Public Post

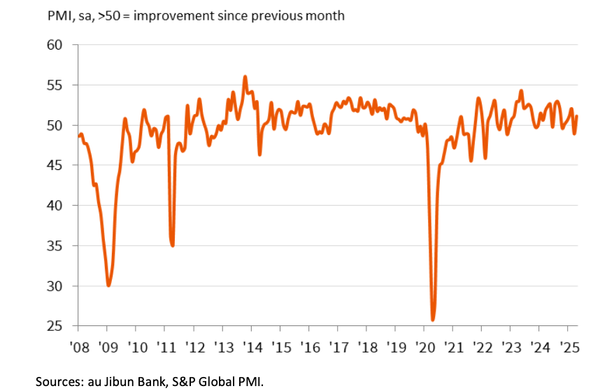

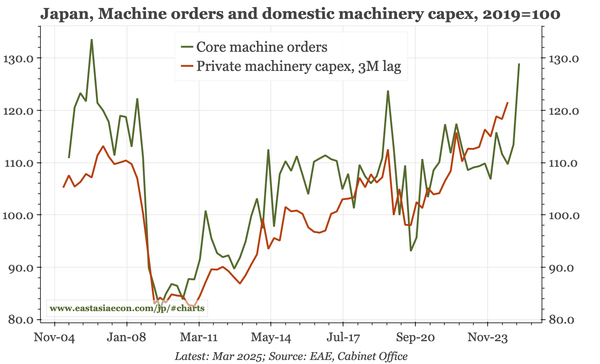

Japan – strong orders, weak sentiment

March machine orders surged, which could be tariff-related, but the strength was in domestic not foreign orders. Anyway, it seems unlikely to last, with today's flash May PMI repeating the downbeat message of the EW, with business confidence "the second-lowest recorded" since 2020.