Subscribers Only

East Asia Today

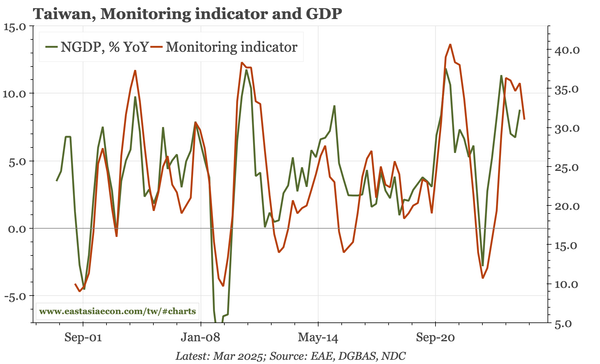

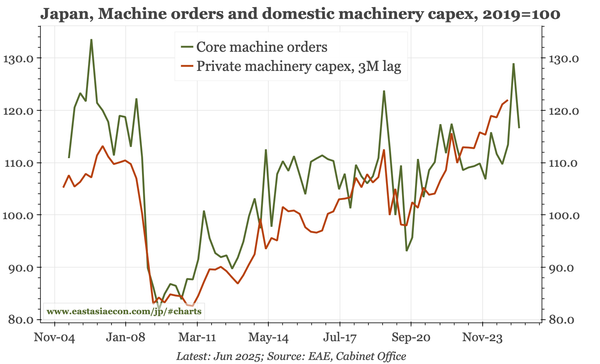

Quite a lot today, starting with a longer thematic piece on the outlook for Japanese consumption. In terms of the cycle, there's June machine orders and July exports for Japan, and July export orders and Q2 BOP data for Taiwan.