Subscribers Only

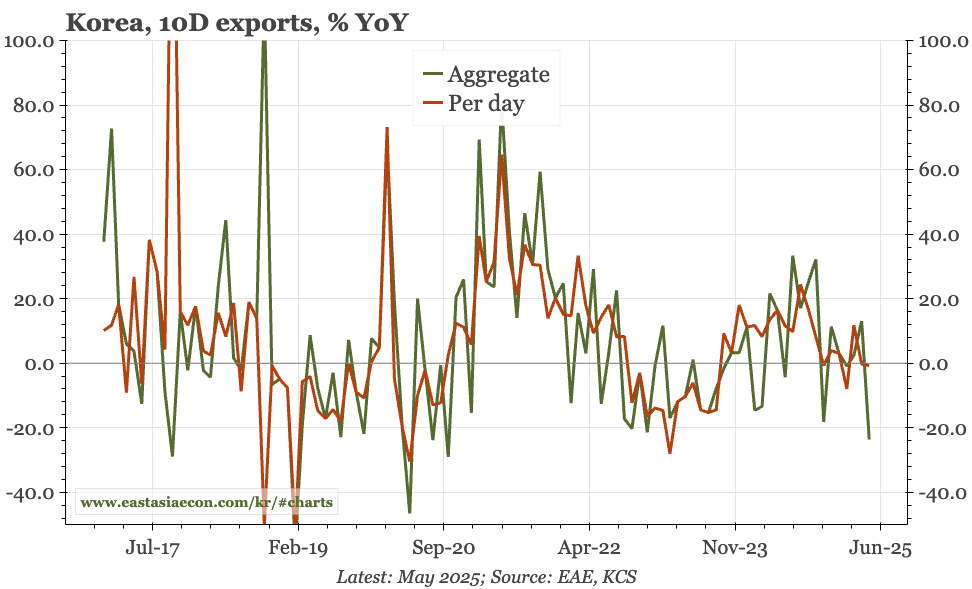

Korea – exports better, but sentiment weak

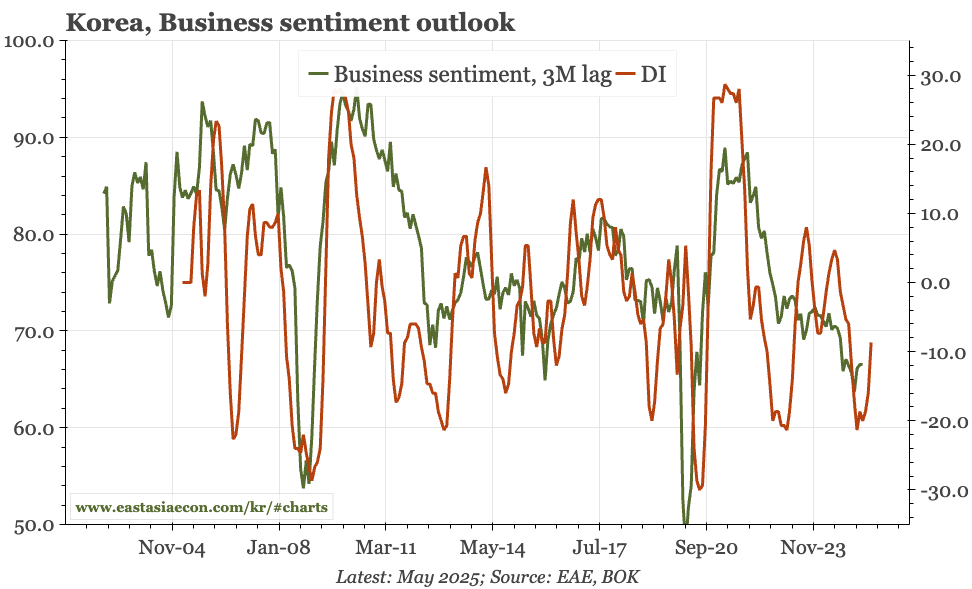

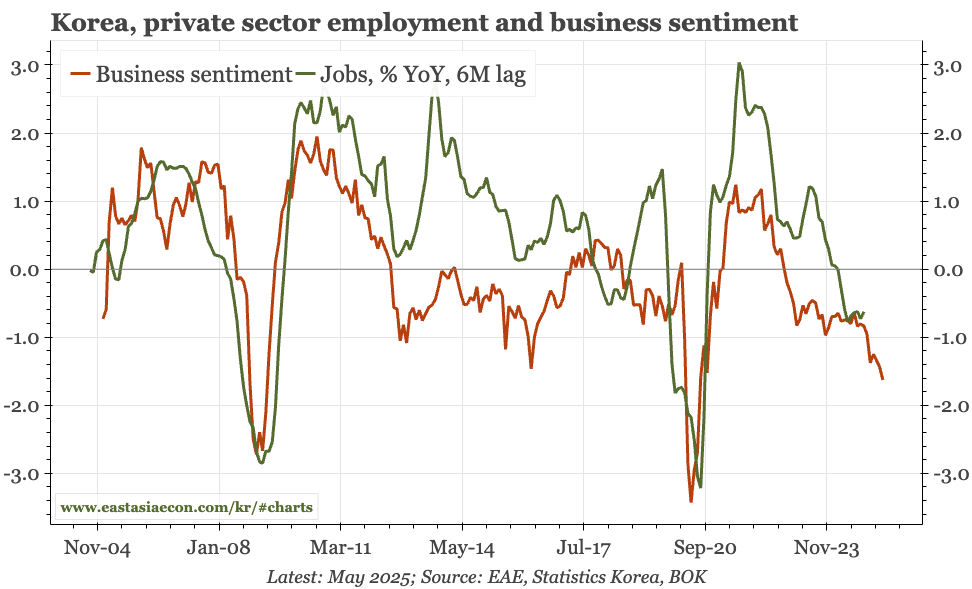

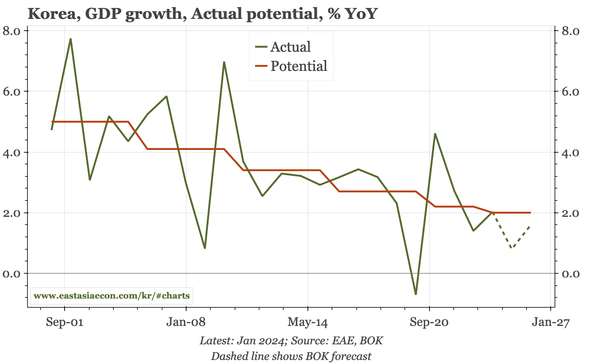

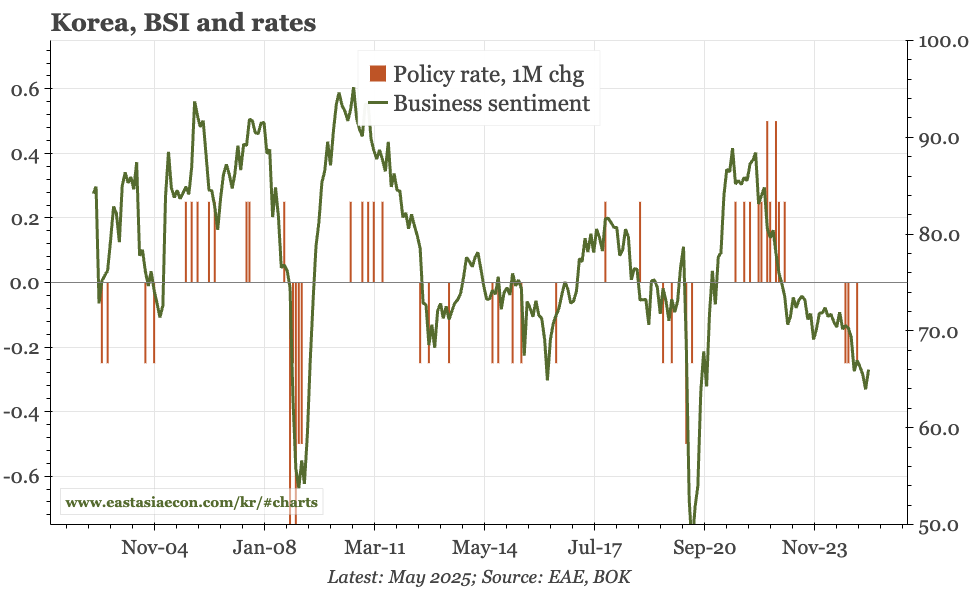

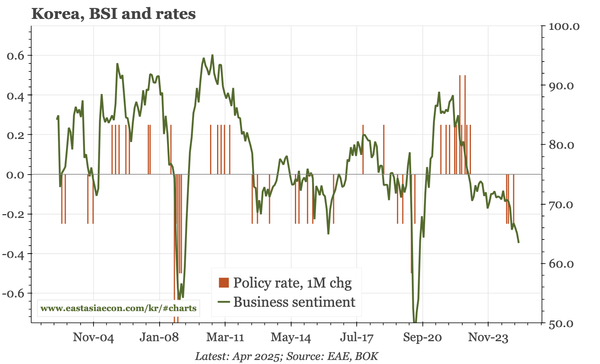

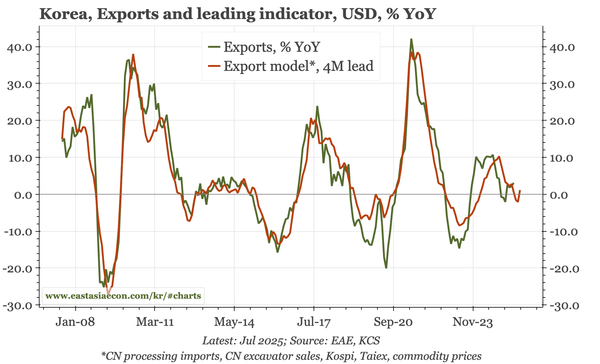

The lift in exports in June was sustained in July. But I'd be sceptical that marks the start of an upcycle. The strength is all about semis, and today's PMI, like last week's BOK business sentiment survey, was sluggish. If there are upside risks for Korea, they are likely domestic, not external.