Public Post

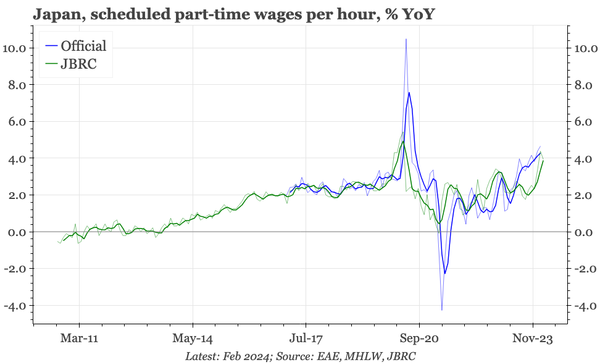

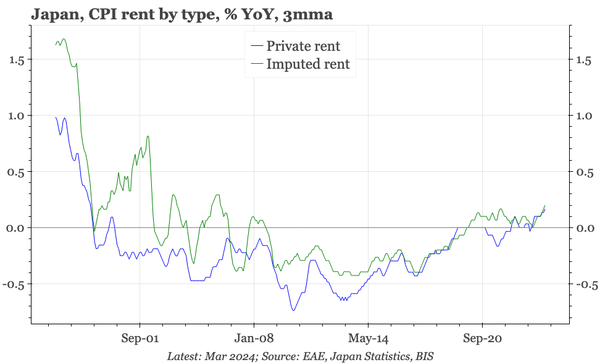

Japan – finally, some rental inflation

It still isn't even at 0.2% YoY, but rental CPI is now rising the fastest since the 1990s, which is pulling up imputed rent too. Together, they account for almost 20% of the basket.