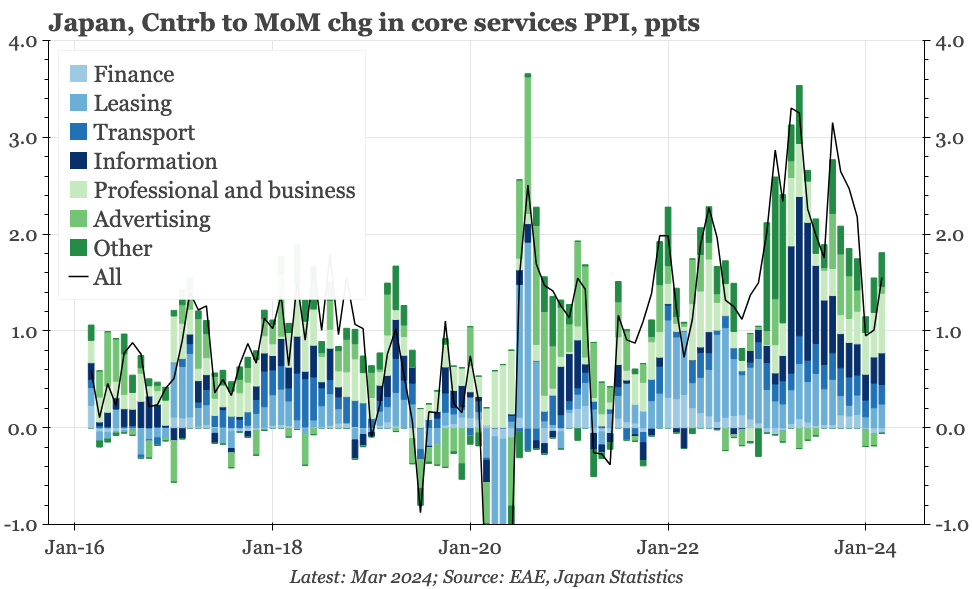

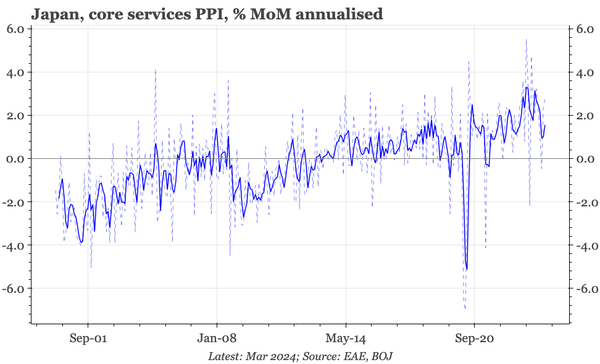

While not yet certain, it looks like the recent fall in services PPI might be bottoming. That is important for a BOJ that will want to sound more hawkish given rising $JPY.

The NBS's series for 10-day industrial prices 10 suggests overall PPI has stopped falling, though with big differences depending on the commodity.

The drop in services PPI inflation since late 2023 has threatened the BOJ's wage-price narrative. It is important that March data suggest a floor.

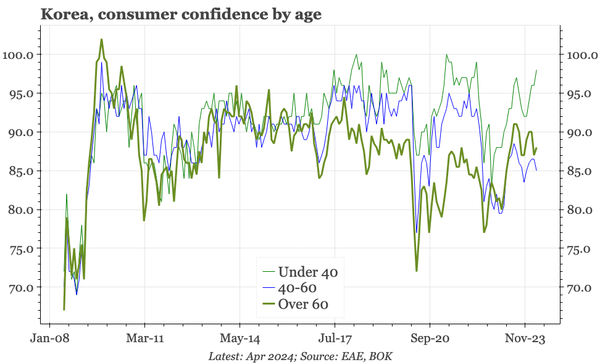

Overall consumer confidence is at the average of the last 20 years. But by age, young people are more optimistic than usual, 40-60 year olds much less so.

Unusual domestic strength got Taiwan through the '23 export recession. Exports are now recovering, but consumption is still holding up. That's good news for the economy, bad news for the central bank.

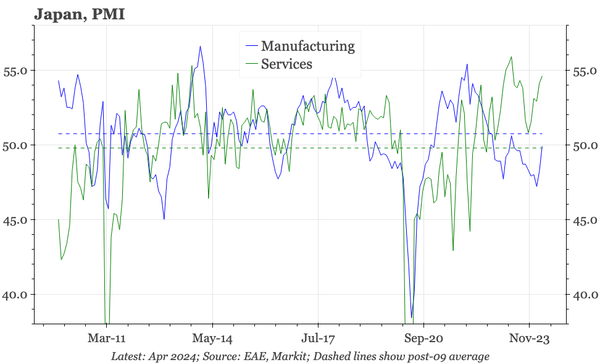

Export volumes haven't responded to JPY weakness, but profits have. That's feeding into manufacturing sentiment, which is better than history, and better than the rest of the world. With services sentiment also strong, the BOJ can continue to argue the macro cycle is warming up.

