Subscribers Only

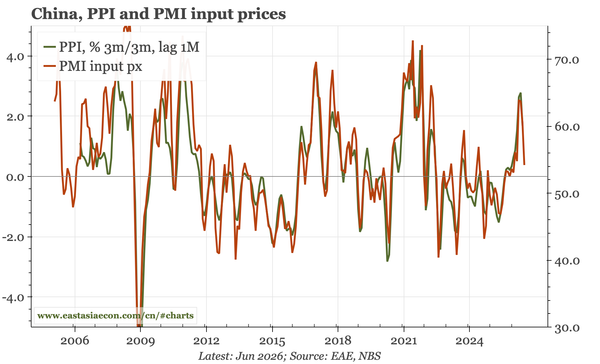

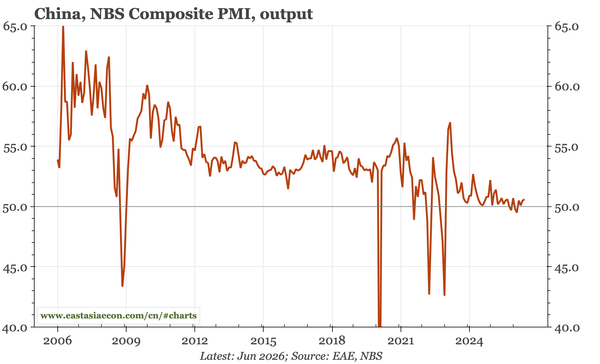

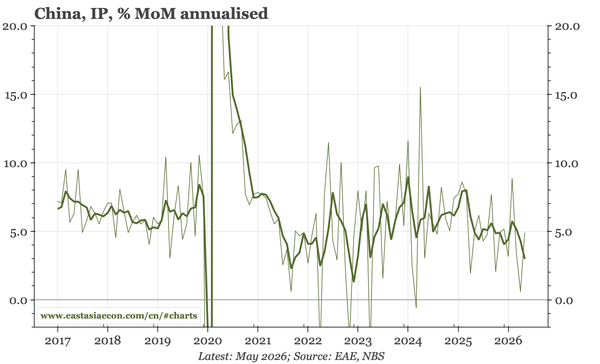

China – PMIs down again

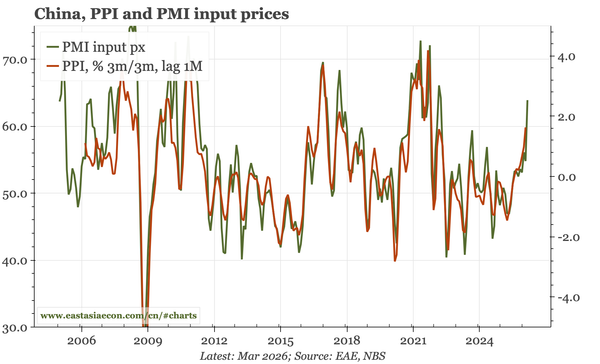

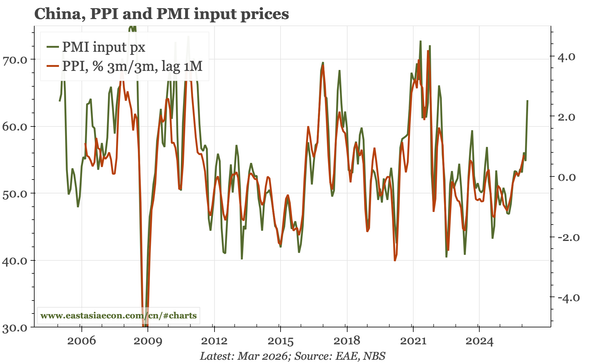

The across-the-board weakening of the official PMIs will reinforce cycle pessimism, with px indicators point to an end of the recent upturn in PPI inflation. The likelihood of renewed monetary easing is growing, but detailed data – and the Politburo statement – suggest only incremental change.