Subscribers Only

Last week, next week

It isn't yet all about the war, given the real strength in semi demand. That backdrop is one reason to think underlying inflation will be lifted by the latest crisis. The durability of the AI cycle will also be the canary in the mine for a negative supply shock becoming a negative demand shock.

Subscribers Only

Last week, next week

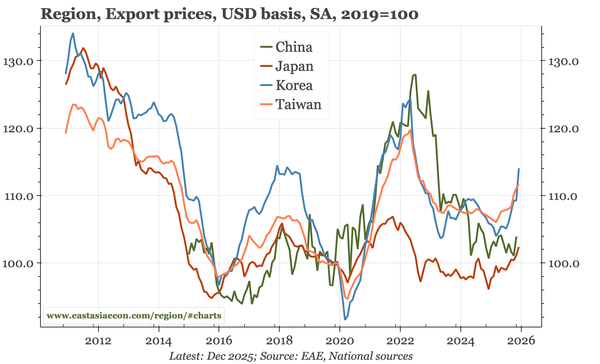

I spent time last week delving into export prices and terms of trade, dynamics that should be offering support for currencies. The data flow was all about Japan, and painted the picture of an economy in good shape. That could yet be undermined by policy choices, either at home, or in the US.

Subscribers Only

Last week, next week

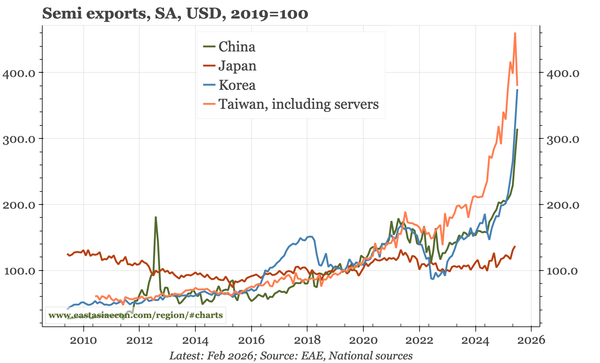

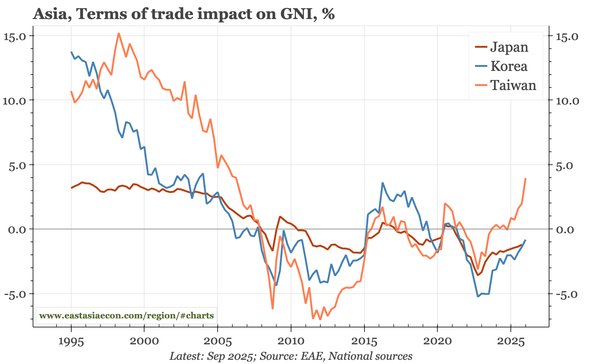

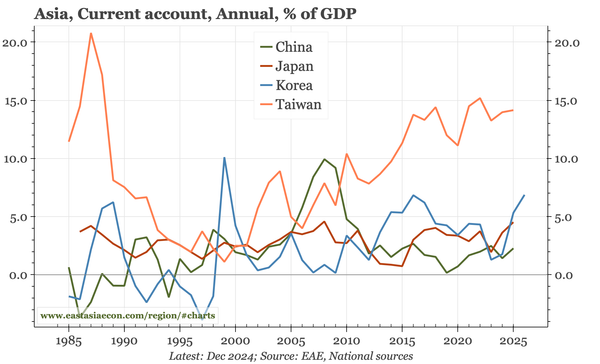

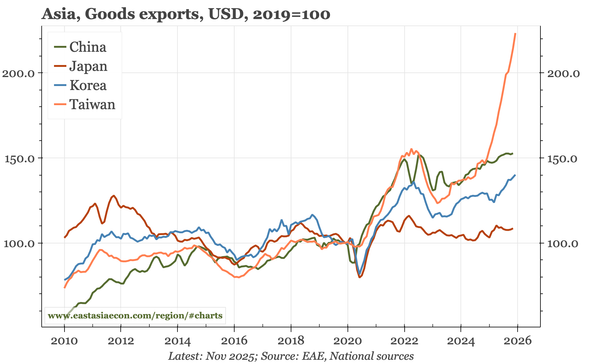

Three themes from last week: improving terms of trade, led by rising export prices; expanding current account surpluses; and growing optimism about the sustainability of AI-related hardware demand that is critical for cycles in Taiwan and Korea. Also, happy year of the (fire) horse.

