East Asia Econ

Home

About

QTC

Region

CN

JP

KR

TW

Calendar

中文

Linkedin

Youtube

Twitter

Data

Sign in

Subscribe

Korea

Article archive

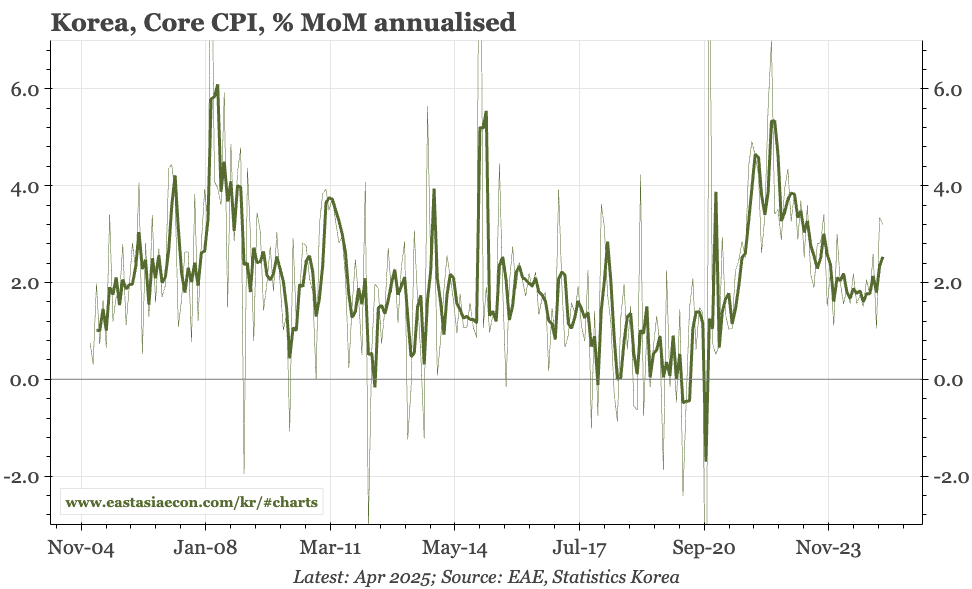

Korea – headline CPI ticks up, but should now fade

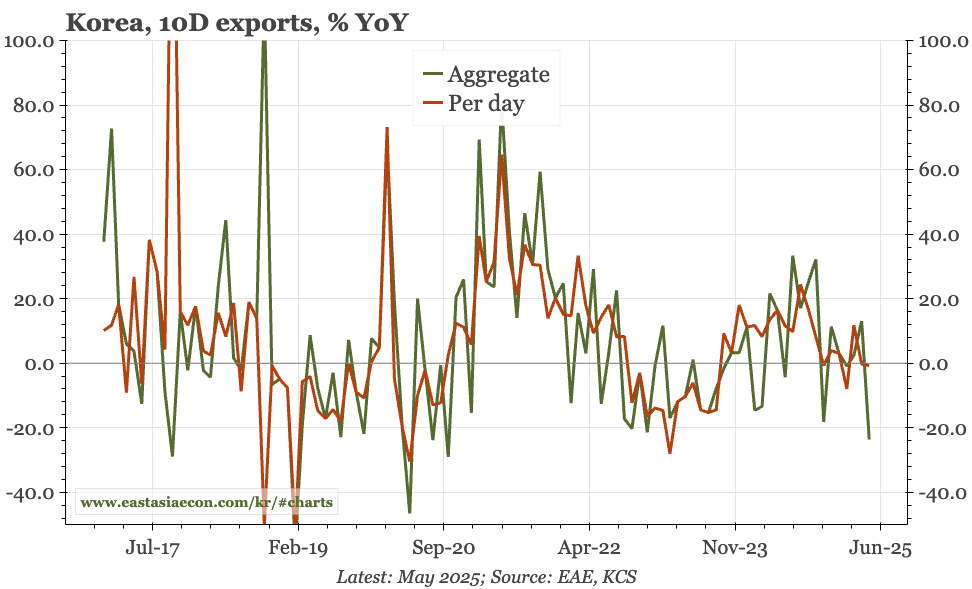

Korea – finally, export perk up

Korea – a change, even if it's not fundamental

Korea – employment and exports still sluggish

Korea – core CPI lower in May

Korea – rates down again

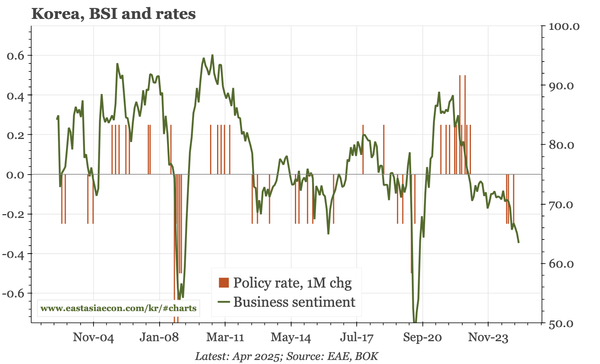

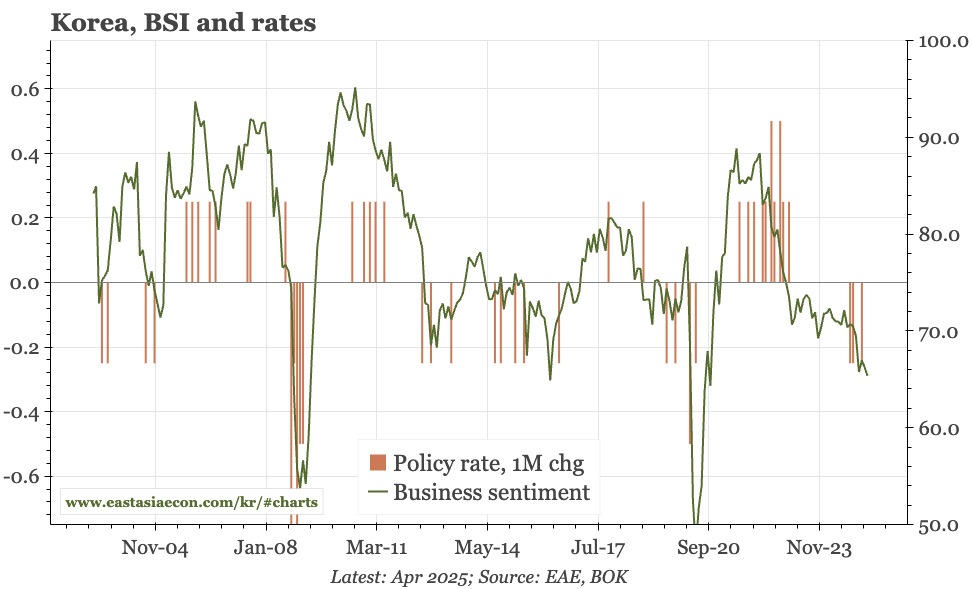

Korea – business sentiment still weak, BOK still cutting

Region – at last, Korea bucks the trend

Korea – becoming....East Asian

Korea – structural labour market looseness

Korea – minutes show cuts ahead

Korea – activity weaker than inflation

Korea – business sentiment worsens again

Korea – BOK says "come back in May"

Korea – cycle worsening, rates to fall