Public Post

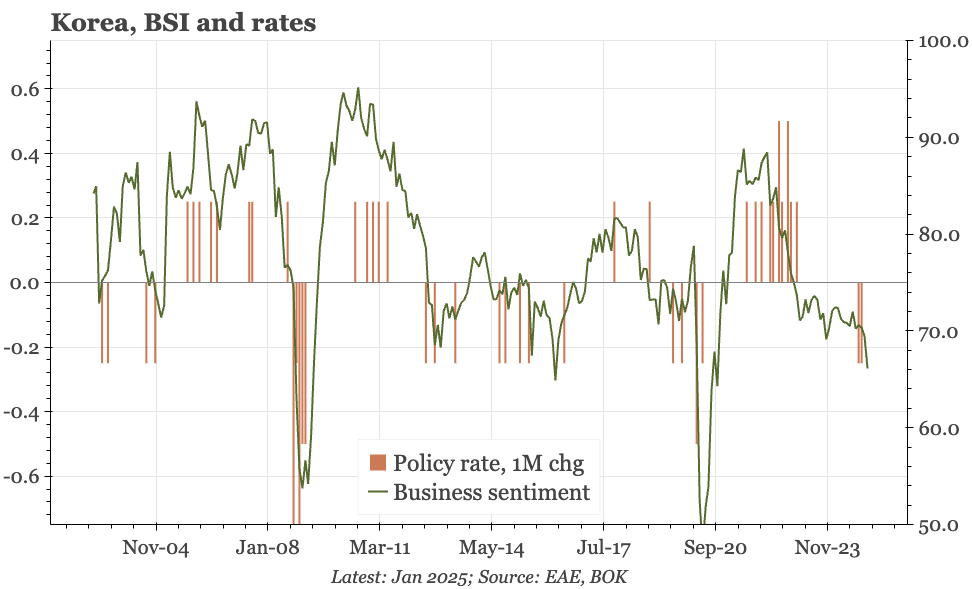

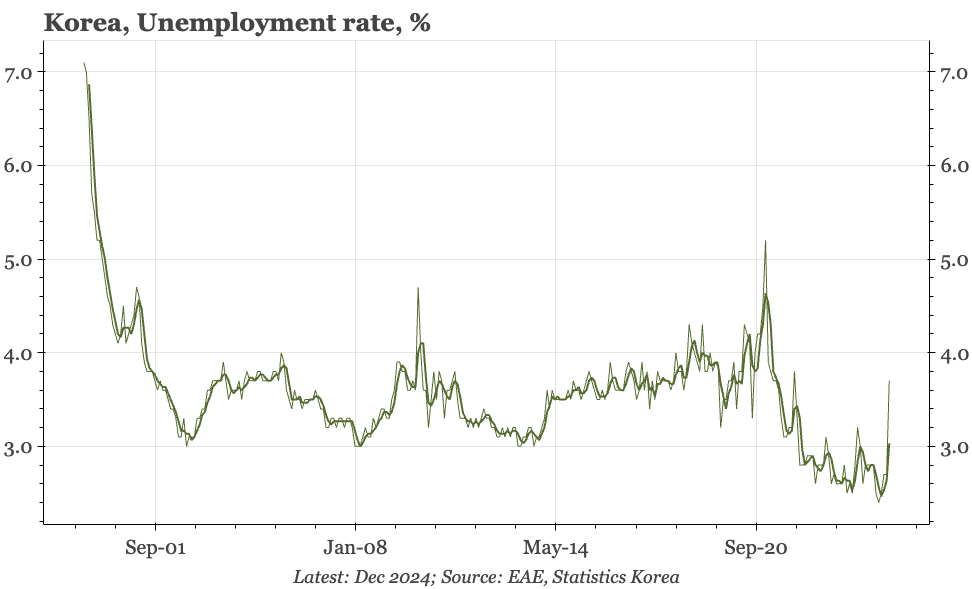

Korea – nasty employment data

December employment fell sharply, and while that can be explained by the ending of some government jobs projects, it fits with the sharper downturn in the cycle in Q424. That will likely be the focus for the BOK tomorrow, despite other data today showing KRW weakness pushing up import prices.