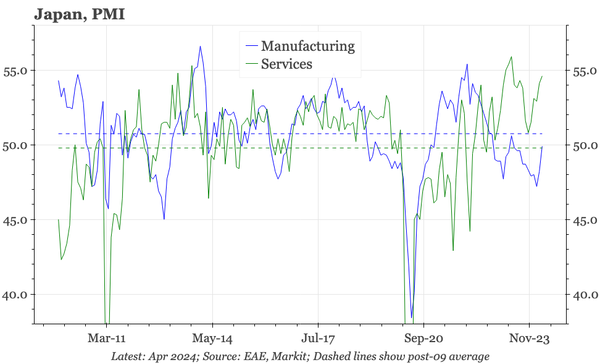

The flash services PMI remained strong in April, and the mfg PMI lifted towards 50. S&P also reported the survey showing "intensifying price pressures". Japan is heating up.

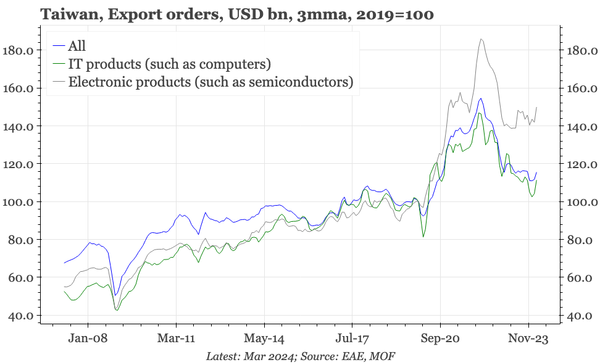

There was a bit of pick-up in IC orders in March, but not by enough to lift total orders, which have yet to regain 2023 levels. The export recovery remains sluggish.

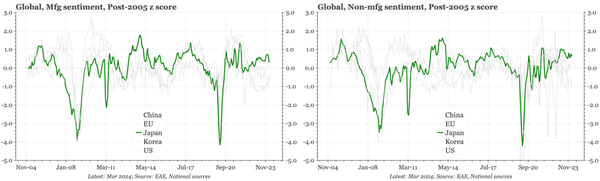

Relative to history, business sentiment in Japan is the strongest among most major economies in both mfg and non-mfg. That's only been seen once before.

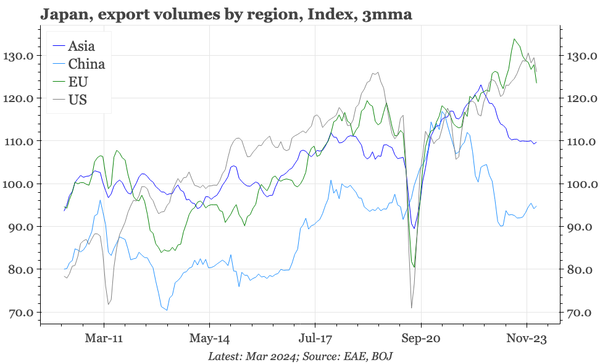

Japan's export volumes to China are still almost 20% below the peak. Nor surprising, when the only strength in China's imports is primary goods and semi.

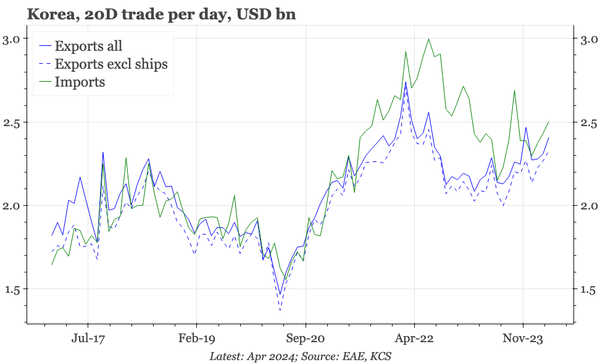

Korean exports are recovering. But at 5-10% YoY, growth doesn't yet look strong enough to offset weakness in the domestic economy.

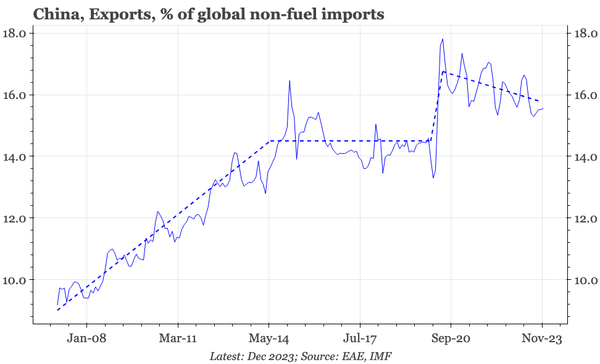

Cyclically, China's exports are improving, but the lift doesn't look particularly strong yet. Structurally, too, recent export performance has been a little underwhelming.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

There's quite a contrast between the sense of domestic manufacturing capex boom, and the lack of any rise in imports of capital goods outside of semi.

