Subscribers Only

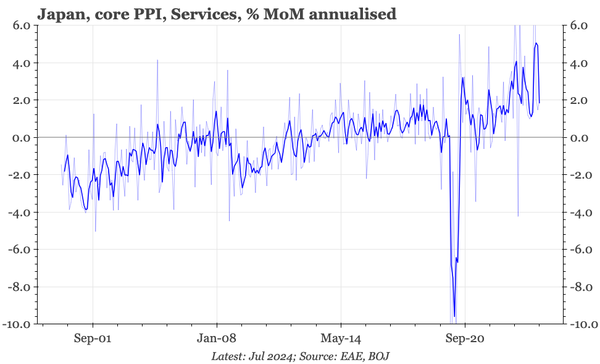

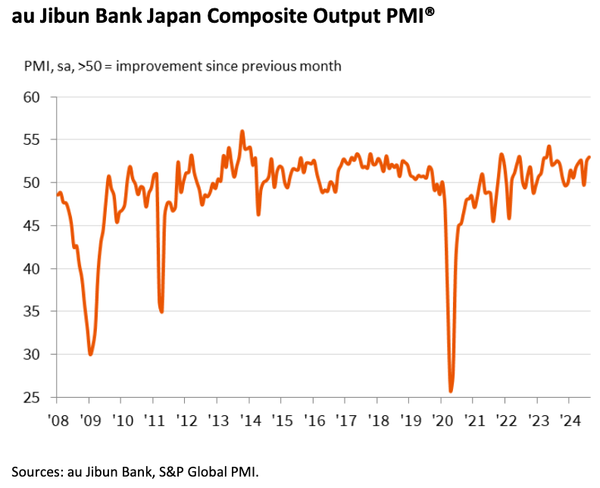

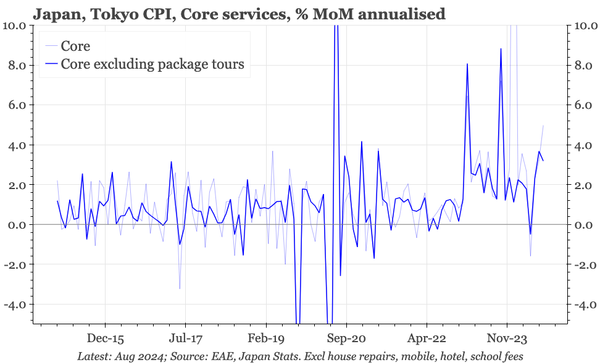

Japan – inflation on track

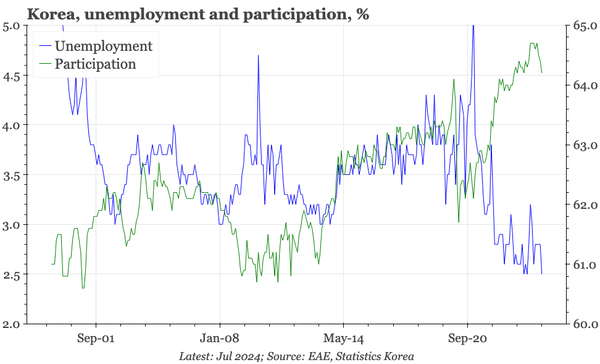

The BOJ's Himino emphasised this week that the policy path isn't set in stone. But the bank does seem to have quite a strong view on the path the economy is taking. This week's inflation data were consistent with that, but labour market data were a bit softer, and there's no consumer pick-up yet.