Subscribers Only

East Asia Today

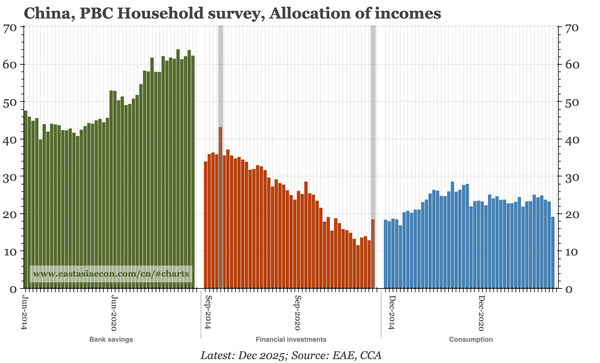

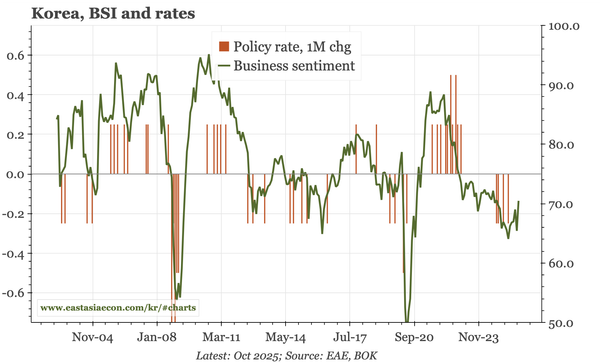

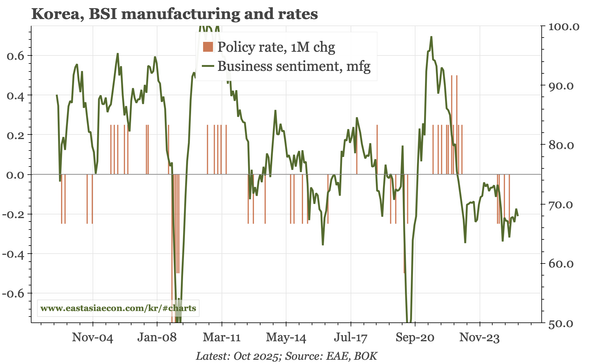

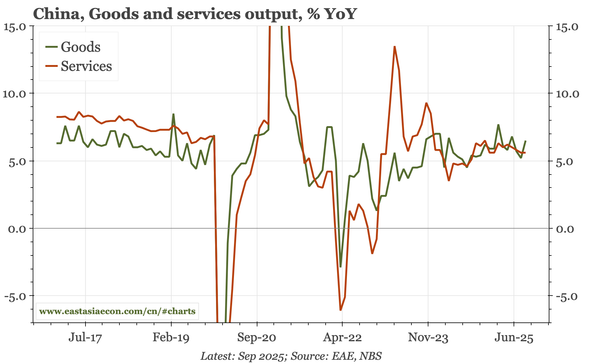

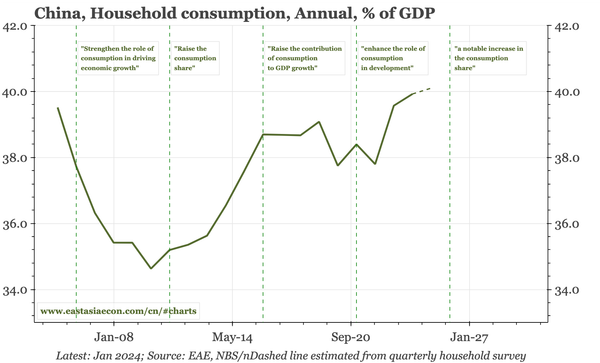

Lots of sentiment surveys to discuss today: business confidence in Korea (better), consumer confidence in Japan (also better, even though inflation expectations remain high) and Q3 economy-wide surveys for China. Also, some details of China's 15th FYP, with some encouraging language on consumption.