Public Post

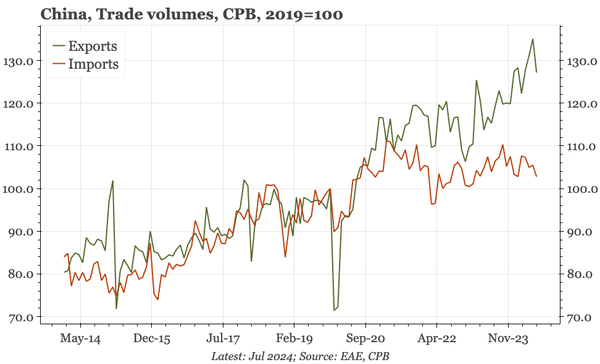

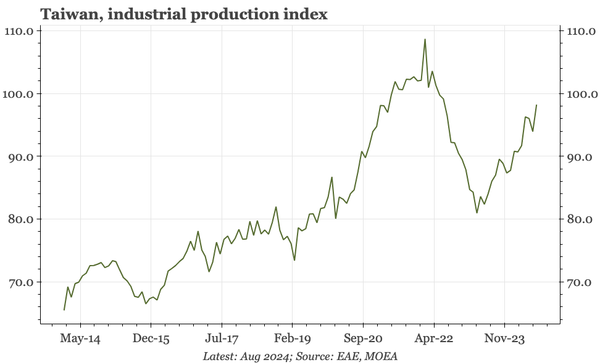

Asia – the big shift in exports

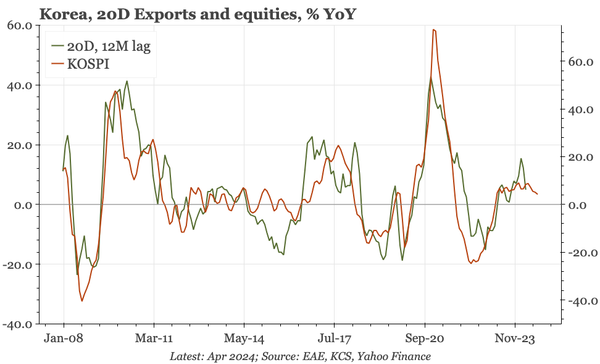

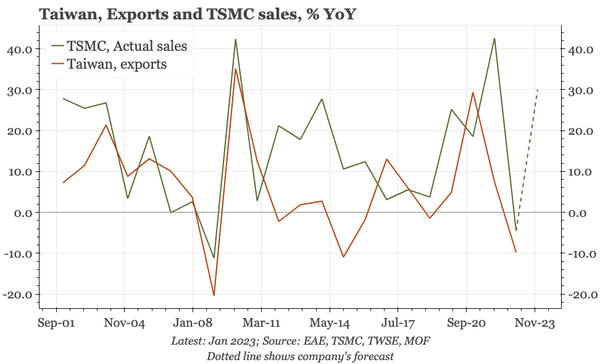

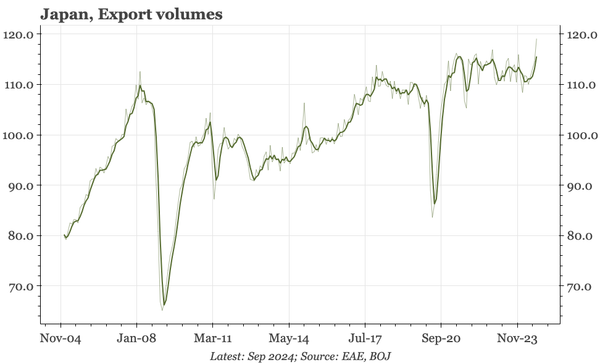

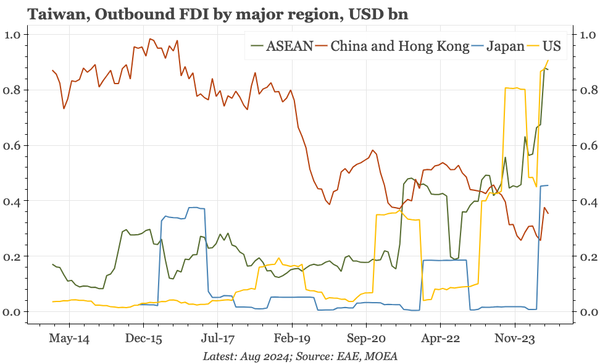

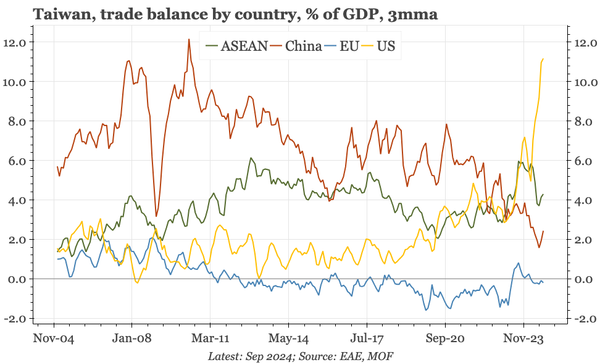

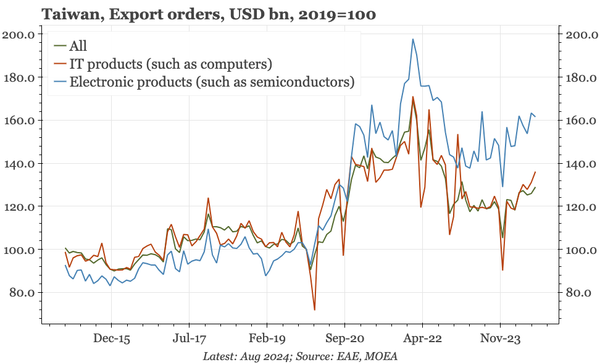

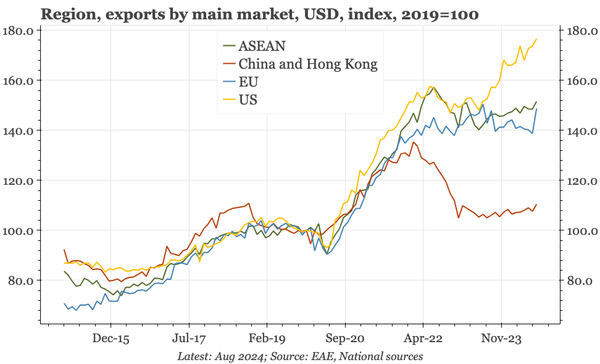

The export data across the region continue to show an enormous shift in the direction of trade. Exports to China haven't recovered following the post-pandemic slump. Where there is growth, it is all about the US.