Subscribers Only

East Asia Today

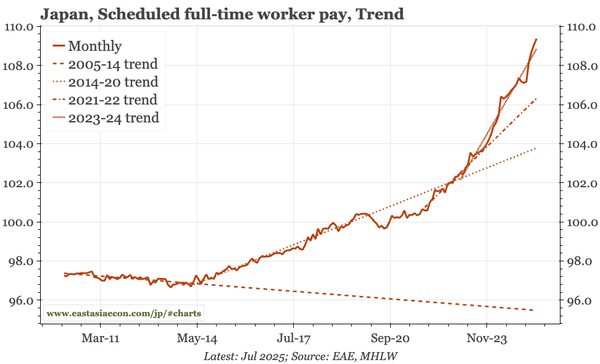

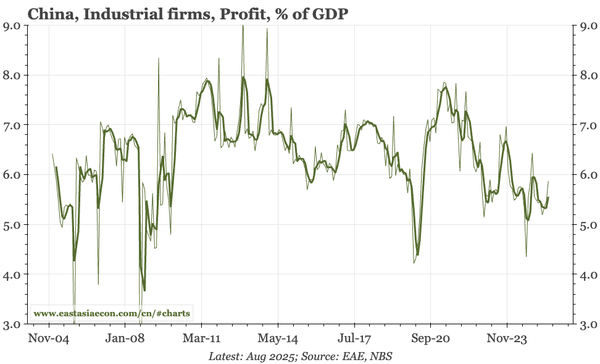

A quiet day for domestic macro today. The only data release was Saturday's profits data in China. In Japan, MPC member Asahi Noguchi gave a speech, in which he made a couple of interesting points, but governor Ueda's speech at the end of the week will obviously matter more.