Subscribers Only

Last week, next week

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

The platform for tracking and understanding East Asia macro

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

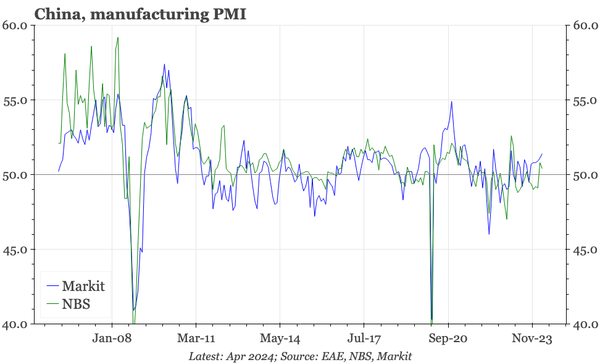

It has taken a long time, and still isn't powerful, but recovery is finally being seen in the manufacturing PMIs. At the same time, non-manufacturing isn't slowing down much, and price pressures are picking up again. Taiwan doesn't look like an economy where policy is too tight.

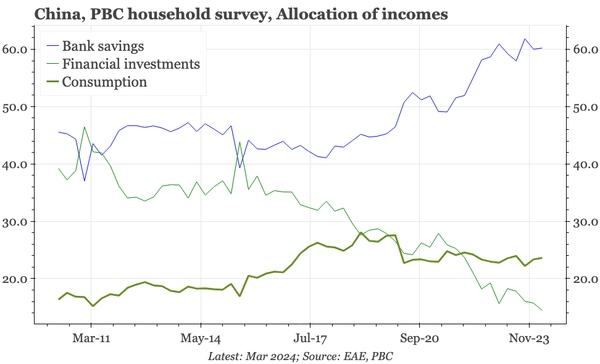

The PBC's Q1 depositor surveys show that it is less consumption sentiment per se that is weak than consumer price and property expectations. In this context, the news that the Politburo is studying ways to reduce property inventories is potentially significant for the macrocycle this year.

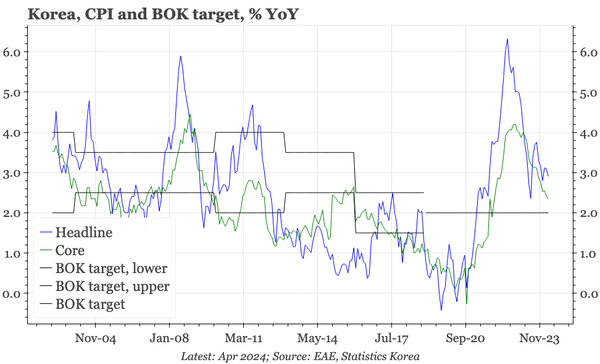

Core inflation looks controlled, but headline continues to run around 3%. Leading indicators don't suggest that goods prices pressures are about to subside quickly. One reason is the weakness of the KRW and as a result, our model still isn't flashing the risk of a near term change in policy.

The boxes in the BOJ's full outlook report present a clear explanation of the bank's confidence around wages and prices, and hint at the policy implications.

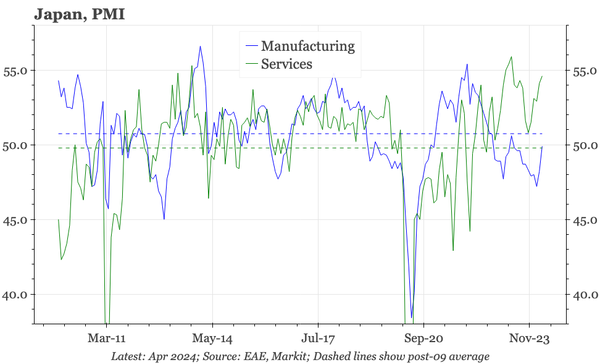

The mfg PMIs continue to suggest the industrial cycle, in terms of activity and pricing, is through the worst. For now, though, the strength is mainly in exports. As a growth driver, that shouldn't be dismissed, but the upturn would feel more sustainable if domestic indicators were improving more.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

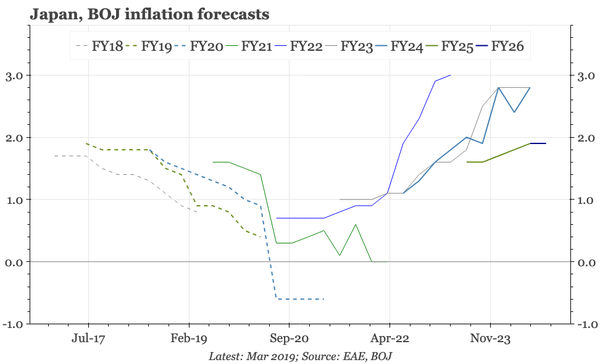

The BOJ didn't change policy, but once again, sounded incrementally more confident, issuing a FY26 core inflation forecast of +2.1%. That outlook makes policy rates still near zero look very low.

