Public Post

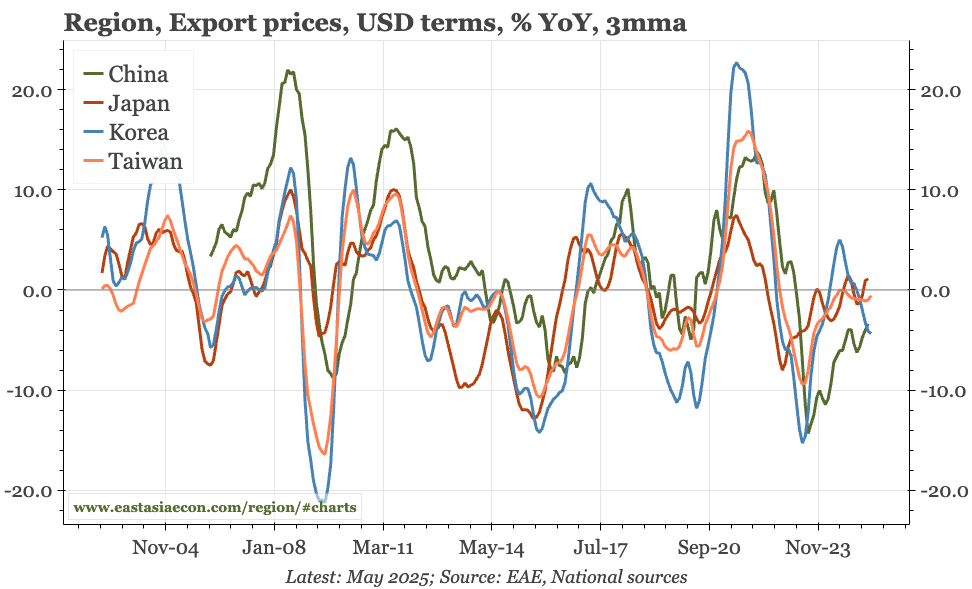

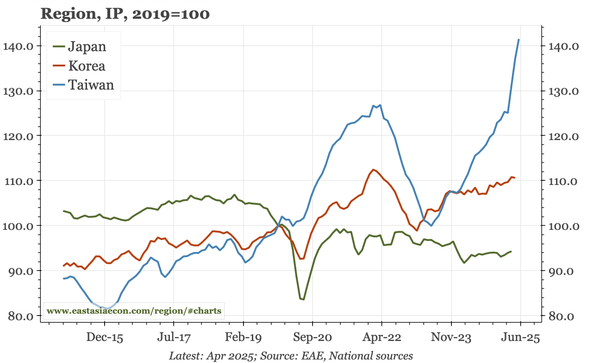

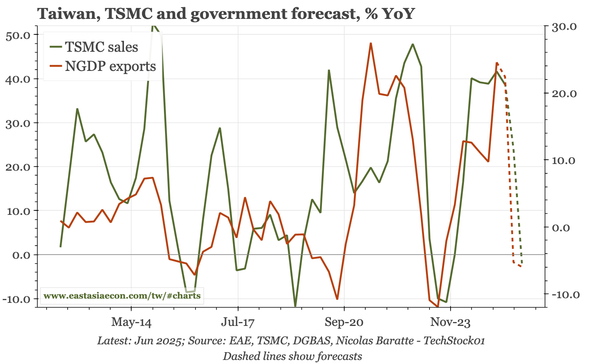

Taiwan – further softening of LIs

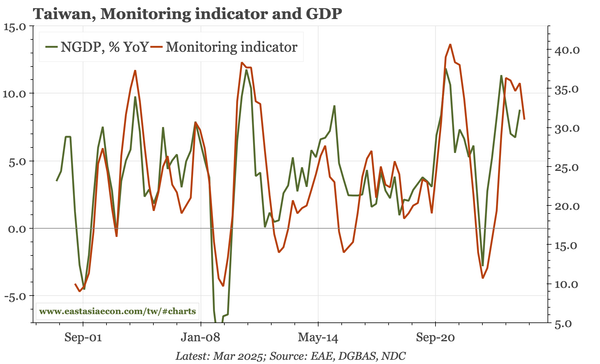

The clear conclusion from the official leading indicators is that the cycle has peaked. However, given that exports always had to slow from the absolute surge in 1H25, that isn't news. The difficulty in 2H25 will be differentiating normalisation after that surge from a real cycle deterioration.