Subscribers Only

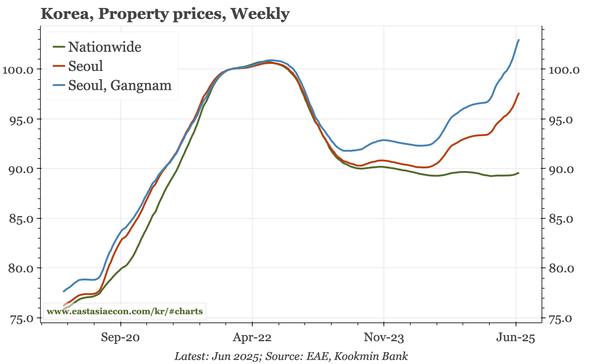

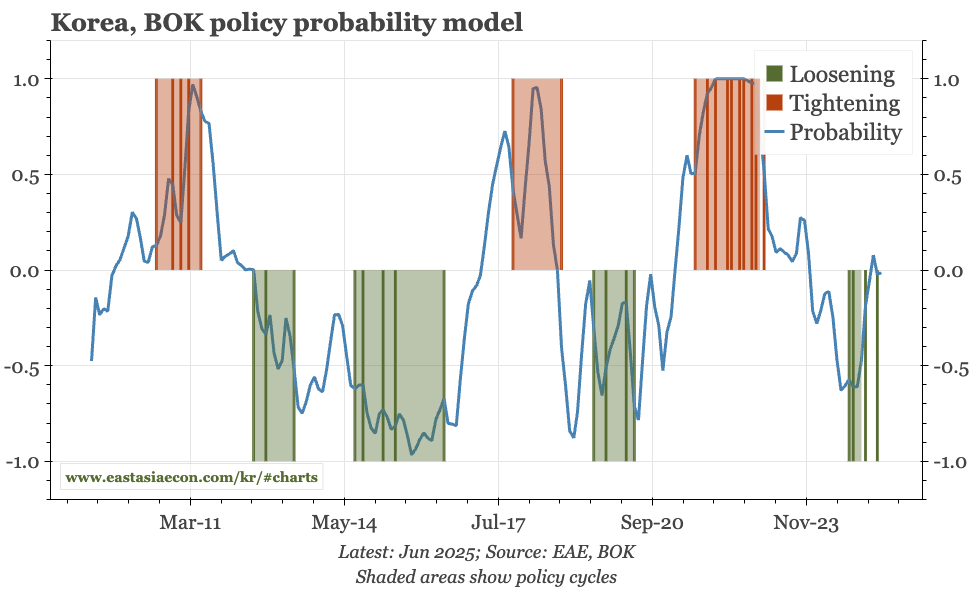

Korea – continued labour market slack

The labour market remains slack, with employment dropping in June. Wage growth is also declining, and other data released today show import prices dropping 6% in June. This all suggests inflation will remain constrained, giving room for the BOK to continue to cut rates.