Q1 GDP was solid, but the weakness in business sentiment in April makes us feel economic momentum is incrementally weaker. The consumer survey showed price expectations remaining elevated, which fits with weekly price data showing no big slowdown in food or energy price inflation through April.

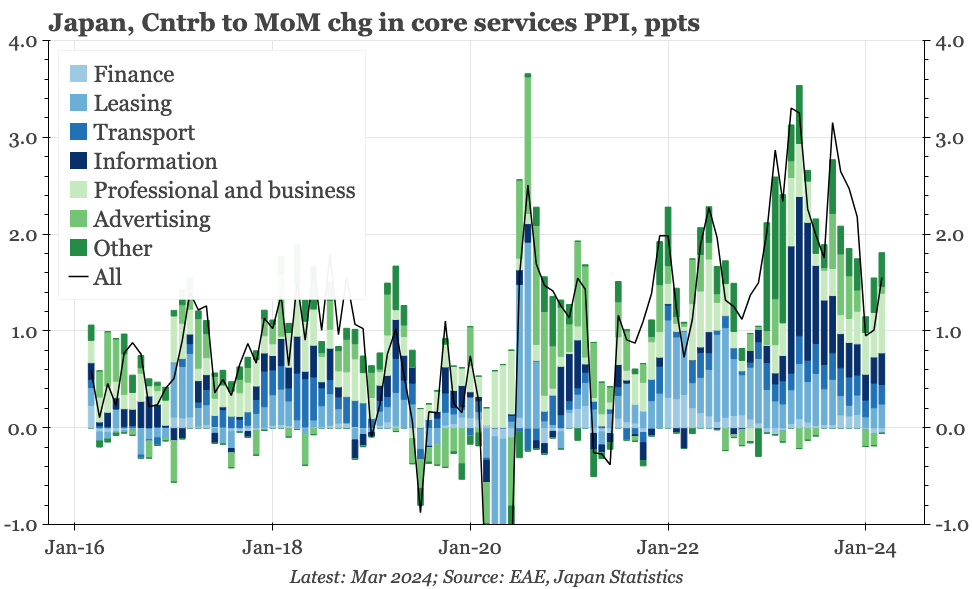

While not yet certain, it looks like the recent fall in services PPI might be bottoming. That is important for a BOJ that will want to sound more hawkish given rising $JPY.

Export volumes haven't responded to JPY weakness, but profits have. That's feeding into manufacturing sentiment, which is better than history, and better than the rest of the world. With services sentiment also strong, the BOJ can continue to argue the macro cycle is warming up.

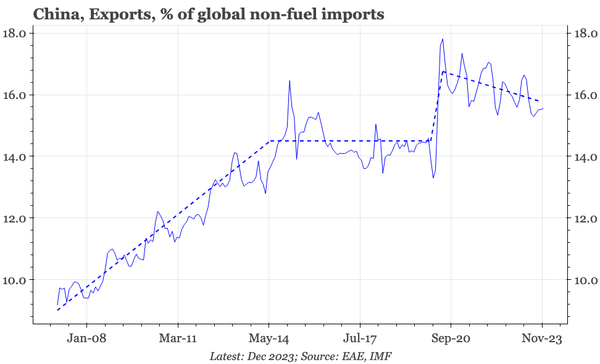

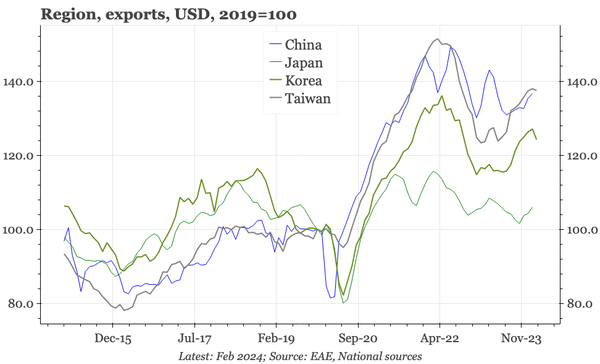

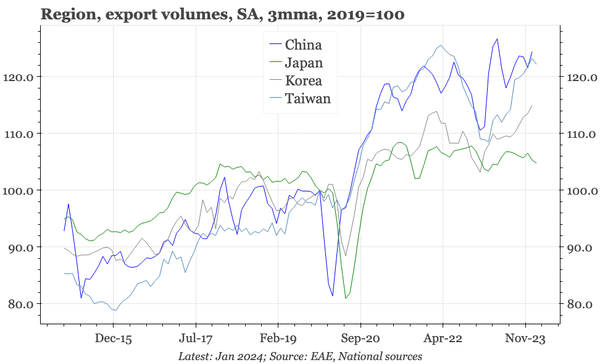

Cyclically, China's exports are improving, but the lift doesn't look particularly strong yet. Structurally, too, recent export performance has been a little underwhelming.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

