Public Post

East Asia Today

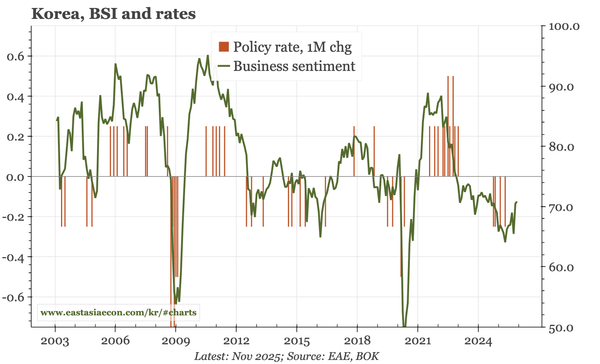

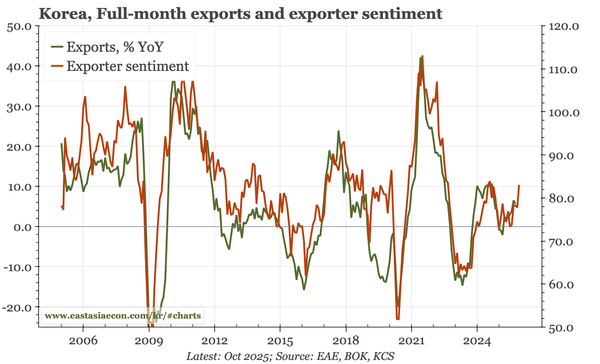

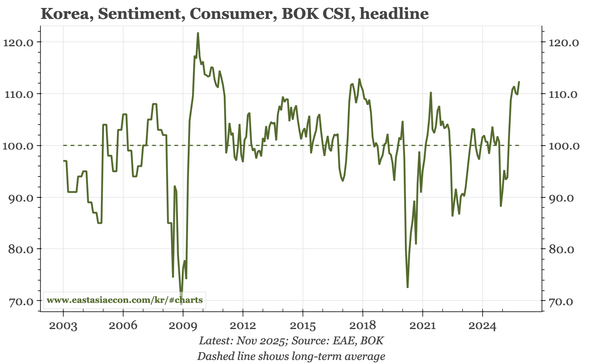

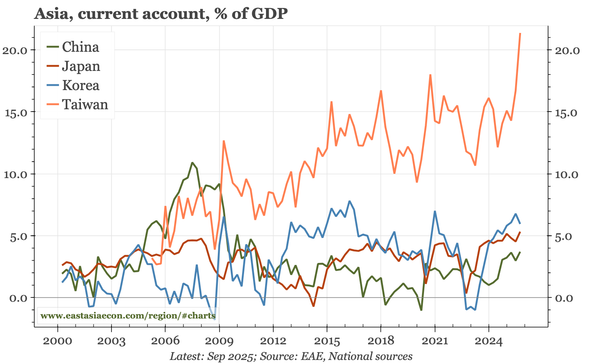

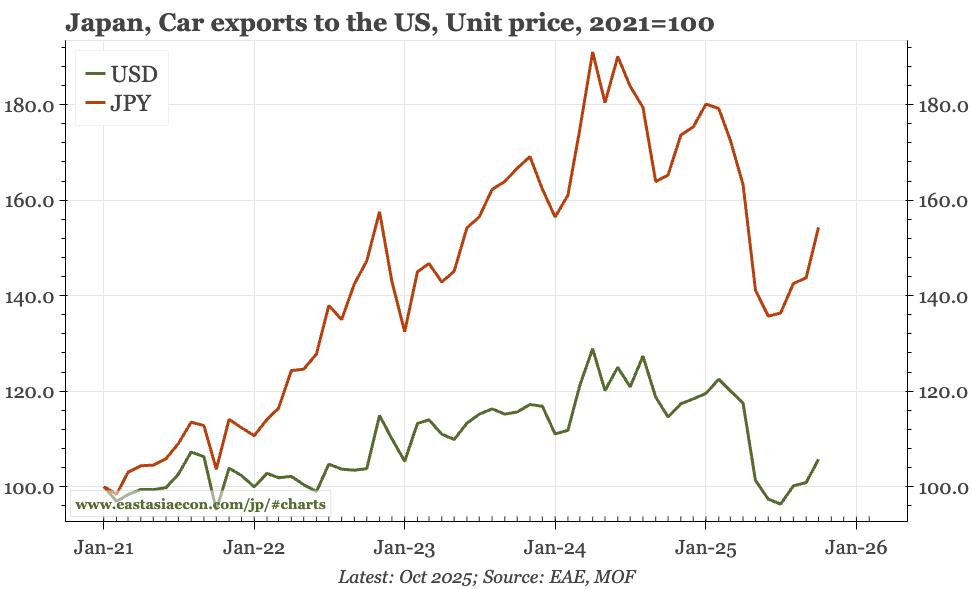

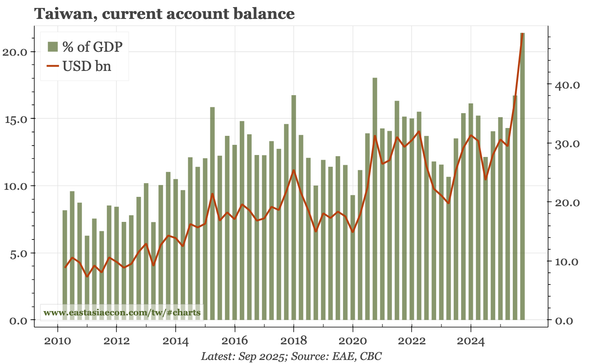

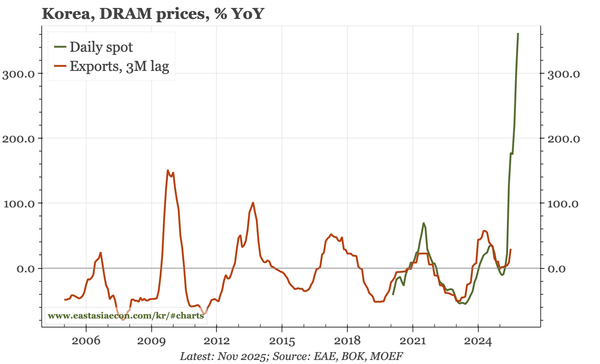

