Subscribers Only

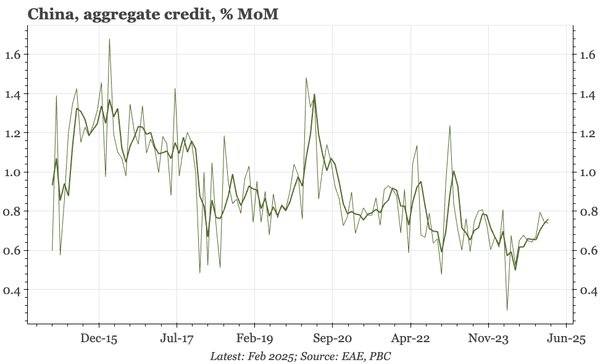

China – a turn in the credit data

The upturn in credit growth that began in June last year is continuing. That should be helping to put a floor under nominal growth. But that comes with caveats: private-sector credit lost momentum in February, and while mortgage lending isn't slowing, it doesn't show any sign of a rebound either.