Subscribers Only

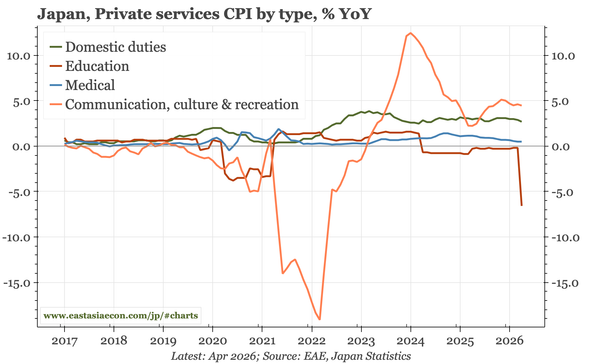

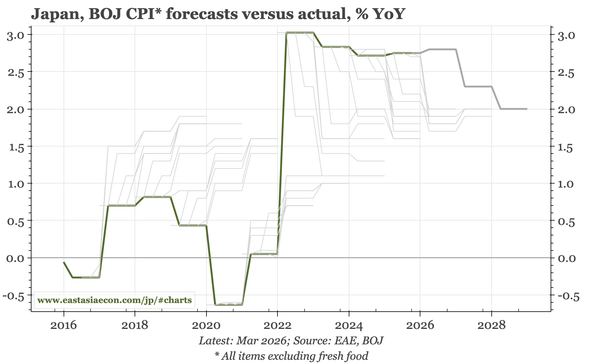

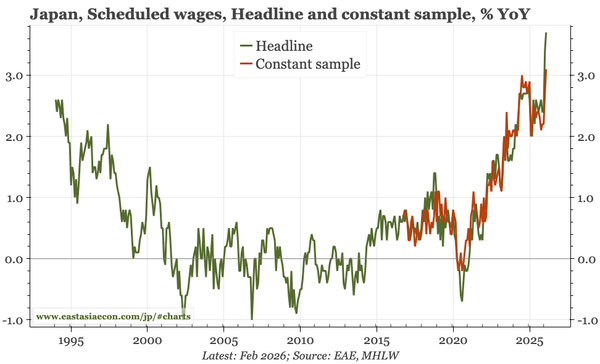

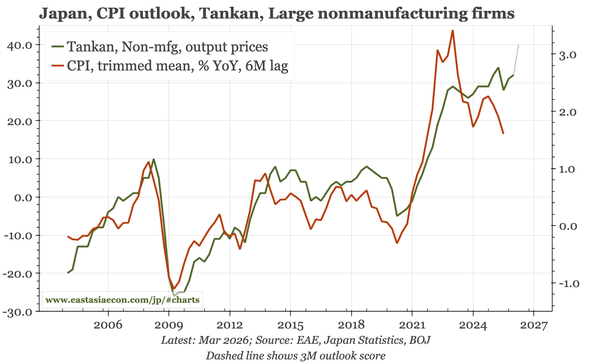

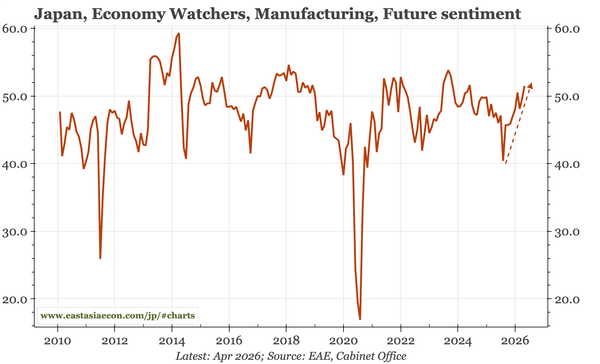

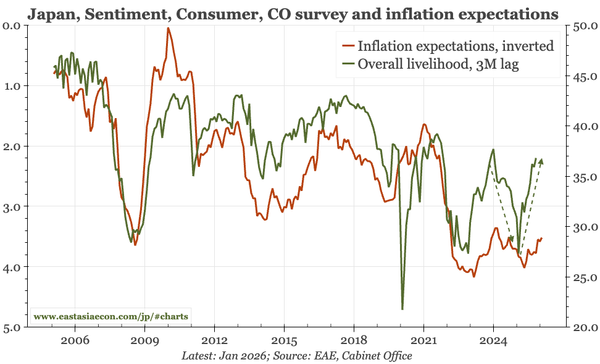

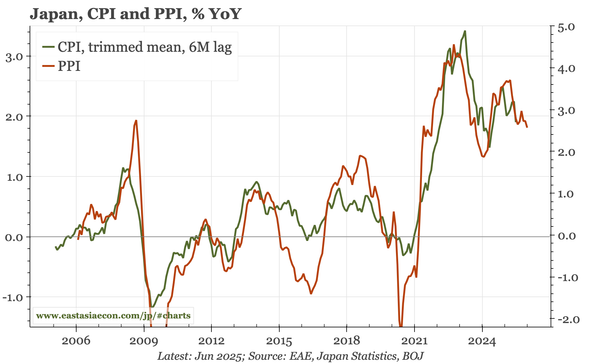

Japan – sentiment strong, prices stronger

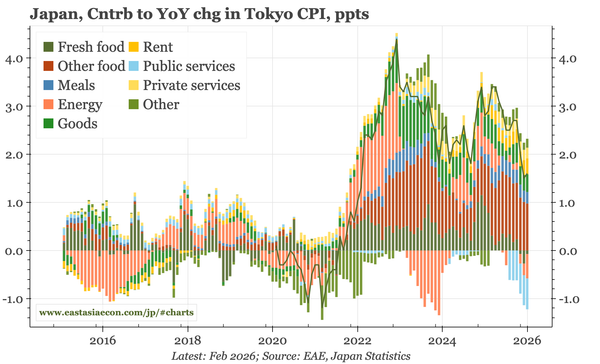

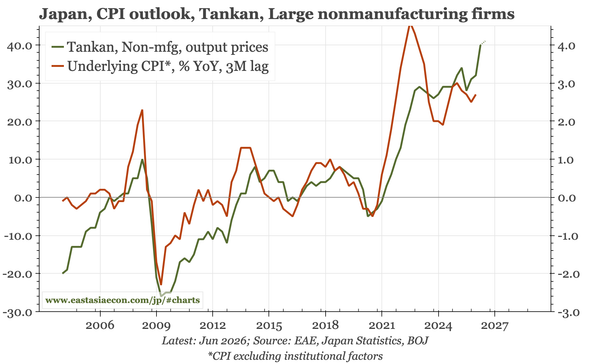

The detailed version of the Tankan won't be released until tomorrow. But the headlines today show a clear story: business sentiment remains strong, and inflation pressures have risen yet again. The BOJ needs to become more hawkish.