Public Post

Region – Back to the Future: East Asia and Trump 2.0

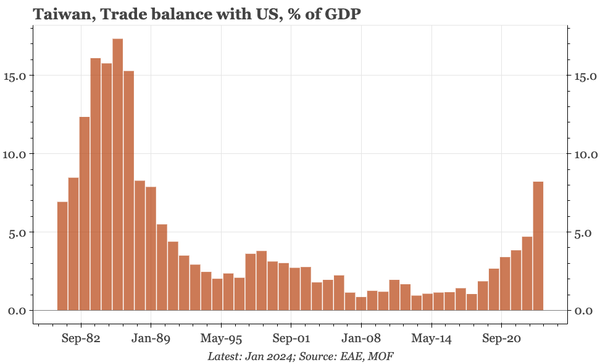

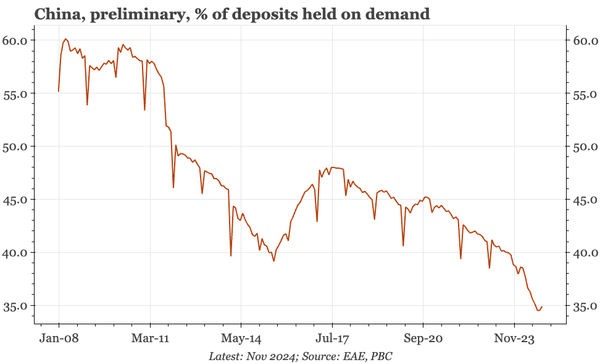

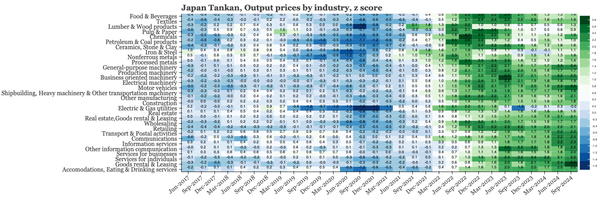

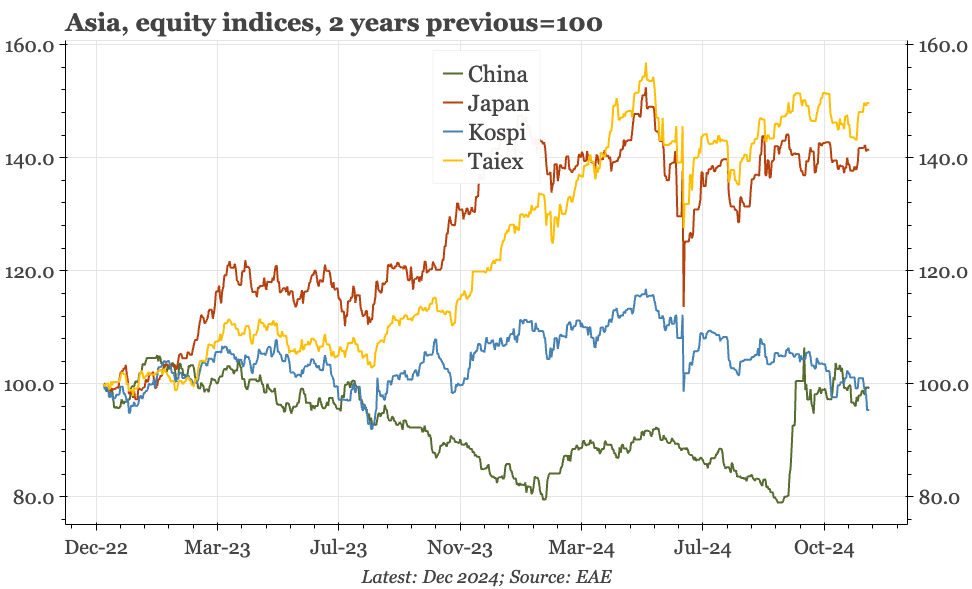

The film Back to the Future came out in 1985, and with inflation in Japan, deflation in China, and big external surpluses once again, there are all sorts of regional economic themes that have echoes of then. Here's a podcast in which I discuss the implications, with links to the underlying research.