Subscribers Only

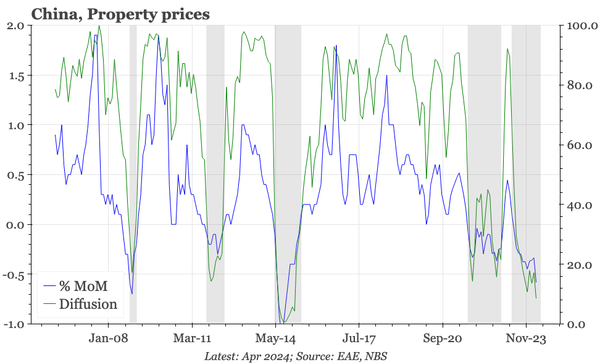

China – property down yet again

Property remains in a deep funk, and while the government talks confidently about a successful transition to new growth engines, all the policy action indicates increasing concern that real estate remains so weak.