East Asia Econ

Home

About

QTC

Region

CN

JP

KR

TW

Calendar

中文

Linkedin

Youtube

Twitter

Data

Sign in

Subscribe

East Asia Econ

Macro and market analysis of the world's largest economic region

Japan – tariffs a bigger concern than prices and consumption

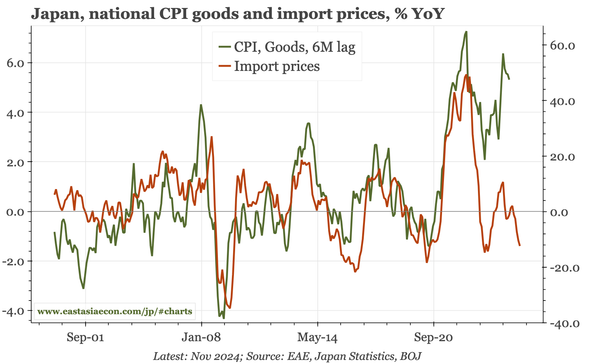

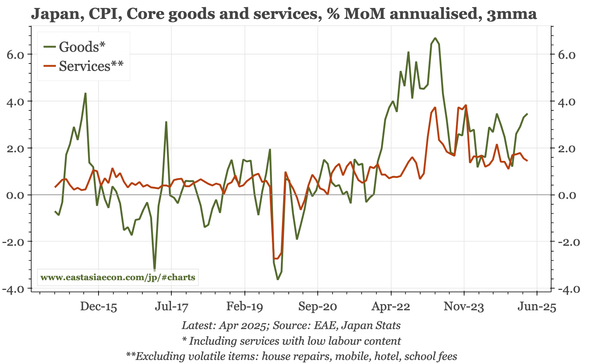

Japan – goods prices starting to reverse

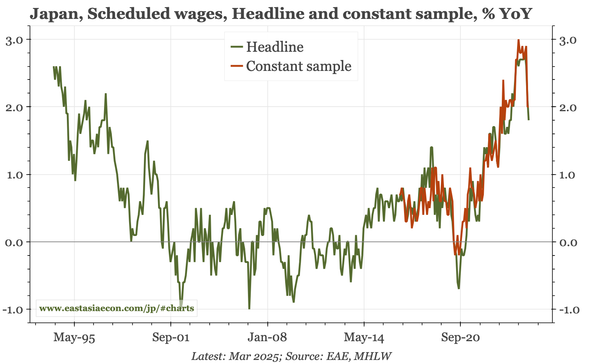

Japan – still the real wage squeeze

Japan – BOJ officials still leaning positive

Japan – issues sharpen for the BOJ

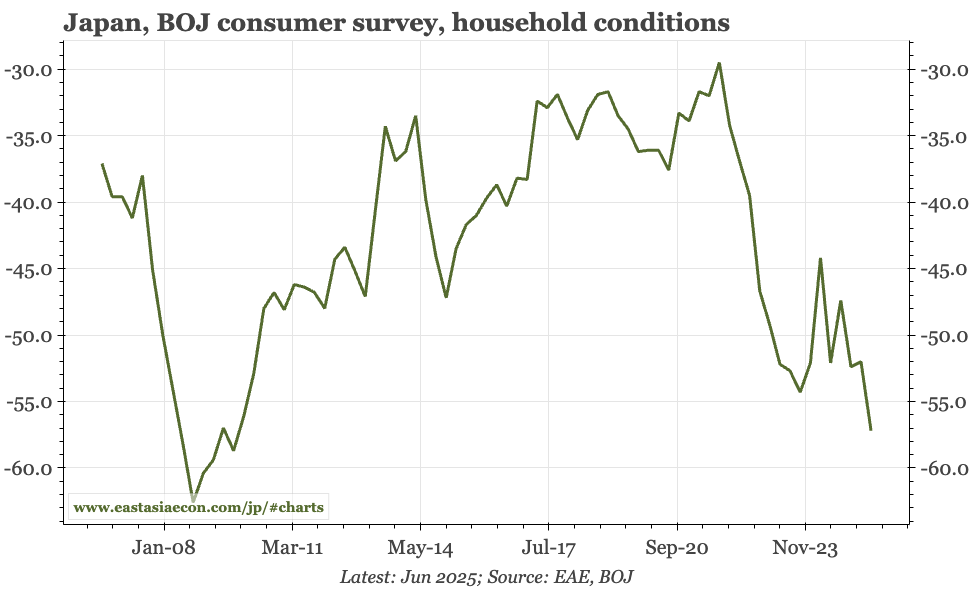

