Subscribers Only

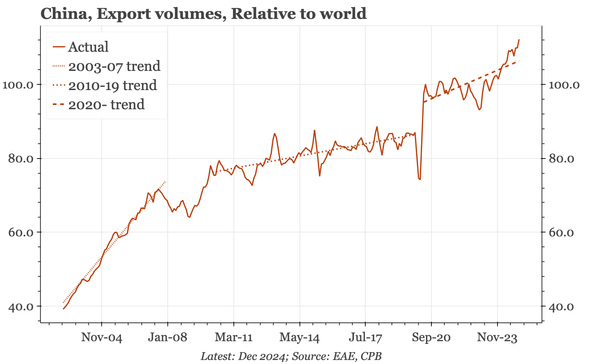

China – import ratio now the lowest since the 1990s

Exports through March were solid, but not so strong as to suggest big front-loading. The real standout is the import ratio dropping to a new post-1990s low. The trade surplus upsets Trump. Equally though, weak imports limit China's appeal as a market for others looking for an alternative to the US.