Public Post

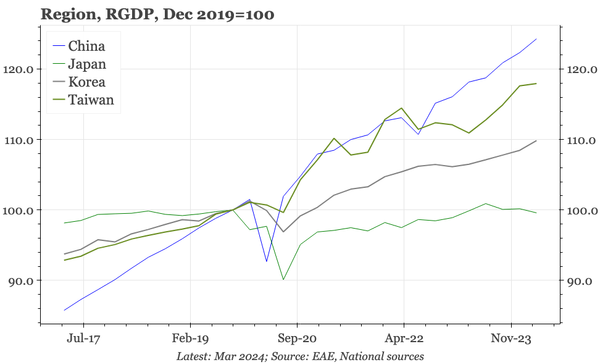

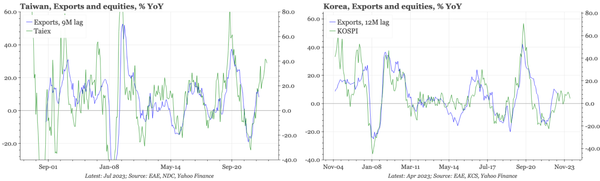

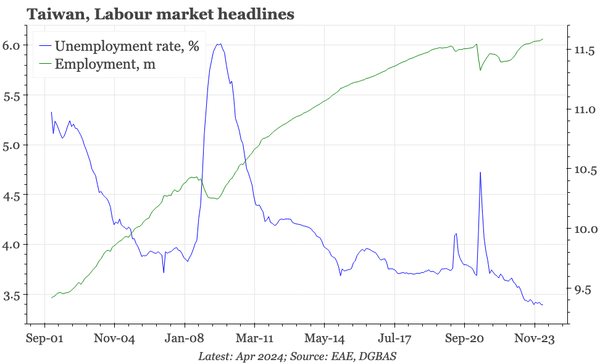

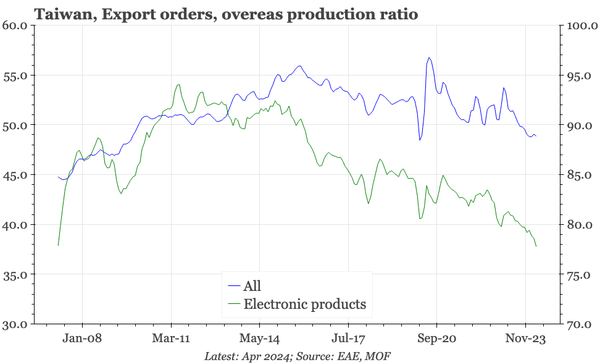

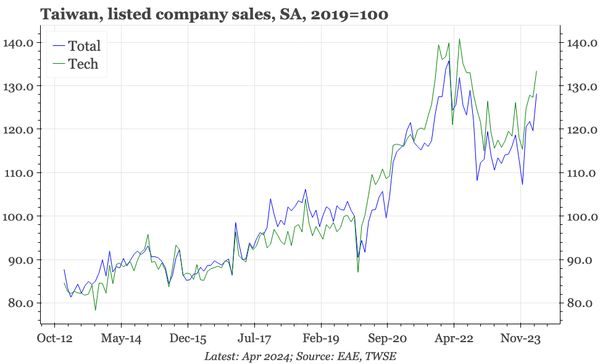

QTC: Taiwan – no consumer slowdown

Domestic activity carried the economy in 2022-23 as exports slowed. Exports are now picking up, but consumption is also remaining solid. Consumer confidence isn't particularly strong, but purchasing intentions are.