Public Post

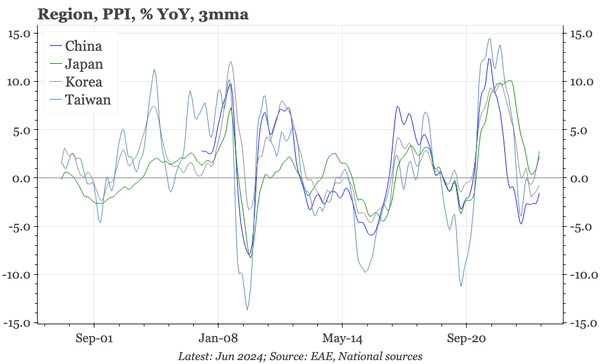

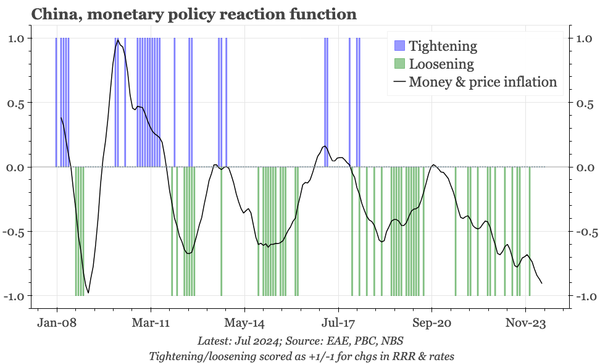

QTC: China – industrial prices stable despite property

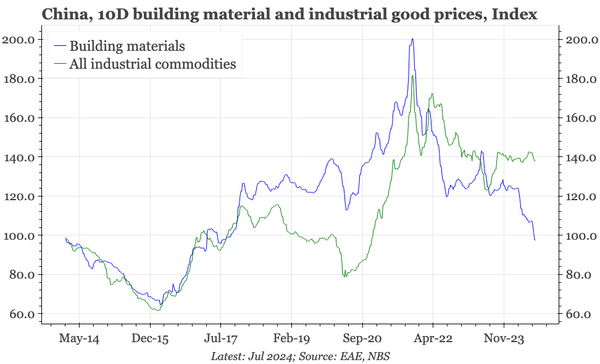

The collapse in property market activity is showing up in sharply lower prices for building materials: they've now fallen by 50% from the peak. But overall industrial prices haven't fallen in the same way, and continue to point to PPI inflation of around 0%.