Subscribers Only

Last week, next week

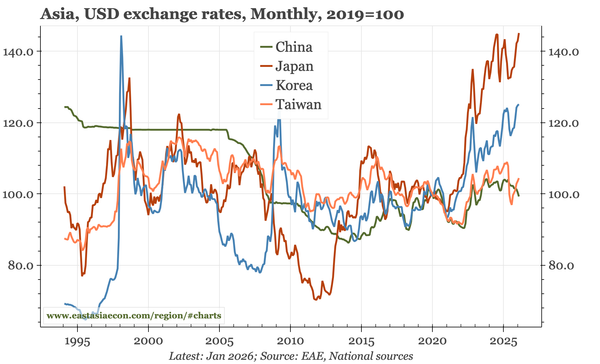

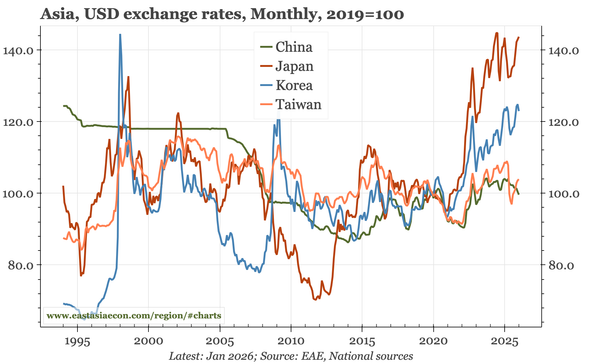

The fundamental themes for the region are rising external surpluses, improving manufacturing cycles, and lessening deflation in China. That mix should be helping currencies. The offsetting factors to be monitoring are politics in Japan, flows, and global dynamics around tech and the USD.

Subscribers Only

Last week, next week

Regional themes: continuing (and under-appreciated) nominal improvement in China; election uncertainty in Japan; strengthening export momentum in Korea on the back of chips; which in turn looks significant given the huge outperformance of Taiwan through 2025, all because of AI and semiconductors.

Subscribers Only

Last week, next week

Is a ceiling forming for $Asia? Three developments are helpful: CNY fixing strengthening through 7; more US interest in Asia under-valuation; visible concern in Tokyo about weakness in both the JPY and JGBs.

Subscribers Only

Region – cycles, structures and currencies

Using an update of my regional chartpack to think about exchange rates. Specifically, I think the cycle and structure dynamics are moving risk-reward in favour of Asian currencies. I'd argue that is true if the global picture is unchanged, but it could also be true if conditions in the US falter.

Subscribers Only

Last week, next week

Themes: capital flows v CNY appreciation in China; fiscal fear v real policy rate in Japan; foreign v domestic equity strength in Korea; policy status quo v export surge in Taiwan.

Subscribers Only

Last week, next week

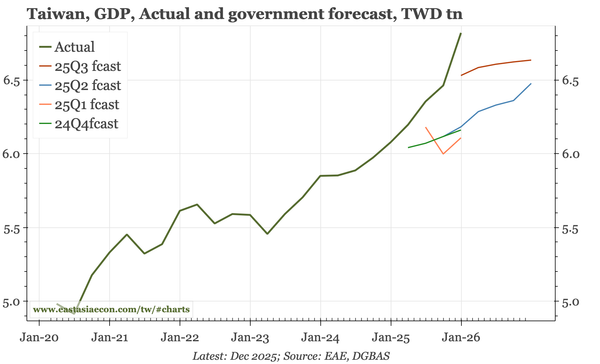

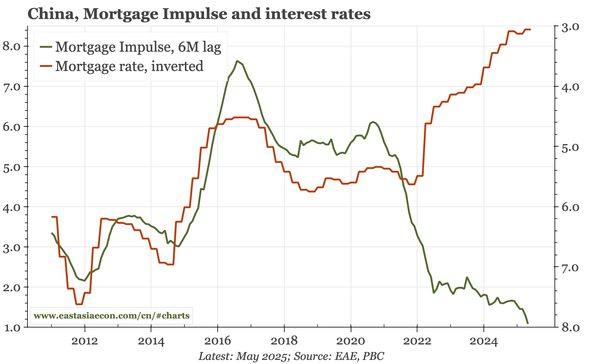

China: the nominal stabilisation is fragile. Japan: with the cycle looking good, the risk of a BOJ upside surprise is the highest since July 2024. Korea: the upside scenario from the semi cycle still isn't the base case. Taiwan: macro becomes more interesting if the chip cycle sustains into 2026.