Subscribers Only

Region – commodity boom or BS....slide pack

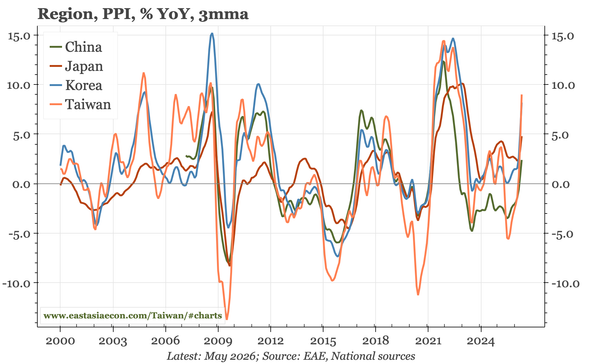

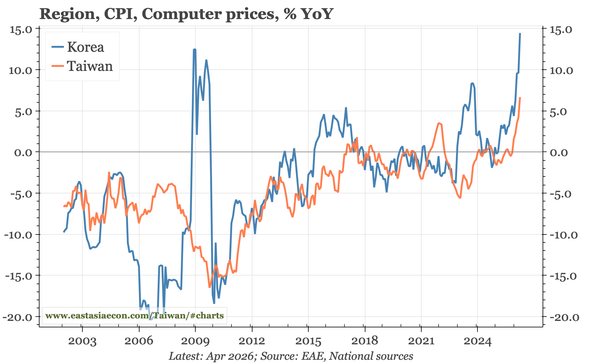

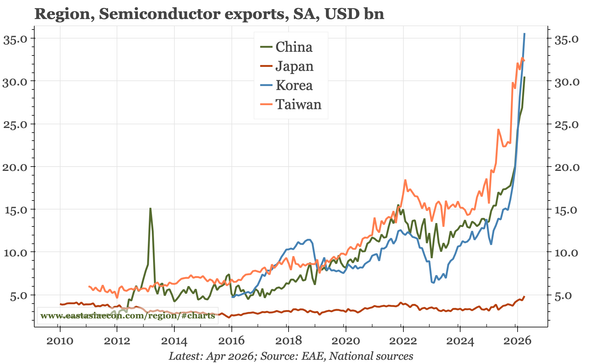

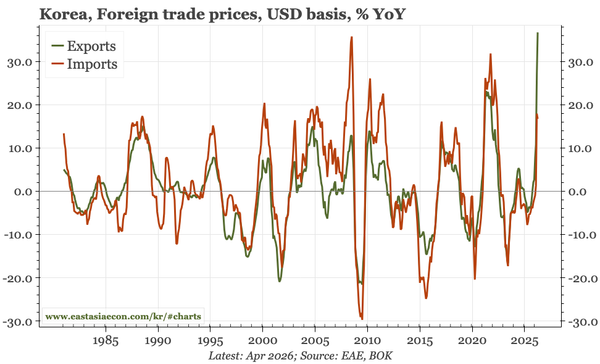

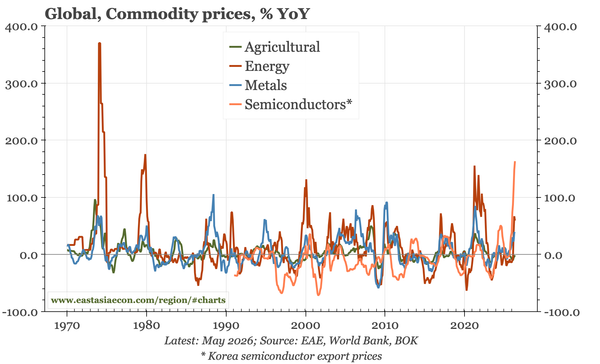

Earlier this week, I published a longer note delving into the macro and market implications of the semiconductor boom. You prefer pictures to text, so this is the accompanying chart pack.