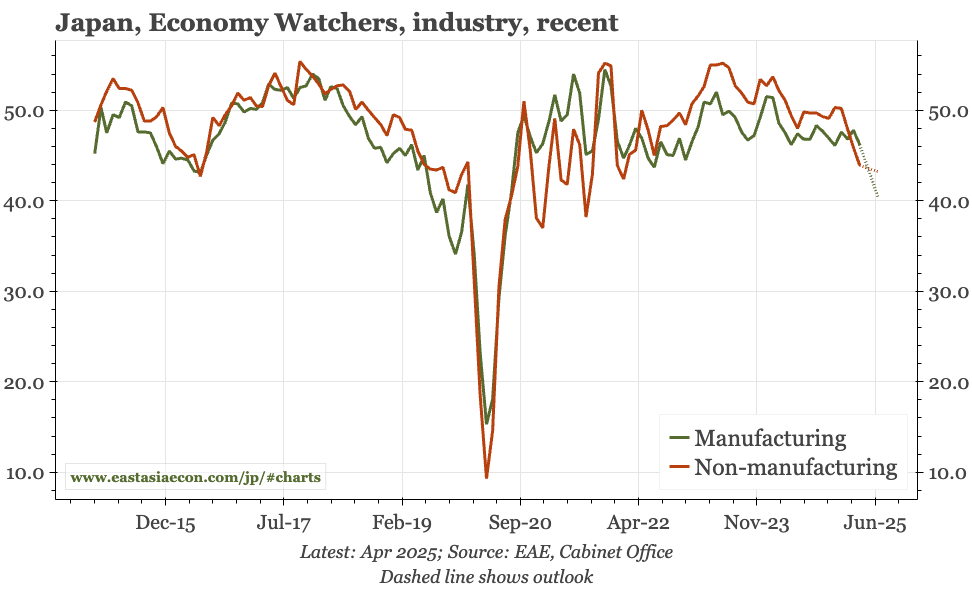

Japan – helpful rebound in consumer confidence

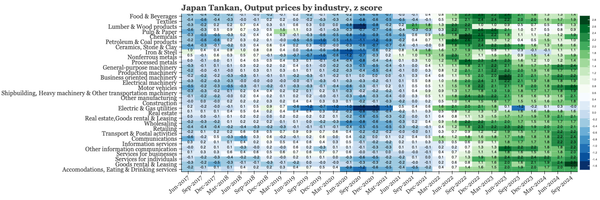

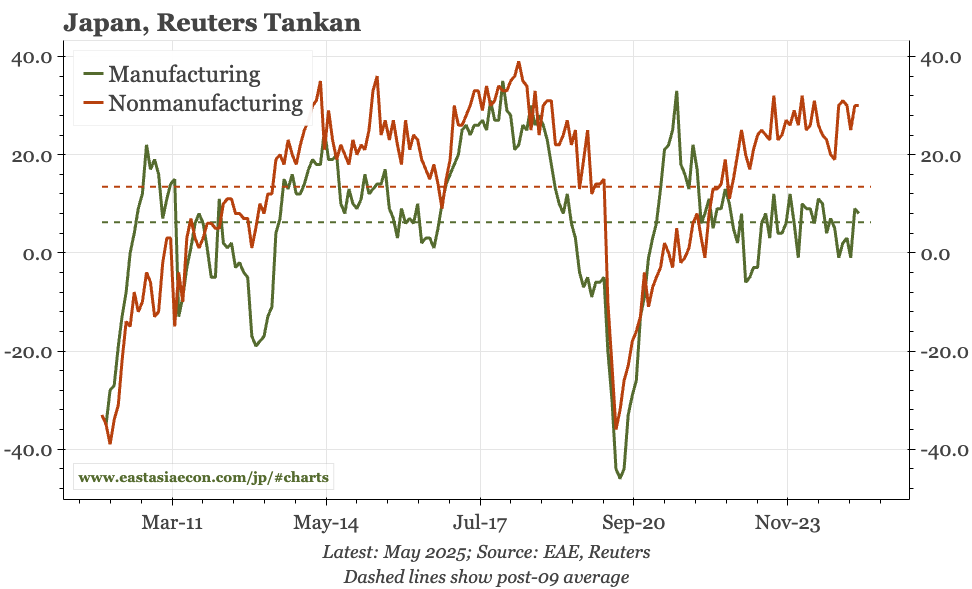

Japan – another solid Tankan

Japan – cycle review and BOJ scenarios

Japan – Tamura's case for further hikes

Japan – more subdued

Japan – wages jump in April

Japan – Ueda upbeat

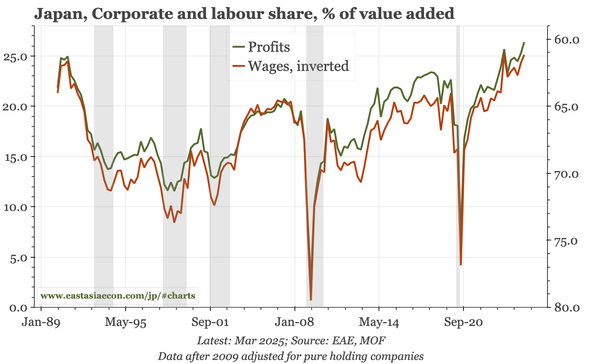

Japan – profits up, labour share down

Japan – high CPI, tight labour market, weak spending

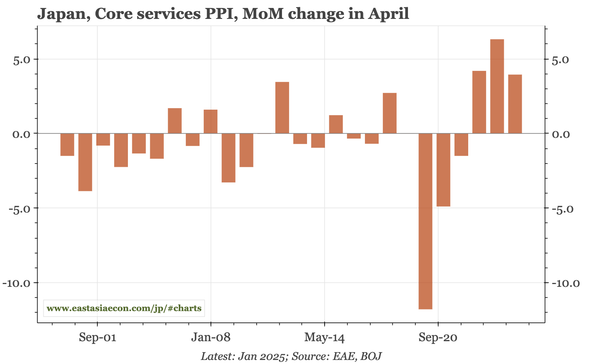

Japan – SPPI shows solid underlying inflation

Japan – headline inflation up, core stable for now

