Subscribers Only

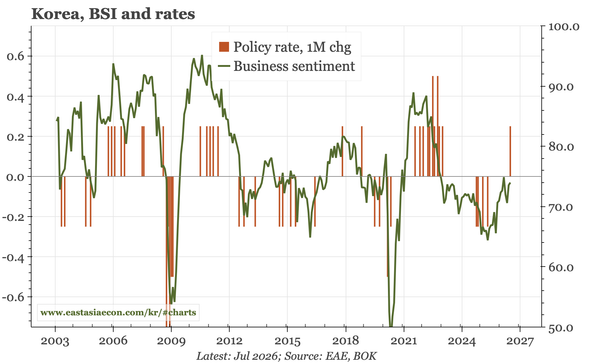

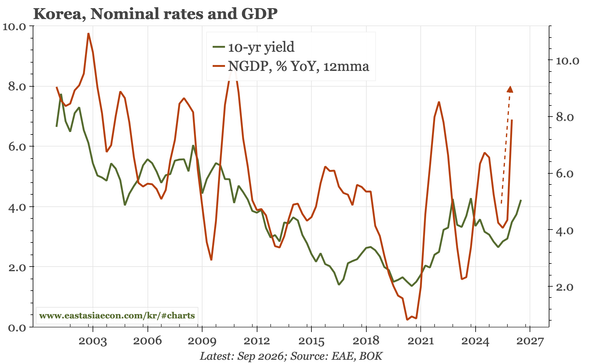

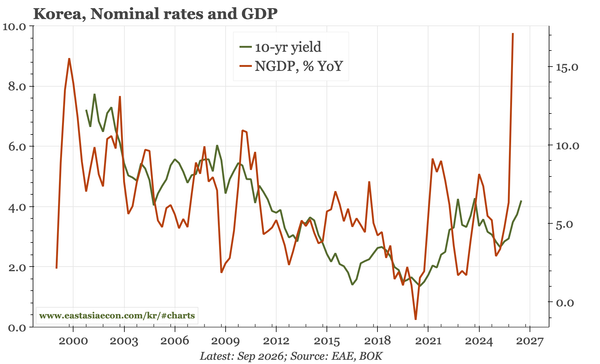

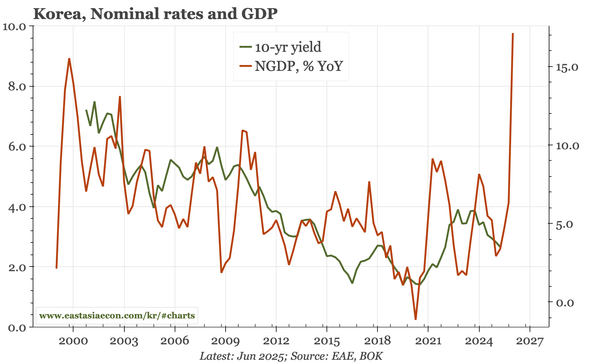

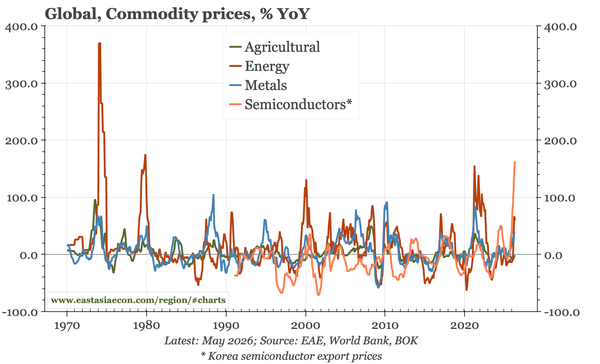

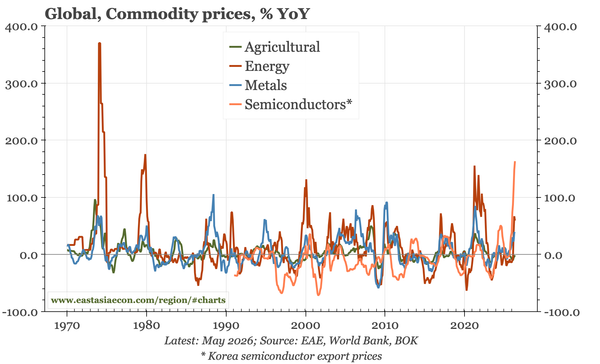

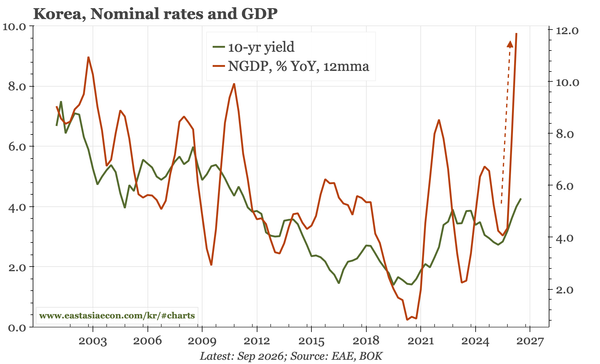

Korea – nominal growth nears 20%

Korea's real GDP growth in Q1 was solid, but nominal continues to be spectacular, rising almost 20% YoY for the first time in 30 years. Stronger nominal growth is typical of a commodity boom, and suggests more upside for rates than implied by inflation and real GDP alone.