Subscribers Only

East Asia Today

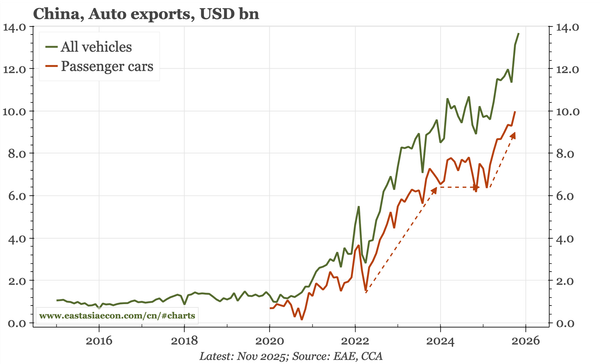

Detailed trade data show hybrids becoming the big driver of China's auto export surge. The political tensions with China have yet to derail Japan's tourism industry. In no surprise to anyone, Taiwan's central bank kept policy on hold in its Q4 monetary policy meeting.