Subscribers Only

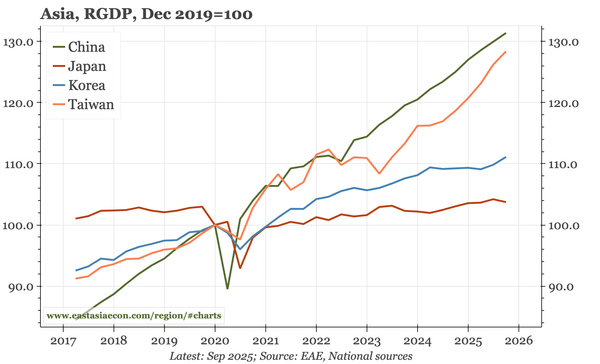

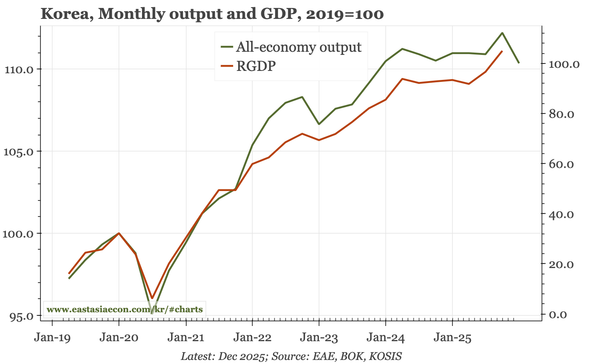

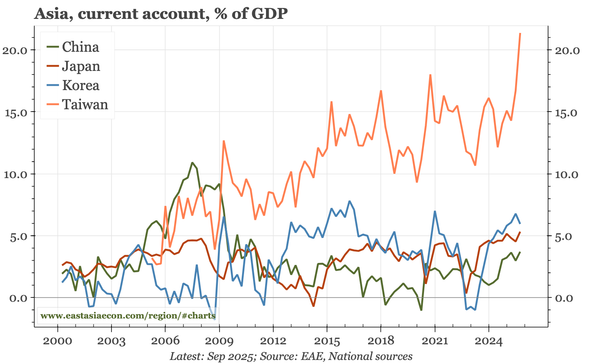

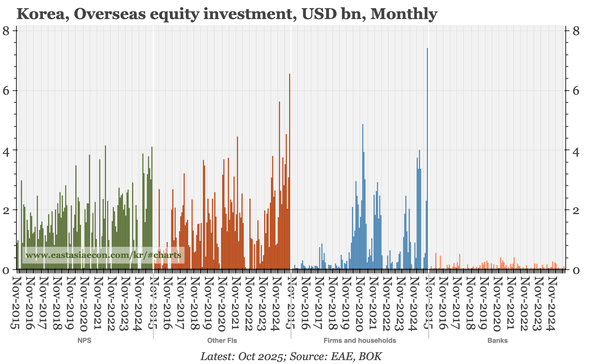

Korea – more huge overseas equity buying

The big shift in Korea's BOP since 2020 has been the rise in overseas buying of equities. That outflow surged anew in October to a record high, and by offsetting the large current account surplus, has helped keep $KRW near record highs.