Subscribers Only

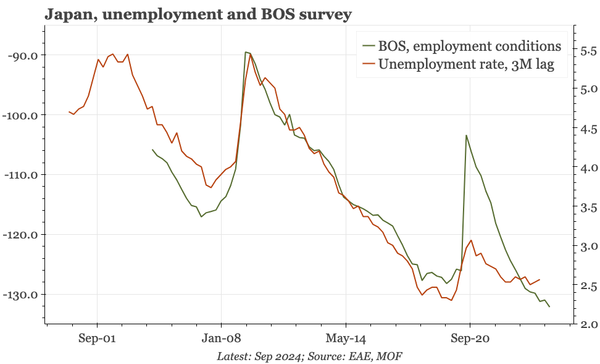

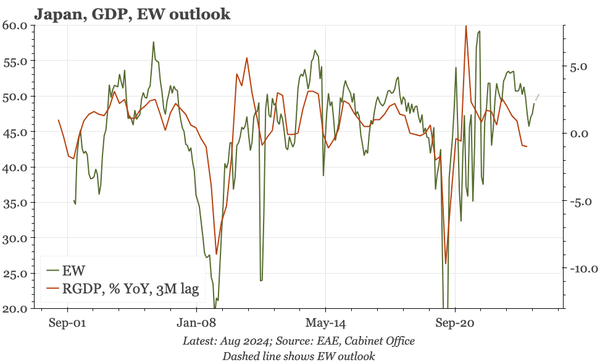

Japan – cold feet

The BOJ's stance now has two clear dimensions. One, as before, is its constructive view of the domestic economy. But now there's also an explicit concern about US growth. As long as one offsets the other, the BOJ has time. However, if the US soft lands, then the BOJ will have ground to make up.