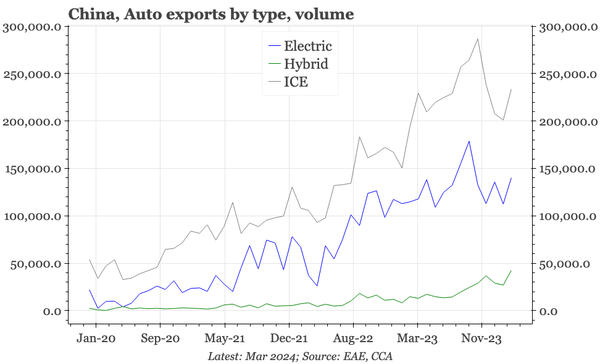

There are many reasons to expect a new wave of Chinese EVs to the world, but the last one arguably peaked in 2022, and another has yet to appear.

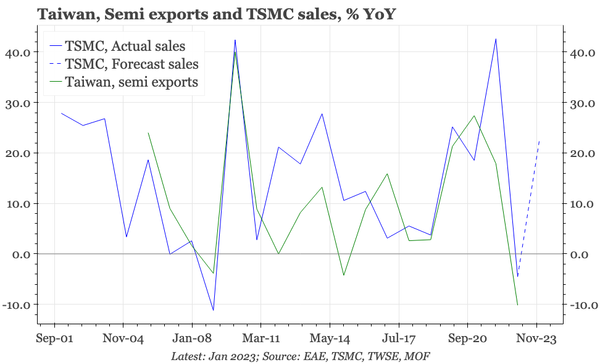

TSMC yesterday was less bullish on semi as a whole in 2024, but its own unchanged sales outlook still suggests a strong year for Taiwan exports

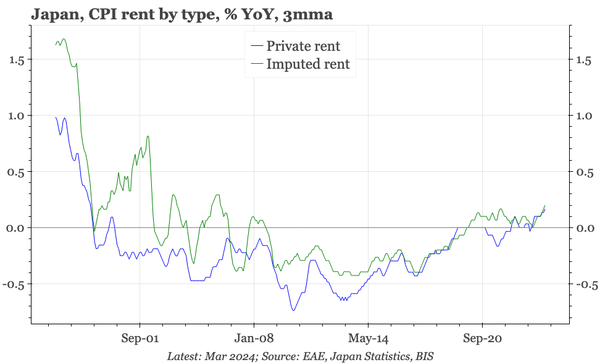

It still isn't even at 0.2% YoY, but rental CPI is now rising the fastest since the 1990s, which is pulling up imputed rent too. Together, they account for almost 20% of the basket.

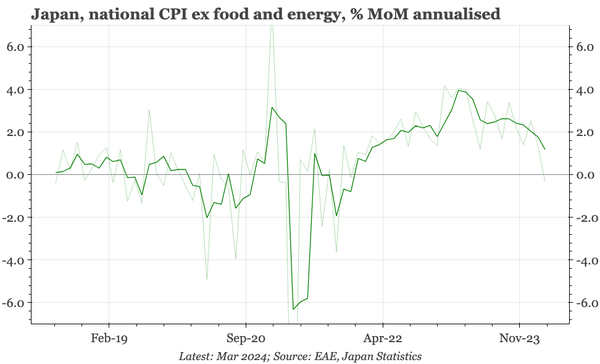

We estimate that sequential core CPI inflation turned negative in March. The macro backdrop suggests that should be temporary, but uncertainty about the real strength of the domestic inflation dynamic constrains the BOJ's ability to respond to the unhelpful weakness in the JPY.

It is remarkable, given the big mortgage rate cuts and everything else thrown at the property market, that buyer sentiment just gets worse and worse.

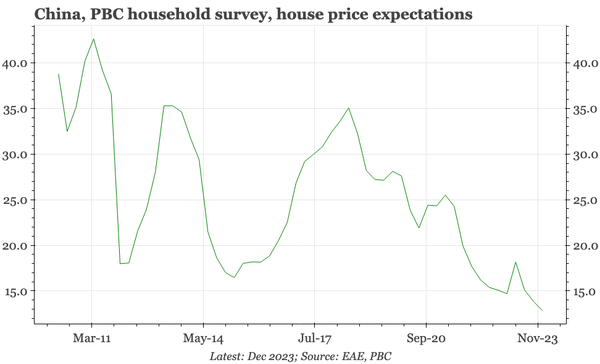

The belated release of the PBC's consumer survey continues to show falling price expectations, and so hint at rising real rates.