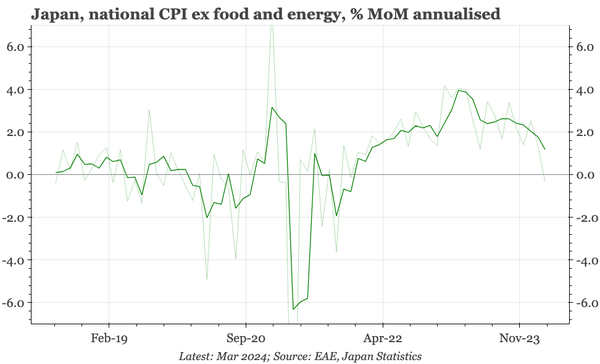

We estimate that sequential core CPI inflation turned negative in March. The macro backdrop suggests that should be temporary, but uncertainty about the real strength of the domestic inflation dynamic constrains the BOJ's ability to respond to the unhelpful weakness in the JPY.

The belated release of the PBC's consumer survey continues to show falling price expectations, and so hint at rising real rates.

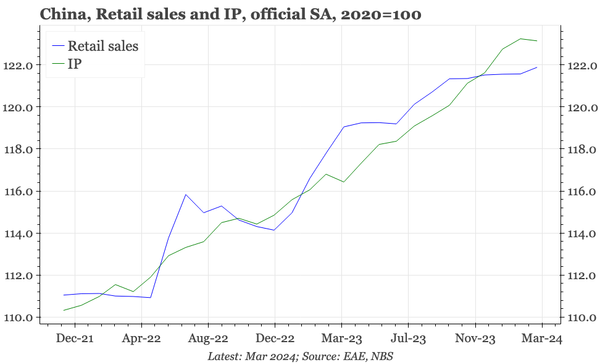

The consensus on China has improved in recent weeks, but there's nothing in the Q1 activity release to reinforce that shift.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

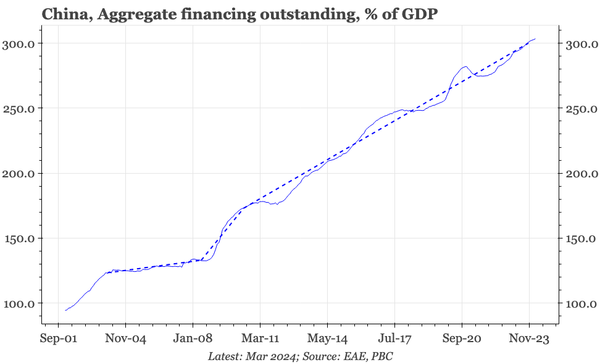

China's monthly monetary release doesn't seem nearly as important as it once did, because a lot of the major indicators are rangebound. The one indicator that looked a bit different last month was M1, but that rebound fully reversed in March back down to just 1.1% YoY.

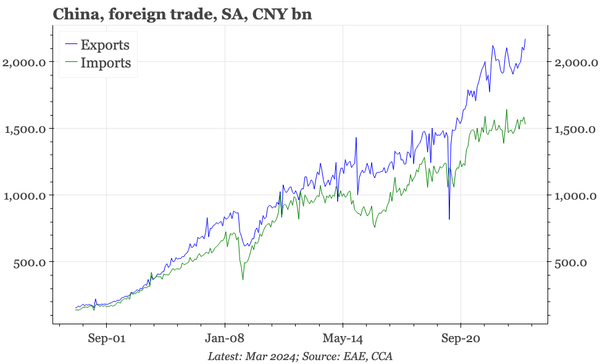

We think today's export data were strong, reaching an all-time high in CNY terms. If there was weakness, it was in imports. The result, obviously, is a renewed widening of the trade surplus.

