Subscribers Only

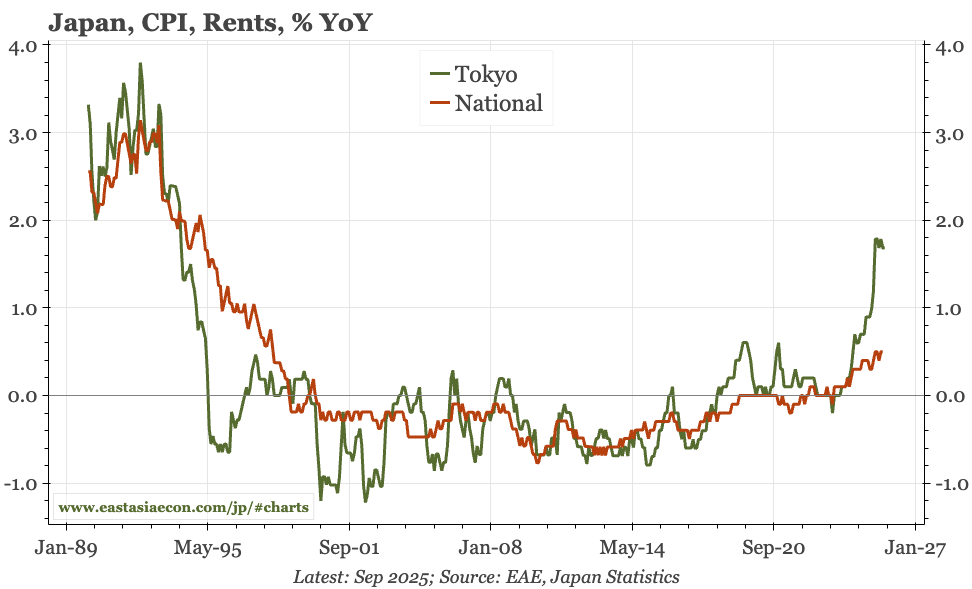

Japan – another noisy month for CPI

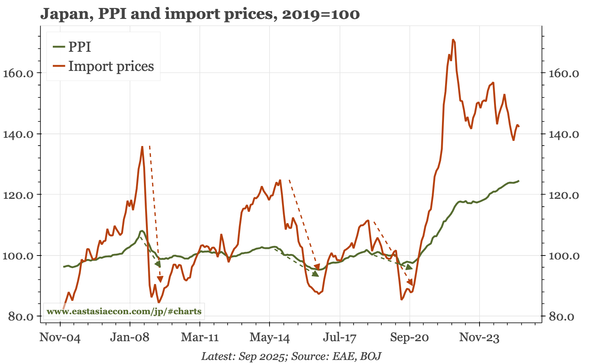

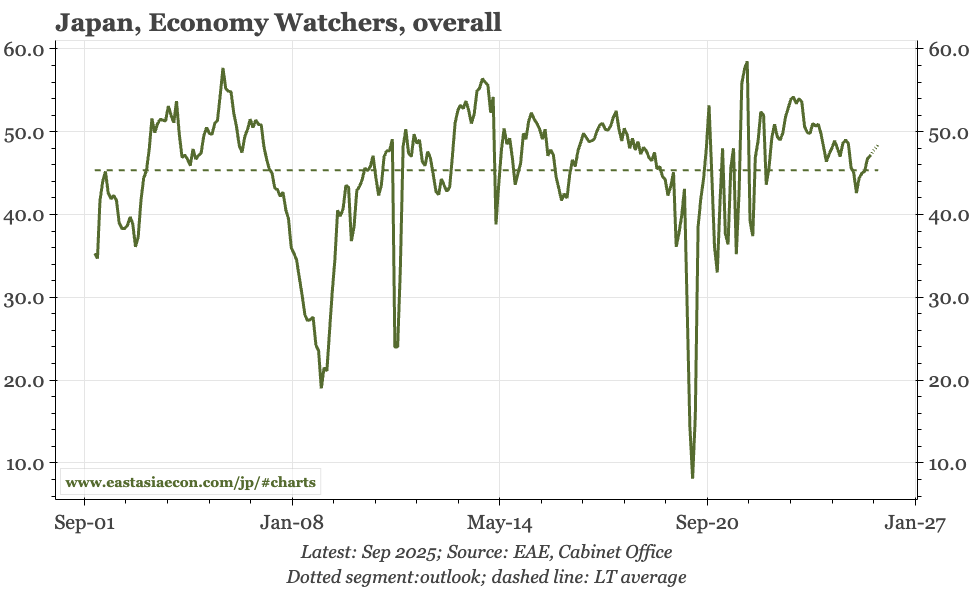

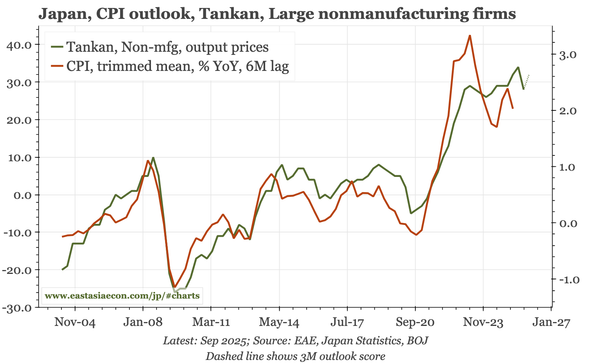

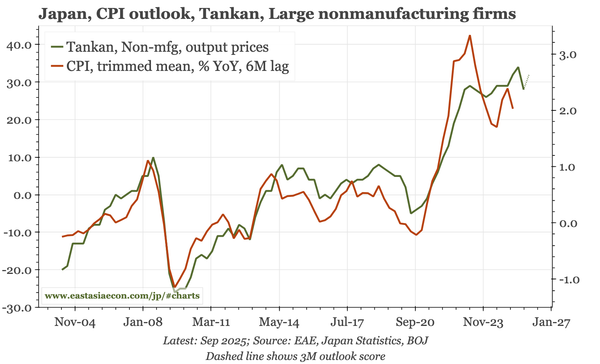

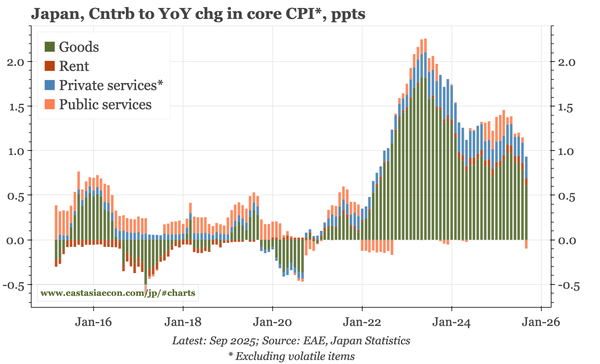

National inflation data for September was messy again. One reason was public service prices falling, a development that stands out when a theme of recent BOJ speeches has been pent-up inflation pressure in the public sector. Overall, the inflation picture still looks solid.