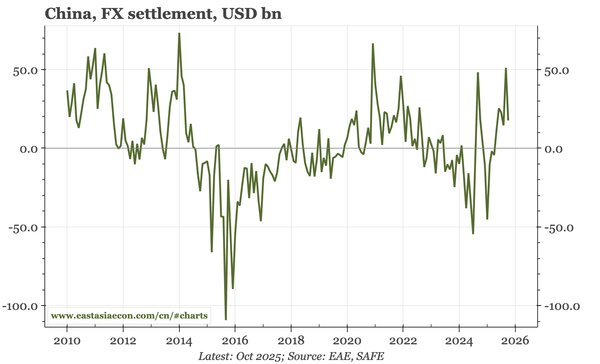

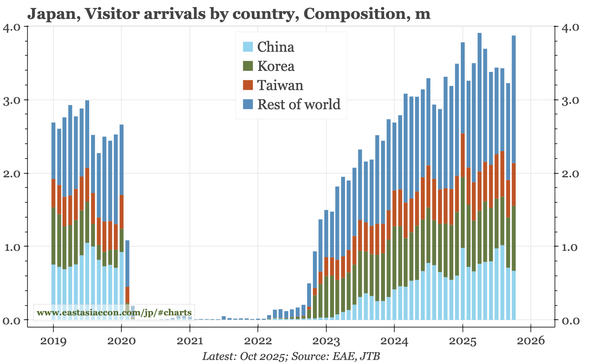

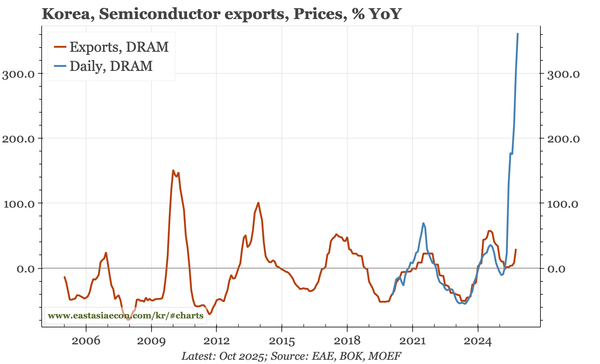

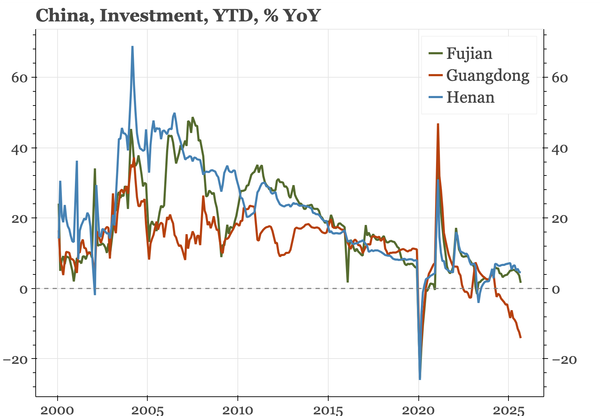

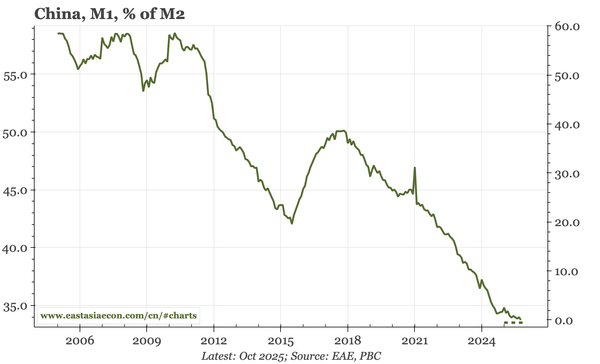

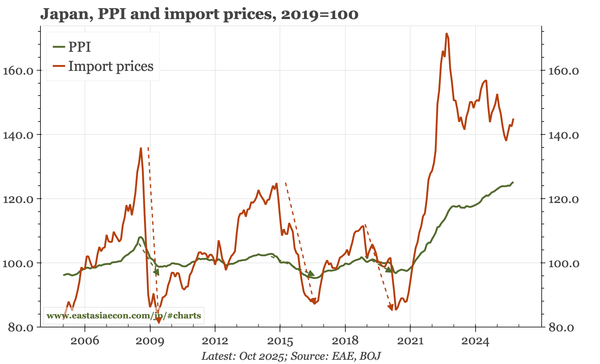

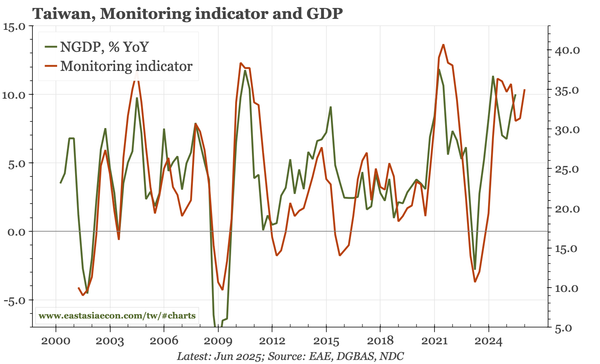

The big event today was the BOK meeting. The bank was a bit more constructive on the outlook, but data that was separately released show labour market conditions remaining weak. Elsewhere, profits in China are flat-lining, exports in Japan aren't dropping, and macro data in Taiwan remain strong.