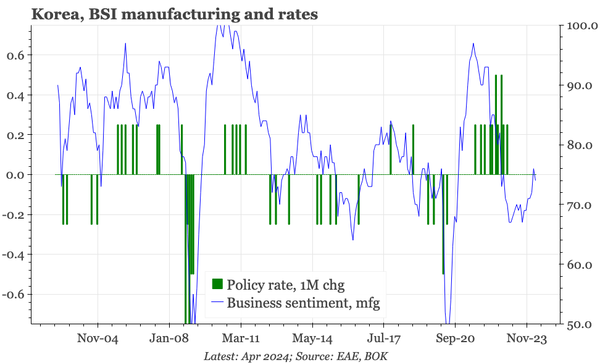

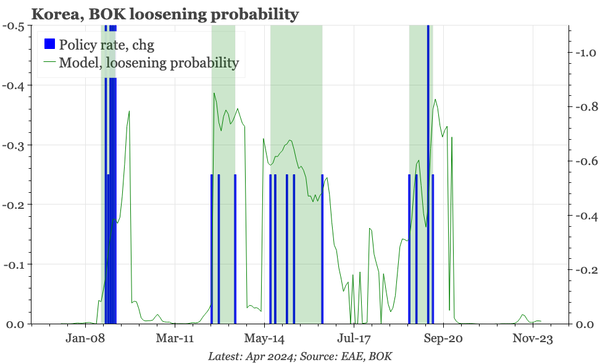

The BOK today sounded confident that core is coming down, but argued that headline is more uncertain. Of course, these two measures are different, but the distinction still feels disingenuous, and gives the impression that the bank is just trying to buy a bit more time.

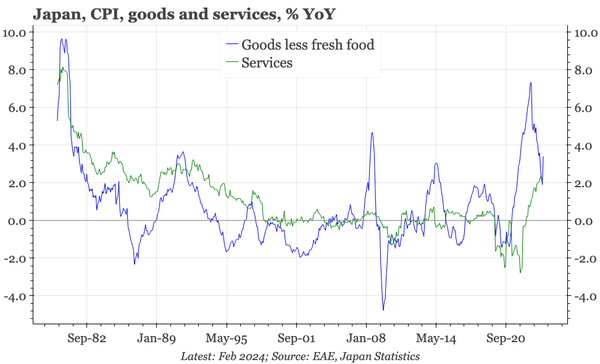

We take a detailed look at services prices, which account for 50% of the CPI basket, and need to continue to rise if inflation is to be sustained.

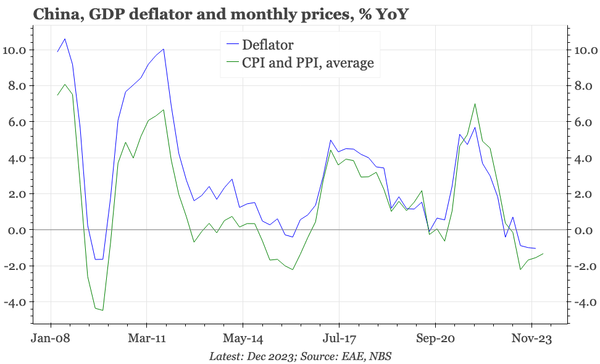

Price trends in China remain range bound, with PPI falling at a 2.5%-3% YoY rate, and CPI fluctuating around 0.7%. Narrow leading indicators for inflation suggest some strengthening from here, but a real change in inflation dynamics needs a change in China's overall macro dynamics.

With headline CPI still above target and the US-Korean yield gap widening, we don't think the BOK is ready to cut yet. However, the weakness of economic activity and the softening of core inflation raise the likelihood of a dissenting vote.

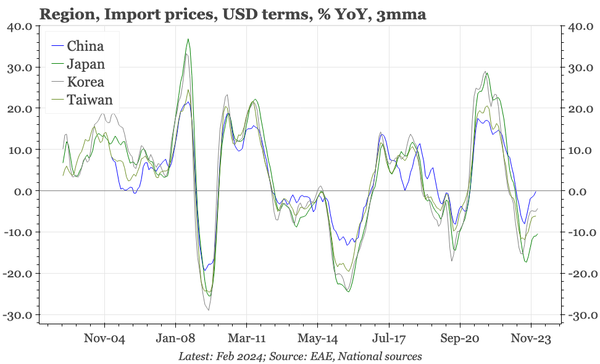

The export cycle is recovering, but more in volume than value terms, and in Taiwan and China than Korea. This won't remove worries about weak consumption in Korea and China. But it likely is sufficient to keep Taiwan's economy tight, and the CBC will likely be hiking again if exports rise more.

Consumer confidence for March gives reasons to think that stronger consumption will drive continued economic recovery in 2024.