Public Post

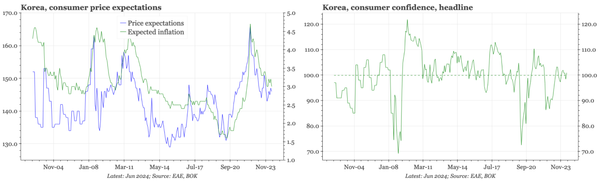

QTC: Korea – no change in consumer sentiment

There's nothing in the June consumer confidence survey to shift the BOK. Confidence was neither strong nor weak. General price expectations ticked down, but picked up for property.