Subscribers Only

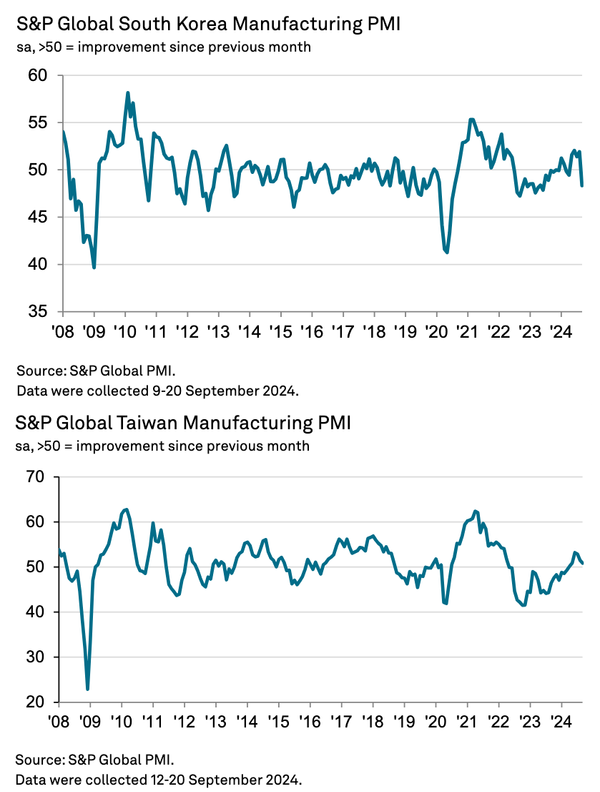

China – exports drop in September

Exports dropped quite sharply in September. China is still making share gains in autos especially, but this is another sign that the best of the recovery in the regional export cycle is probably now done. That matters for China when exports have been the strongest sector of the economy.