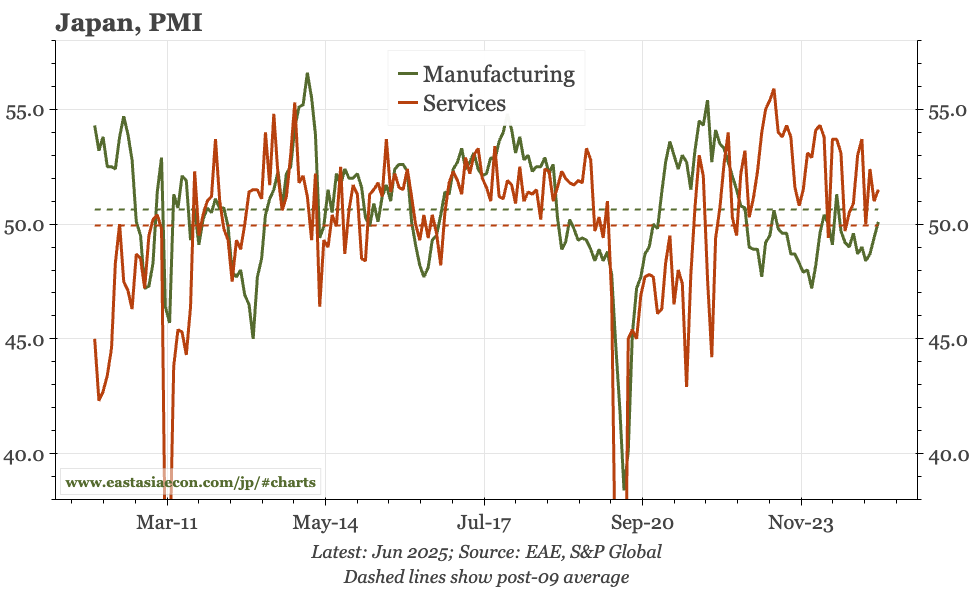

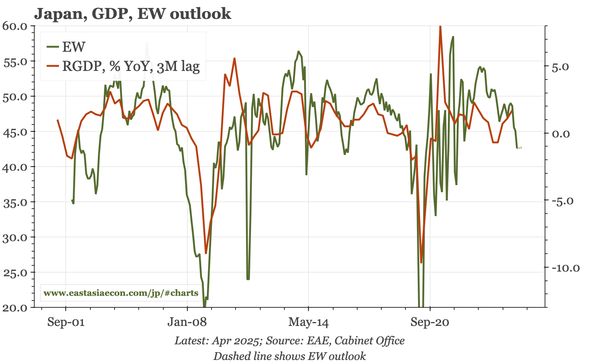

Japan – not bad, but still uncertain

Japan – details better, but headline GDP already declining

Japan – sentiment takes another step down

Japan – wage growth down, waiting for April

Japan – uncertain outlook, but not giving up on wages

Japan – tariffs matter, but so does inflation

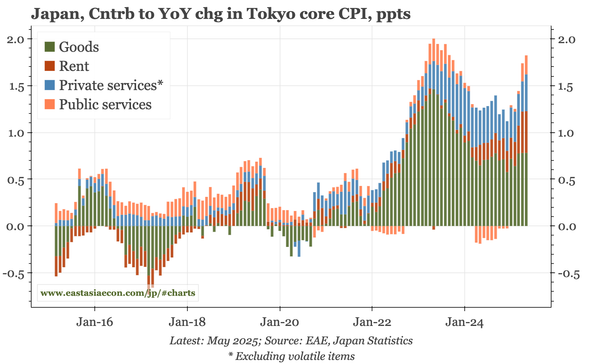

Japan – broad-based inflation

Japan – four reason why the JPY hasn't helped exports

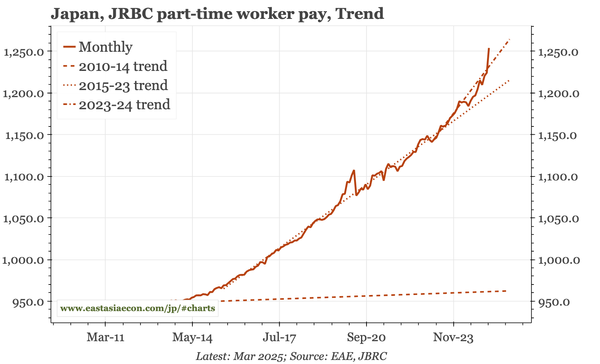

Japan – CPI mixed, but part-time wages up

Page 1 of 11

Older Posts

→